Trade War: New Countdown Begins

Trade deals demonstrate that tariffs are here to stay.

By Vaibhav Tandon

President Trump’s tariff war has stirred up a whirlwind of disruption, affecting businesses and supply chains. As conditions begin to settle, the outlines of a new trade landscape are emerging.

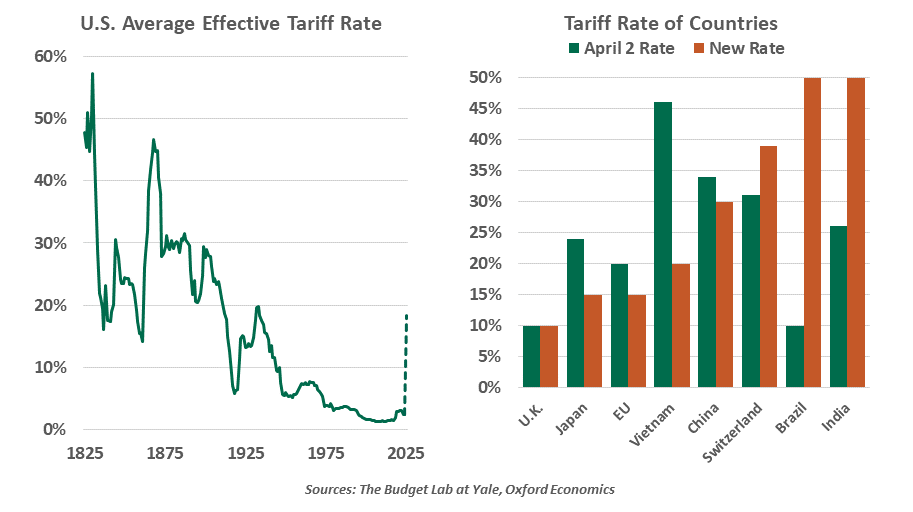

The August 1 deadline for trade talks produced reprieve for some and dismay for others. A handful of governments secured last-minute deals, avoiding steeper levies. But many were left exposed to sweeping trade penalties. The U.S. administration has maintained a baseline 10% duty for around 100 nations, alongside “reciprocal” tariff rates ranging from 15% to 50% for 70 economies. America’s major trading partners like the European Union (EU) and Japan are subject to a 15% penalty, with certain sectoral exemptions.

Governments that have not reached a deal or have large trade surpluses with the U.S. are facing steeper country-specific duties. Switzerland is now subject to a 39% tariff. Canada is facing a 35% import tax, although it applies only to goods that do not comply with the United States-Mexico-Canada Agreement.

Trade and economic considerations were not the sole criteria for tariff decisions. A 50% tax applies to most Brazilian imports, linked to the prosecution of its former president. India has joined Brazil in facing the highest import duties, due to its oil trade with Russia.

In sum, levies on the vast majority of U.S. goods imports have soared. The average effective tariff rate has skyrocketed from just under 3% before February 2025 to 18.3% — a level not seen since the depths of the Great Depression in 1934.

Even with current agreements in place, the haze of uncertainty won’t vanish anytime soon. Deals are yet to be hammered out with important trading partners like Canada and Taiwan. Higher duties on Mexico have been paused for another 90 days, but not dropped. Still up in the air are assessments on commerce with China, and on key sectors like pharmaceuticals. If no comprehensive trade agreement is reached, U.S. levies on Chinese goods could revert to their immobilizing April levels.

Many of the deals announced thus far are framework or verbal agreements, unsigned and with details yet to be ironed out. Billions of dollars in investments were promised in deals with the EU and Japan, but it is unclear if and how the commitments will be delivered. These investment pledges could prove to be more symbolic than substantive.

Despite recent deals, tariffs are set to skyrocket.

Countries facing high “reciprocal” tariffs are among the most vulnerable, but it's not just the magnitude of import taxes that will determine the extent of economic losses. Markets with deep commercial ties with the U.S. stand to lose the most from the trade war. The German economy is highly reliant on international commerce, with about one-third of gross domestic product tied to goods shipments. The U.S. is a top destination, with automobiles as the single largest export category. Therefore, a 15% duty on German imports could prove to be more disruptive than a 50% penalty on a country like India, which is far less reliant on goods trade.

