The View From The Far East

Asian economies are in the crosshairs of U.S. trade policy.

By Carl Tannenbaum

There is an expression in Mandarin that translates to English as “Hearing it a hundred times is not as good as seeing it with your own eyes once.” I couldn’t agree more. I read reports on Asia all the time, but understanding the region requires time on the ground.

I spent the last two weeks of May catching up with partners and clients in Malaysia, Singapore, China, and Hong Kong. Following are some reflections on those conversations.

- Clients in Asia were not surprised that tariffs would be used as leverage by the United States. President Trump had promised as much during last year’s election campaign.

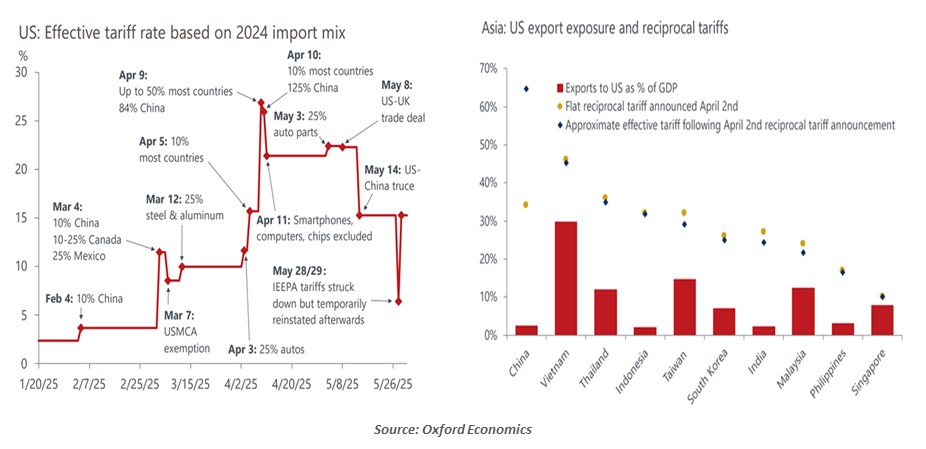

What did surprise them has been the rapidly shifting tariff landscape. New levies are proposed, and then deferred days later. Exceptions are belatedly granted for more essential items. Threats escalate, and then negotiations bring things back from the brink. Accords are typically temporary, creating a string of expiries that keep stakeholders on edge. Courts are beginning to weigh in on the legality of trade measures.

The rise and retreat of tariffs against the European Union, which occurred during the middle weekend of my journey, was cited as a case in point. An audience convened for breakfast in Hong Kong on the morning of May 29 hailed the injunction against reciprocal tariffs handed down by the U.S. Court of International Trade. I had to caution that this would not be the last word on the matter; the President has appealed, and he has other avenues that he can pursue to keep the pressure on. A handful of emerging economies in Asia are most at risk, given their reliance on exports to the U.S. and the level of tariffs that have been proposed.

The potential boundaries on U.S. tariffs have become a little clearer. Negotiations, legal proceedings and market reactions are defining a ceiling. The administration would like to sustain a floor of 10%, if the law allows. This corridor of outcomes helps bring a little clarity, but high levels of uncertainty will continue to challenge policy and planning.

No one expressed anger towards the U.S. during my rounds. The prevailing sentiment was puzzlement; Asian countries had come to think that their partnerships with America were a source of strength, and are wondering why the benefits of economic and cultural interactions seem to have lost currency. No one wants a trade war, but neither are they willing to retreat too far from arrangements they see as mutually beneficial.

It may take quite a while for China and the United States to reach a durable trade agreement.

- Both China and the United States feel as if they have the upper hand in trade negotiations.

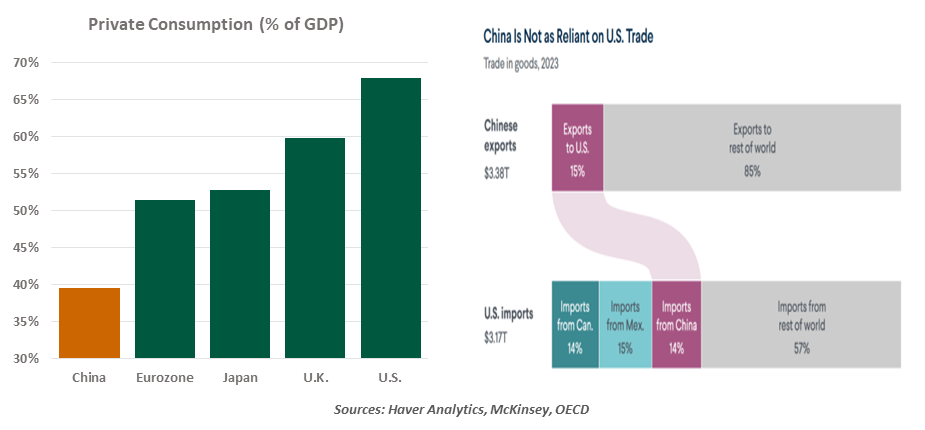

American negotiators point to inherent weakness in the Chinese economy as a motivation to make a deal. Overall, China remains very reliant on exports, as domestic consumption has been sluggish. But while China sells a lot to overseas buyers, exports to the U.S. make up a modest fraction of the total. And the U.S. is dependent on key Chinese imports like rare earth minerals, which are currently being restricted.

On the other side, prices for many items in the U.S. will start to show the effects of tariffs later this year. The Chinese are betting that the increase in inflation will not sit well with the American populace, creating an economic and political problem for the White House.

With both sides sensing that the other is under pressure, a durable agreement between the two countries will take time to complete.

- Investors in Asia have extensive holdings of U.S. stocks and bonds. Those assets have performed well, and the depth of America’s financial system remains an attraction.

We fielded a number of questions during the fortnight on the performance of U.S. markets and the U.S. currency. American stock returns have lagged this year, partly because of the shadow being cast by trade policy. The fiscal bill that is making its way through Congress seems likely to add trillions to the national debt over the next decade. The U.S. dollar has lost about 10% of its value this year against a trade-weighted basket of other currencies.

No one confessed to wholesale asset reallocation, but there is concern that this is the beginning of the end of American exceptionalism. If global investments lose their anchor, finding safe harbor will become very challenging. And for as long as Treasury bonds remain the world’s reference asset, increases in U.S. yields and term premia will carry over to other markets. This may make it more difficult for some countries to sustain their own debt levels.

There is no sign of a mass exodus from U.S. markets or the U.S. dollar.

The schedule for my visit was packed, but I did have the chance to enjoy some memorable meals. Our team in Singapore arranged a dinner in a local place that specializes in fresh seafood, taken from saltwater tanks on the premises. No white tablecloths: we were seated at a big round plastic table set on the boundary of the parking lot. The clams in lemongrass broth and the chili crab were amazing, and the spirit at the table was high.

In Beijing, our new country head led us out for a simple meal of char siu, steamed chicken, and roast goose. In Malaysia, we enjoyed beef rendang and whole snapper in chili sauce. Lunch in Hong Kong included dan dan xiao long bao, soup dumplings with a fiery filling. And during a hawker center crawl on a Saturday morning in Singapore, we concluded with fresh durian. Many are turned away by the odor that emanates from the fruit, but I have come to enjoy it very much.

One day, I hope to enjoy some leisure travel in Asia. A more relaxed pace will allow for a deeper connection with the region, its people, and its cuisine. Until then, I hope that the tone surrounding trade with the area will become more relaxed and that the connections we share will remain strong.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.