The Bank of Japan Prunes Its Portfolio

The central bank balance sheet is moderating.

By Vaibhav Tandon

A Generational Exit

Desperate times call for desperate measures. But decisions made during a crisis can have lasting impacts.

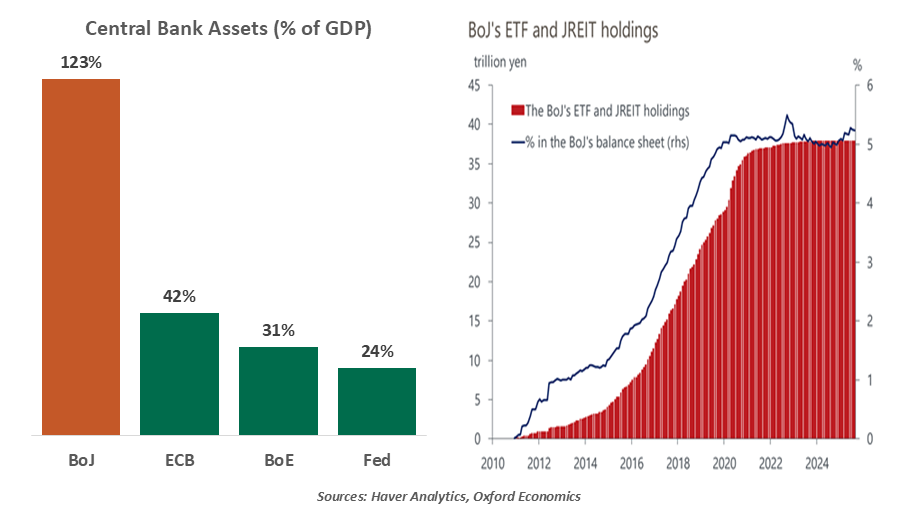

In the late 1990s, the Bank of Japan (BoJ) reacted to the Asian financial crisis by purchasing domestic stocks, long considered too broad of an intervention by a central bank. This became a major step in the exceptional expansion of the BoJ’s balance sheet, both in terms of size and composition. Now, many years later, the central bank plans to unwind those holdings.

The BoJ kept its policy rate unchanged at the September meeting. But it surprised markets by announcing intent to begin selling its holdings of Exchange-Traded Funds (ETFs) and Japanese Real Estate Investment Trusts (J-REITs). Coming just over a year after the central bank unveiled a roadmap for quantitative tightening, this move is seen as another step toward policy normalization. Deflation, a problem for decades, appears to have been conquered.

Japan is charting course to end an era of ultra-easy policy

Market reaction has been fairly muted and is likely to remain so, given the glacial pace and limited scale of the unwinding. The BoJ intends to sell ETFs and J-REITs at an annual rate of about ¥625 billion, representing about 0.05% of total market value.

The planned pace of selling is similar to the one used when the BoJ sold stocks it had accumulated between 2002 and 2010, in the aftermath of financial crisis of the late 1990s. That process spanned nine years and ended only recently in July 2025.

The BoJ Governor acknowledged that it could take more than a century to completely unwind these holdings. A faster process would risk igniting a broader sell-off, as the BoJ holds roughly 7% of the Japanese stock market via ETFs and about 5% of the J-REIT market. The BoJ’s 2021 shift from Nikkei-linked ETFs to those tracking the Topix triggered a 6% drop in the Nikkei over the following four sessions.

As of mid-September 2025, the BoJ holds about ¥80 trillion worth of ETFs and J-REITs. At current prices, these holdings carry an unrealized profit of around ¥44 trillion. This places the BoJ at an advantage to other central banks, whose bond holdings are underwater.

While the pace of QT will be slow, the decision by the BoJ marks another step toward closing an extraordinary era of monetary policy. The BoJ broke new ground with its asset purchases, and we welcome the signal that desperate times are in the past.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.