India's Incomplete Growth

An economy cannot subsist on services alone.

By Vaibhav Tandon

As I inch closer to middle age, my naturally dark hair is progressively being overshadowed by shades of gray. I’m learning to embrace the “salt and pepper” look.

With an average age of 29, a large proportion of people in India still sport more pepper than salt. But while India continues to enjoy a large demographic dividend, its economy is far from maturity.

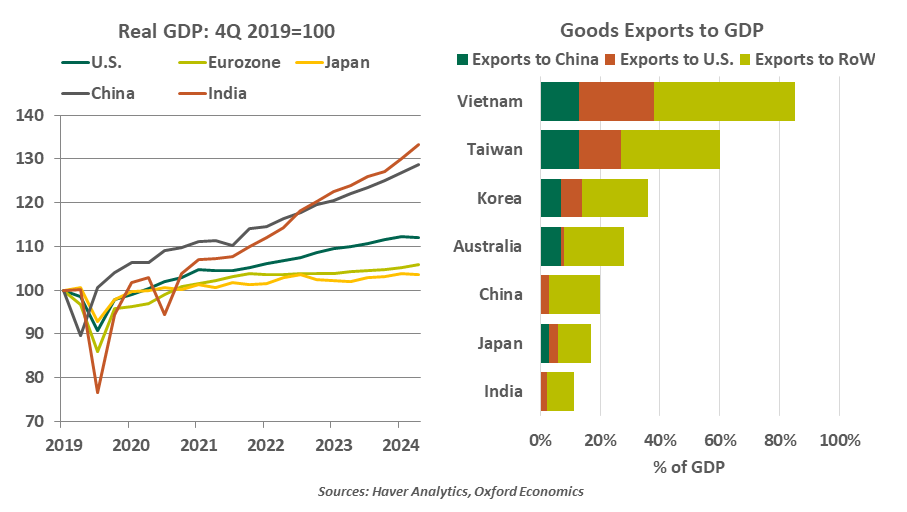

India remains the fastest-growing major market in the world. It is poised to become the world's fourth-largest economy this year, according to the International Monetary Fund. Following a slowdown in the middle of 2024, real gross domestic product (GDP) bounced back in the first quarter of this year, clocking an impressive 7.4% year over year increase.

To some, the first quarter results put concerns of a structural slowdown to rest. But there are challenges on the horizon that could keep India from reaching its true potential.

Some strong foundations are in place. A strengthened monetary policy framework has contributed to a structural decline in interest rates. Yields on 10-year Indian government bonds have declined from around 9% to slightly above 6% over the past decade. Inflation has fallen below 4%, the midpoint of the central bank’s target range, allowing a full percentage point of short-term rate cuts over the last few months.

India’s external account position has drastically improved. Foreign reserves remain near a record high of around $700 billion, equivalent to 11 months of import cover. The government has remained committed to fiscal prudence: India’s fiscal deficit has declined from 9.2% of GDP in 2020 to 4.8% in the most recent fiscal year. External debt has been increasing, but is modest when compared to other emerging markets (EMs).

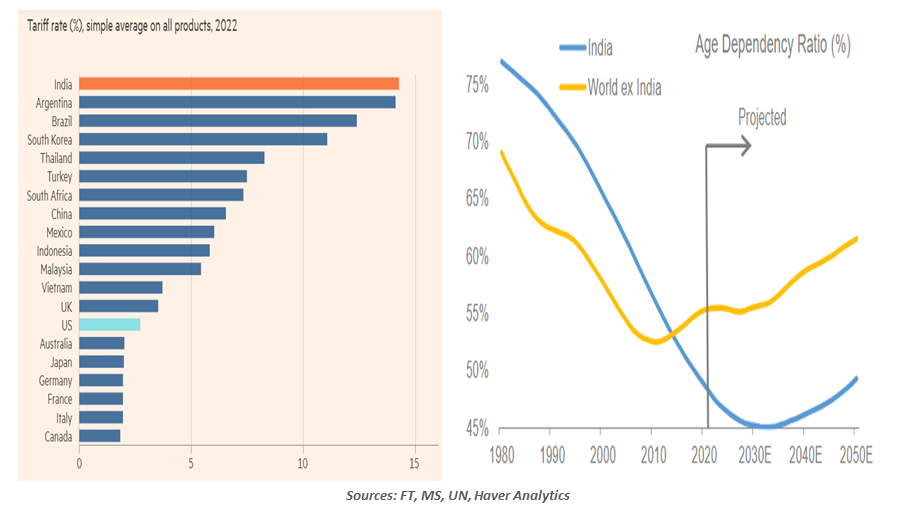

Despite being one of the most protective economies (India has the highest average import duty in the world), India has managed to avoid the worst of U.S. trade retaliation. Indian exports were hit with a 26% reciprocal tariff, far below the duties announced on many other markets. The relatively modest merchandise trade surplus of $45 billion likely helped India escape more punitive actions.

India has not benefitted from recent shifts in global trade.

Even though America is India’s largest export market, accounting for about 18% of goods, the economy is not overtly reliant on trade with the U.S. or the rest of the world. Merchandise exports account for 11% of India’s economic output, compared to 85% in Vietnam. About 30% of Indian exports, including critical products like pharmaceuticals, remain exempted from U.S. levies. A trade accord between New Delhi and Washington seems likely.

Further, India is a much more prominent exporter of services, not goods. India’s services exports have grown rapidly over the past decade and surpassed goods shipments briefly in late 2024. India is the world’s seventh largest service exporter; by contrast, the country ranks 16th globally in manufacturing exports.

While the focus on services has been a relative advantage during the current trade war, India will have to become a more prominent player in manufacturing if it is to perpetuate recent economic success. The service sector employs less than a third of India’s large labor force of about 600 million people.

The nation remains a laggard with a mere 3% share of global industrial production. Global trade shifts have only delivered small gains to India, not windfalls. India’s share of U.S. goods imports rose only 0.6 percentage points to 2.7% between 2017 and 2023, even as China’s share dropped around eight percentage points over the same time period. The country’s limited gains have been concentrated in low-cost or lower value-added products like textiles and minerals.

India’s manufacturing sector has struggled to boost its contribution to the domestic economy. Reliance on Chinese inputs, which constitute 15% of total imports, has been growing.

Like China, India has a large domestic market and ample, low-cost labor. Improvements in infrastructure have facilitated construction and logistics. These factors make India a promising location for setting up industrial plants, but India continues to fare poorly in its ease of doing business. Other Southeast Asian economies offer simplified tax laws and more extensive free trade agreements, making them more popular destinations for companies’ operations.

A developing economy lifecycle typically entails a shift from an agrarian base to manufacturing, followed by a transition to services. The Indian economy seems to have skipped the industrialization phase. The lackluster performance of the manufacturing sector is one of the key reasons why India has fallen behind other EMs in per capita income growth since its economic liberalization in the early 1990s.

India needs an intense push to boost manufacturing.

Boosting the manufacturing sector will be critical to addressing the country’s rising employment needs. India's working-age population is forecast to continue to grow until 2037, giving it one of the lowest old age dependency ratios in the world. India alone is expected to add 21% of the world’s working population in the next eight years.

A growing young population can be a great advantage, but only if that talent is put to good use. India’s current pace of GDP growth will not generate enough jobs to fully absorb this increase in the labor force. According to the World Bank, the Indian economy will need to grow by close to 8% on average over the next 22 years to become a high-income economy.

As its economy matures, India must act aggressively to create more opportunities for its growing population. Failure to address these challenges will prevent the country from making a graceful transition from pepper to salt.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.