Rethinking Bank Regulation

The right level of regulation requires careful calibration.

By Carl Tannenbaum

There is a strongly held belief in the Administration that excessive rulemaking has stifled innovation and economic growth. The financial sector has been one of the focal points of the deregulatory agenda. This is especially visible in the following areas:

- Capital rules. Banks hold equity and long-term debt to buffer against losses that might cause the firm to fail and thereby threaten the financial system. Capital requirements are coordinated internationally by the Basel Committee on Banking Supervision (BCBS). The BCBS proposed a new framework in 2023, which would have raised minimums on large U.S. banks. It now appears that the U.S. will not adopt this standard, creating a big gap with European practice.

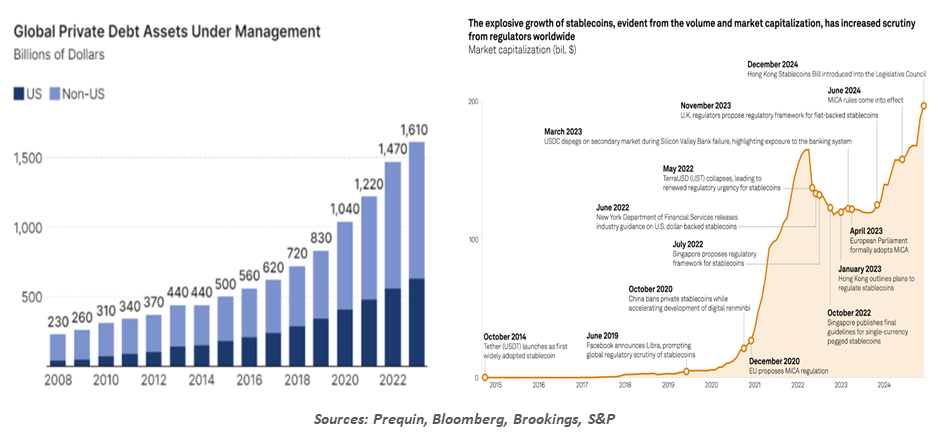

Setting the right level for bank capital is not easy. Too little creates systemic risk, and too much hinders the flow of capital through the economy. Traditional intermediaries are already losing ground to private credit pools, which do not face the same level of oversight. Regulators will do well to keep 2008 in mind as they seek to reframe standards in this area. - Stablecoins. As we discussed in our background piece on this topic, stablecoins account for a small but growing fraction of financial assets. Congress has moved to liberalize the creation of stablecoins, which have the potential to compete with banks for deposits, or become a new medium for banks to manage transactions. Despite the name, stablecoins can be destabilized by a number of forces, which need to be monitored carefully.

A lighter regulatory touch could increase both credit flows and systemic risk.

- Climate risk. Global regulators had arrived at standards that would lead banks to account for climate risks. This can take the form of physical risk to bank facilities or loan collateral, or transition risk which accounts for the gradual impact of climate on the financial standing of companies, industries and regions.

Firms were slated to expand disclosure of their vulnerability (and that of their vendors) to climate change, and to implement processes to measure and manage risk. Earlier this year, however, major U.S. regulators turned away from these efforts.

The costs to insure against and recover from severe climate events are already on the rise. Regulation notwithstanding, banks will have to account for this.

As is the case for other industries, banking regulation tends to swing from heavy to light based on the proximity of the last crisis. Let’s hope that the changes being made today don’t bring the next crisis closer.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.