Jackson Hole Recap

Discussions ranged from the Fed's next move to its generational challenges.

By Ryan Boyle

Acquaintances are sometimes surprised when they learn I have never attempted downhill skiing or snowboarding. Nothing about the prospect of sliding down a frozen mountainside appeals to me. If I were to attempt it, I would call the day a success if I got through it without injury from the inevitable falls.

Last week witnessed the annual monetary policy thought leadership retreat at the mountain resort town of Jackson Hole, Wyoming. Though held outside of ski season, this year’s event took place in a perilous context. The theme was Labor Markets In Transition – Demographics, Productivity and Macroeconomic Policy. Given mounting challenges, the opportunity to slip and fall was elevated.

Jerome Powell opened with his eighth and final address to the conference in his role as Federal Open Market Committee (FOMC) Chair. His remarks were more closely watched this year than is typical, as investors try to gauge when the FOMC will next cut rates. Powell’s speech seemed to give an all-clear signal for a cut in September. The speech started with a focus on the softening labor market, concluding it is in a “curious kind of balance” with rising risks of layoffs. Regarding inflation, he expressed a “reasonable base case” that tariff-driven inflation will be short-lived. While every statement was hedged, it was by no means a pushback against hopes to see easier policy.

Powell also took the occasion to preview changes to the Federal Reserve’s monetary policy framework. Every five years, the Fed revisits its Statement of Longer-Run Goals and Monetary Policy Strategy, which offers detail as to how the FOMC will approach their Congressional mandate. The statement was last revised with unfortunate timing in 2020. On the heels of a prolonged cycle of below-target inflation despite very low rates, the FOMC adopted a “flexible average inflation target.” This approach intended to heat the economy to exceed target inflation, bringing about a long-run average of 2%. In hindsight, welcoming inflation was the wrong stance for the challenging cycle that ensued.

Powell characterized the new framework as an evolution. The FOMC removed its focus on the challenges of operating in a zero-rate environment and will no longer seek to overshoot inflation. The new statement will balance the Fed’s dual mandate of employment and inflation, no longer referring to “shortfalls” in employment but more broadly to “deviations” from optimal levels. It adds new language as to how the FOMC will address intervals in which its two mandates are in tension.

The Fed will adapt its strategy to a higher-inflation world.

While markets received the address well, we found the speech notable for its omissions. His comments were focused on the present moment, not adopting a broader view of structural changes like the evolving labor market dynamics that were the theme of the event. In his final appearance, he could have offered a retrospective on his tenure. And crucially, Powell took the high road regarding current events, avoiding any acknowledgement or retort about political efforts to influence the Fed. Subsequent developments showed that this did nothing to calm the situation.

