Office Property On The Upswing?

The office real estate sector is working through a difficult cycle.

By Carl Tannenbaum

After a year of working concurrently in our home during the pandemic, both my wife and I were delighted when offices reopened. As she put it, “our marriage isn’t built for so much togetherness.”

Not everyone was similarly thrilled. Many workers came to appreciate the time saved in commuting and the flexibility to balance priorities during the day. Stanford economist Nicholas Bloom has found that working from home is seen as the equivalent of an 8% pay increase by employees. Firms have benefitted from lower levels of attrition and the opportunity to reduce their rental bills.

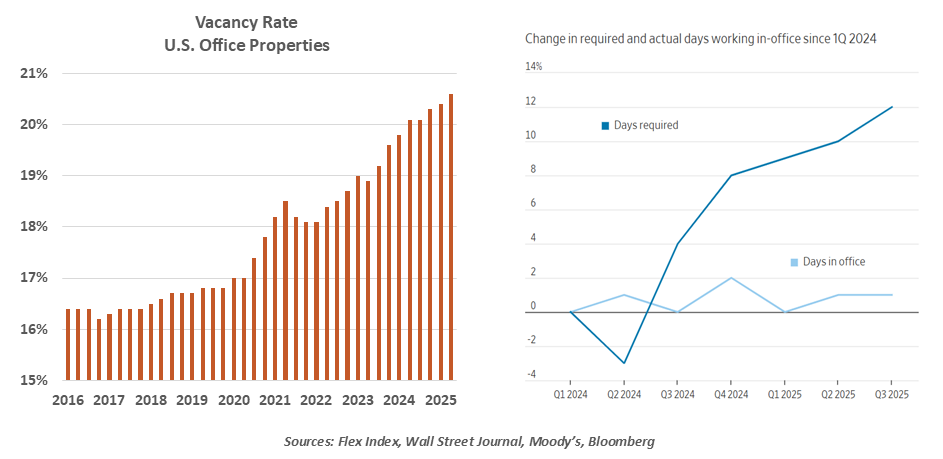

But what appeared to be a win-win situation has been anything but for office landlords. As we discussed in a spot entitled “Out of Office,” the transition to hybrid work initiated a painful reckoning for commercial real estate. According to Moody’s Analytics, office vacancy rates reached an all-time high of 20.7% in the second quarter of this year. Delinquency rates on securities backed by office building mortgages have soared.

To date, though, these trends have not resulted in trauma within the banking system. One reason is that office real estate is heterogeneous: for every skyscraper in an urban center, there are hundreds of more modest buildings spread out across the country. “Class A” properties have fared much better than those of lower quality. More than two-thirds of office properties are 90% leased, just a shade lower than we saw prior to the pandemic. Occupancy levels in some metro areas have slumped, while others have seen only modest declines.

Lenders have generally been proactive about reserving for problem credits and negotiating effectively with property owners to avoid worst-case outcomes. The banking industry has maintained very strong capital levels.

Going forward, there may be reason for hope in the office sector. Firstly, a number of companies have recently announced increased attendance requirements and intentions to monitor compliance more closely. The moves are motivated by a core belief in the value of personal interaction, but the timing may have something to do with labor market conditions.

The U.S. unemployment rate has been near or below 4% for much of the past three years. The rate at which workers quit their jobs (typically for better ones) reached a 20-year high of more than 3% in 2022. Firms were working hard to attract and retain talent, and used flexible work arrangements as a means to that end. Today, by contrast, the unemployment rate is rising and the “quits rate” has fallen below 2%. This may be prompting firms to bring more people back into offices more often.

After a five year slump, there are signs of hope for office properties.

There remains a substantial gap between what firms would like to see and what they are getting. Surveys find that workers are spending the same amount of time in offices as they did at the beginning of last year, despite increasing demands. But for the first time in five years, prospects for occupancy are improving.

Falling interest rates will also be helpful for office properties. Ongoing carrying costs are becoming more manageable, and credit is being extended at more reasonable terms. Commercial real estate loans are typically renewed at three to five year intervals; easier financing conditions may help deal with the wave of maturities on the horizon.

Increased investor demand and lower long-term interest rates have combined to increase valuations and the number of transactions for office buildings. Lower rates also boost the economics of office building conversions. Markets with an excess of office space and shortages of apartments are seeing an increased number of renovation projects. According to AllWork, nearly 150 million square feet nationwide are set to be repurposed.

To be sure, it is unlikely that office occupancy and office property values will return to pre-pandemic levels anytime soon. But there may be a little light at the end of the office corridor.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.