Weekly Economic Commentary | November 14, 2025

How Governments Can Repress Debt

Repayment is just one way to manage debt.

By Carl Tannenbaum

I learned about the civil rights movement in grade school. Inspired by the practice of nonviolent objection, I refused to do the dishes one night unless my allowance was increased. Forced to the sink against my will, I said to my mother: “I am being repressed!”

That was a big word, and I didn’t understand what it implied. In the intervening years, I have acquired a more complete appreciation of what repression is, across a range of domains. But I didn’t know until recently that the term has meaning in the world of finance. The prospect that a form of repression will be used to deal with sovereign debt is a source of concern.

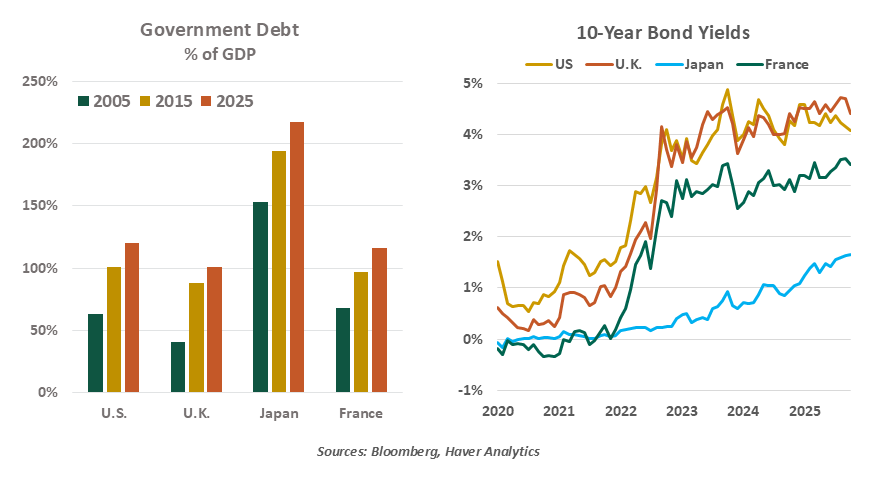

Government borrowing around the world has risen substantially in the past two decades. Two crises, in 2008 and 2020, required massive amounts of fiscal support to head off worst-case outcomes. Aging populations are increasing the costs of national retirement and medical programs. Additional investment in infrastructure and security have been necessary to safeguard economic growth.

From 2008 until 2021, interest rates were very low (and even negative for some countries), keeping carrying costs manageable. But when inflation surged after the COVID-19 pandemic, central banks and markets moved to raise the cost of credit. Debt interest is rapidly ascending the ranks of top line items in national budgets.

It used to be rare that countries ran large deficits during normal periods, but annual shortfalls of more than 5% of gross domestic product are extending far out onto the horizon. This has exacerbated polarization within legislatures, as leading parties assign blame to one other and offer different policy prescriptions. The resulting gridlock has impacts on markets and societies, as witnessed in Europe this summer and during the recent U.S. government shutdown.

I have often been asked when, or how, this will all end. Is there some tipping point that would prompt governments to become more austere? Will the “bond vigilantes” of forty years ago ride again, punishing budget recklessness by requiring higher yields? Could the International Monetary Fund be called upon to prevent a major economy from defaulting, as it did for the United Kingdom in the 1970s?

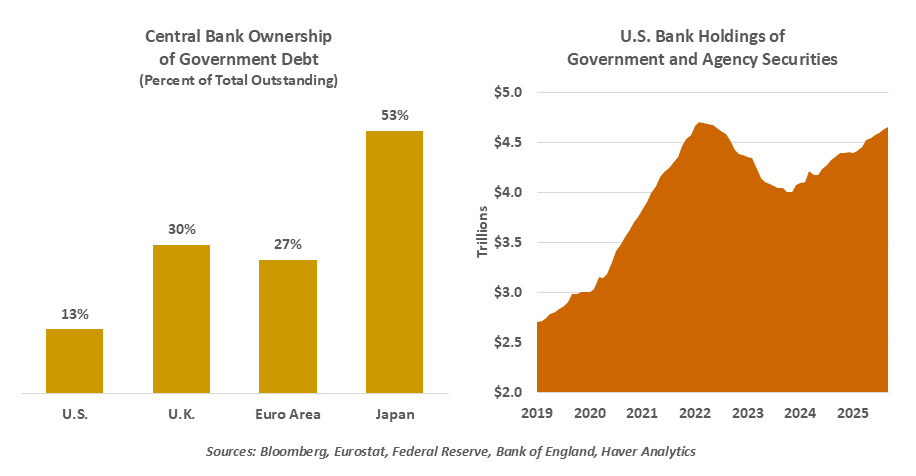

Central banks have become substantial owners of government securities.

I doubt that the most dire of those outcomes will ever be reached. One reason why is the practice of financial repression, which refers to policies that governments use to limit their indebtedness or the interest paid on that debt. Capture of the central bank is the most common way this is achieved. Ever since countries ended the practice of making their currencies convertible to gold, printing money to support fiscal policy has become popular.

In several large economies, the battle over the printing press has been rejoined. Efforts by the White House to control the Federal Reserve have intensified, and some in the U.K. regret moving the Bank of England out from under the U.K. Treasury twenty years ago. The European Central Bank has been a target of constituent countries almost from the moment it was founded.

Getting the central bank to lower interest rates without regard for economic fundamentals is one form of financial repression. But another avenue is to get the central bank to purchase and hold significant amounts of government debt. The door was opened to this strategy in 2008, when the term “quantitative easing” entered our vocabulary. Since then, central banks have come to own significant fractions of their countries’ outstanding bonds.

Efforts to bring those holdings back down to pre-crisis levels have been complicated. For the second time in six years, the Federal Reserve was recently forced to end its balance sheet runoff sooner than many had been expected. Thin liquidity in the financial markets was cited as justification for the decision.

Central banks are not directly mandated to ensure adequate liquidity in financial markets. But steering short-term interest rates to the desired level requires liquid markets. To meet their objectives, therefore, monetary authorities may be forced to finance more and more of their nation’s debts. At least in appearance, this compromises their independence.

The downside of this form of financial repression is higher inflation, which occurs when too much money is chasing too few goods and services. The United States used this tactic in the 1970s to keep Vietnam War era debt from becoming too onerous; the cost came at the end of the decade, when inflation reached 13.5%. There is a risk that central banks will allow inflation to run hot in the decade ahead, something that markets are not prepared for.

Financial repression has costs for investors and societies.

There are other ways to effect financial repression. The Mar-A-Lago accord proposed by current Federal Reserve governor Stephen Miran calls for foreign governments to hold allocations of Treasuries to help manage the value of the dollar. Capital controls can be used to keep investors at home. Bank reserve and liquidity requirements can also be employed for this purpose: U.S. banks hold $2 trillion more in government debt than they did six years ago.

These measures may not appear pernicious on the surface, especially if they head off more severe consequences. But policies that limit freedom of capital movement prevent it from reaching optimal destinations. Money locked into government bonds cannot be allocated to more productive investments. Artificially low interest rates tax savers, and may result in lower levels of national saving. All of these have economic costs.

I now understand that my parents were practicing a form of financial repression. I was required to take what little allowance I received and deposit it into a low-yielding passbook savings account. I didn’t like repression then, and I still don’t.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.