Japan: A Return to Abenomics?

New Prime Minister Takaichi can learn from past reforms.

By Vaibhav Tandon

As Japan’s first female prime minister, Sanae Takaichi shattered a long-standing political glass ceiling. Her economic plan risks breaking Japan’s fiscal ceiling.

A protégé of former Prime Minister Shinzo Abe, Takaichi is seeking to revive his economic playbook of high public spending and low borrowing costs. She has reportedly begun preparing an economic stimulus package worth more than ¥13.9 trillion ($92 billion) to shore up the economy. Takaichi has indicated plans to lift the income tax exemption threshold from ¥1.03 million to ¥1.6 million yen. The prime minister has already moved to abolish the half-century-old provisional gasoline tax rate and is set to introduce electricity and gas subsidies to ease cost of living pressures. Takaichi also wants to accelerate the timeline for increasing defense spending to 2% of gross domestic product (GDP).

Though Takaichi supports expansionary fiscal and monetary policies, she has emphasized a commitment to long-term financial discipline, including reining in the government debt to GDP ratio. Political and economic realities may have compelled her to strike a more cautious tone.

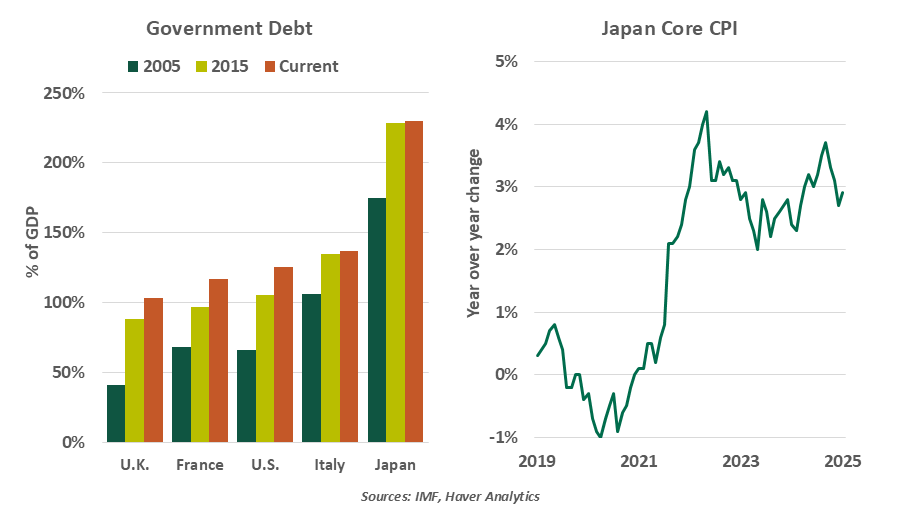

Large-scale fiscal easing will be difficult to deliver. Takaichi is presiding over a minority government and facing resistance from the Japan Innovation Party, which favors small government. Since its asset price bubble burst in 1989-90, the Japanese government has run persistent budget deficits. The “lost decades” have pushed Japan’s public debt burden to the highest among major advanced economies, now more than double the size of the Japanese economy.

The need and room for aggressive easing in Japan has diminished.

On monetary policy, Takaichi could pivot to support the Bank of Japan’s gradual normalization to avoid yen depreciation and a spike in long-term yields. Moreover, the case for ultra-loose monetary conditions no longer exists, as the challenge has shifted from unwelcome deflation to unwelcome inflation.

While the glass ceiling has been broken, the fiscal ceiling remains a fragile construct. Takaichi’s real challenge will be pursuing a fiscal agenda that lifts growth without allowing its weight to further strain already stretched public finances.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.