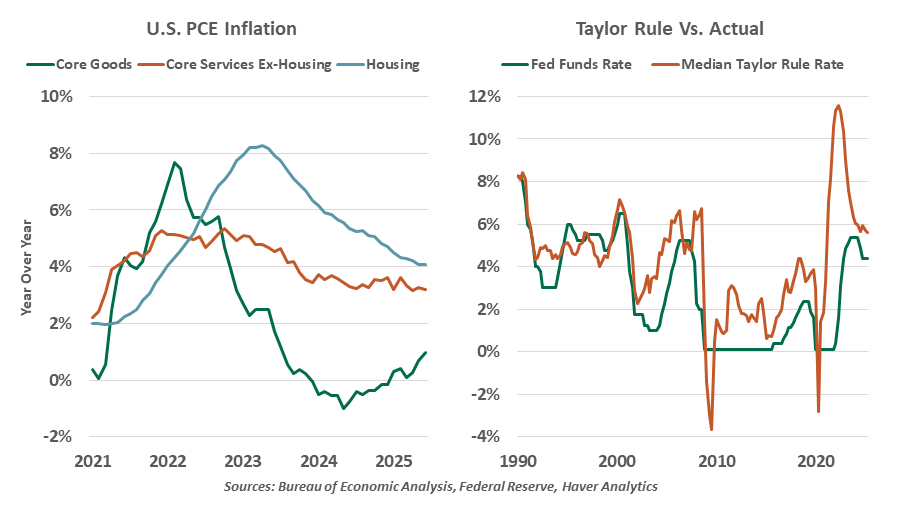

Following Powell’s remarks, the agenda highlighted academic research into labor markets, with speakers who attempted to point the way toward policies that can sustain economic growth. Starting with a central banking focus, the Balancing Labor Markets and Inflation paper revisited the Taylor Rule, an approximation of the optimal Fed Funds rate for a given rate of inflation and output gap. These formulaic approaches have been less useful in the past two cycles, yielding volatile and unworkable estimates of target rates. The paper explored the conditions in which central banks have successfully deviated from the Taylor Rule; in the face of one-off shocks, and accompanied by strong forward guidance, the rules can take a lower priority in rate-setting.

Other pertinent discussions included:

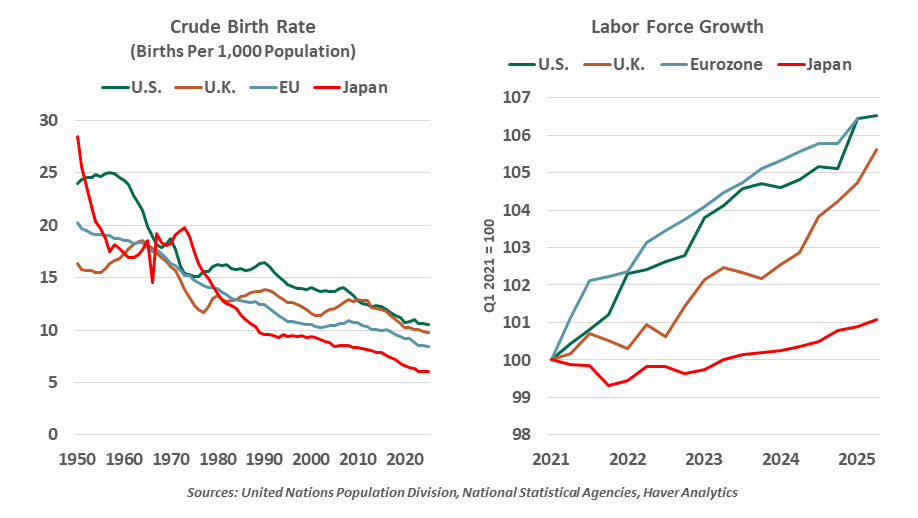

- The structural challenges of demographics and declining mobility. Fertility is falling in much of the world, with one paper exploring the accompanying increase in women’s education and employment prospects.

- U.S. workers are relocating less often. While workers do still move in response to greater demand for labor, these regional shifts have become smaller and less frequent.

- An aging workforce increases demand for financial assets for savings. Researchers attempted to price the effect this has had on returns.

- And of course, technology continues to change the nature of work, with an academic discussion and keynote speech on artificial intelligence.

Labor market trends are challenging across several dimensions.

The agenda was bookended by central bank dignitaries, concluding with a group panel featuring the leaders of the European Central Bank, Bank of England and Bank of Japan. Each offered views of their own evolving labor markets. Japan has long faced tight labor supply due to demographics, a contributing factor to their low-rate environment. Euro area labor markets have been resilient, growing from both high immigration and greater participation. That trend could shift, as is happening in the U.K., where participation and productivity have been sluggish. Every region is different, but all share concerns about shifts in the labor market.

Recent headlines have brought a connotation of chaos to the Federal Reserve. The Jackson Hole proceedings were a reminder of the central bank’s commitment to its mission and intellectual rigor in addressing long-run challenges. The course ahead will be a challenging slalom that could take them off piste. We believe they have the skill to carve a safe path down the slippery slopes.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.