Chinese exports are not only subject to one of the highest import duties, but they will be further challenged by America’s efforts to restrict trade rerouting. An additional 40% levy on transshipments has Southeast Asian economies like Vietnam bracing for major supply chain disrupts.

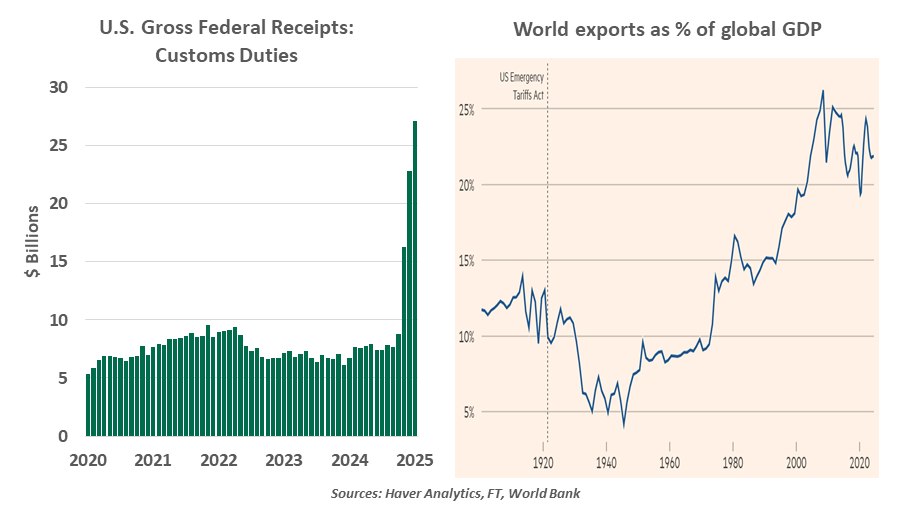

Alongside trade rebalancing and reindustrialization, boosting tariff revenues is also a core objective of the Trump administration’s global commerce policy. There has already been a surge in U.S. customs duties, with over $100 billion collected so far in 2025 (up from $79 billion in the full year 2024). America imported goods worth $3.3 trillion last year. An effective tariff rate of 18.3% would have yielded around $600 billion in proceeds, though substitution and demand elasticity will lower the final tally.

While tariff revenues may help offset U.S. fiscal imbalances, American households will bear the burden of trade restrictions. U.S. corporations are absorbing higher input prices, but this strategy is proving increasingly unsustainable. As pressures mount, many companies are passing these costs through. Imported products including apparel, furniture, toys, watches and cars are all set to become more expensive. Rising prices will force a cutback in discretionary spending, limiting America’s consumption-driven economy.

Brazil’s government has chosen to focus on providing relief packages to industries hit hardest by U.S. tariffs, rather than pursuing retaliation. Canada is actively exploring and expanding into new export markets to mitigate economic damage. But disruptions to broader flows of goods could still prompt job losses and dampen earnings in trade-dependent economies.

International trade will never be the same again.

Asian exporters have not yet taken the full tariff hit, but the growth drag will become more salient as front-loading effects fade. Higher duties could trigger price cuts and lower export volumes. Early signs of damage to the growth cycle are starting to emerge. Asia’s capital imports registered a sizeable month-on-month decline in June, signaling weaker momentum in capital expenditures. Like the protectionist eras of the 1920s and 1930s, America’s tariff war will have profound effects on international trade.

Higher tariffs do not mark the end of globalization. But they are set to usher in a new era of fragmented, protectionist and unequal trade. Striking bilateral or regional deals will become the preferred way of conducting cross-border commerce. Nations will focus on strategic autonomy in critical sectors and lower dependence on unreliable partners.

Sandstorms create displacement and debris, which can be dealt with. We hope that this trade war does not leave economies biting the dust.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.