Asia Pacific Economic Outlook | January 26, 2026

Sailing Through Turbulence

Asia‑Pacific nations enter the new year with steady growth prospects, even as uncertainties persist.

Asia‑Pacific enters 2026 much like a seasoned sailor steering through shifting currents. The region is moving ahead with purpose, but aware that the waters are far from calm. Major regional economies are still benefiting from the momentum built last year. Domestic demand is holding up across much of Asia, with China the notable exception. Tech investment remains an important anchor of growth. Financial conditions have eased after a long stretch of tightening.

Unfortunately, tailwinds have their limits. The fading impulse from global goods trade, a maturing artificial intelligence-driven tech upswing, and weak demand from China all suggest that the breezes pushing the region forward will be less supportive in 2026.

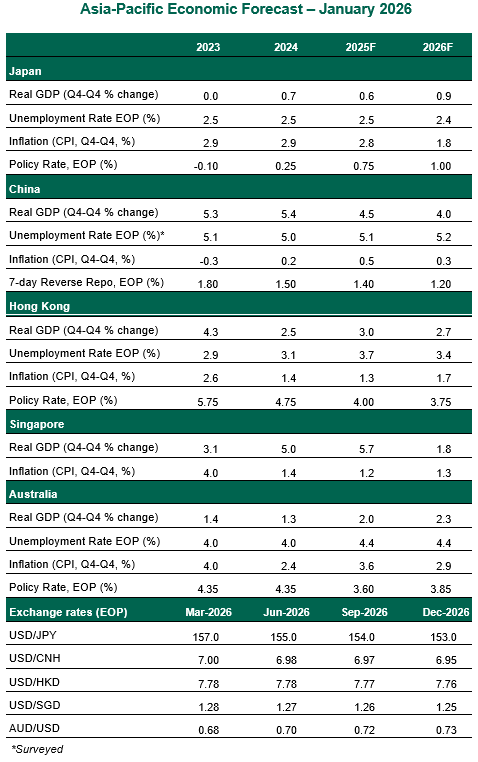

Following are our views on how major APAC markets are poised to perform.

Japan

- Japan’s real gross domestic product (GDP) contracted 0.6% on a quarterly basis in the third quarter, reflecting broad‑based weakness across domestic demand and exports. Consumption should recover as real incomes improve. Headwinds from high U.S. tariffs and trade policy uncertainty are likely to gradually fade in the second half, supporting exports and machinery investment, though the risk of renewed tensions remains. Political frictions with China have risen following comments by Prime Minister Takaichi on Taiwan. Further escalation is not our base case, but any deterioration would be disruptive for Japanese industry and could weigh on bond yields and the yen.

- Prime Minister Takaichi’s announcement of a February 8 snap election has unsettled markets, rekindling concerns about looser fiscal policy and renewed downward pressure on the yen. With headline inflation likely to dip below 2% in coming months due to negative food price base effects, the Bank of Japan (BoJ) is expected to hold policy steady for now. The yen has strengthened recently amid growing speculation over a possible government intervention. But renewed currency weakness, if reinforced by post‑election fiscal expansion, will have implications for BoJ policy. For now, we expect the central bank to hike following Shunto wage negotiations, with risks titled toward one additional increase later in the year.

China

- China met its “around 5%” growth target in 2025, helped by strong first‑half momentum that offset a softer finish to the year. Exports have continued to surprise to the upside, supported by resilient global demand and trade rerouting. Manufacturing indicators are pointing to sustained industrial momentum. The external outlook remains relatively constructive, driven by a rise in exports to markets outside the United States. Rising geopolitical tensions and expanding trade and investment frictions beyond the U.S. pose downside risks.

- Domestically, conditions are less supportive. Persistent weakness in domestic demand in the second half of 2025 is likely reinforcing low inflation expectations among both households and corporations. Weaker retail data reflects slower auto sales and the fading impact of consumer trade‑in programs amid funding constraints. Property market woes persist. We expect policy support in 2026 to remain measured rather than forceful. The goal will be to stabilize activity, rather than deliver a significant growth impulse.

Singapore

- Singapore's economy closed 2025 on a solid footing, underpinned by robust external demand. Real GDP grew 4.8%, up from 4.4% recorded in the prior year. The tariff-related drag on Singapore's trade appears to be milder than initially feared. The domestic picture, while resilient, remains uneven. External demand should stay firm but will provide a smaller lift this year. The artificial intelligence-driven tech cycle that helped bolster activity last year may also lose some steam.

- After back-to-back easing in the first two quarters, the Monetary Authority of Singapore (MAS) remained on the sidelines through the second half of 2025. Inflation momentum has turned up gradually with both headline and core measures holding steady at 1.2% year over year in December. Core inflation should rise in the coming months on account of base effects, though it may not breach the central bank's soft target of around 2%. With growth holding up and price pressures contained, we don’t see a compelling case for further policy adjustments in 2026.

Hong Kong

- Hong Kong’s economy is entering 2026 on noticeably firmer ground. Consumption has begun to improve, trade has outperformed, and financial markets have regained vitality. Even though the boost from trade will moderate, strong equity market gains and the stabilizing residential property market should help sustain momentum. Looser monetary conditions following the Fed’s December rate cut will also filter through, creating a more conducive environment for investment and property market activity.

- The Hong Kong Monetary Authority cut its base rate to 4.0% in December, in lockstep with the latest move by the U.S. Federal Reserve. We think the Fed will lower rates only once in 2026, around mid‑year. While the path ahead may not feature a steady stream of cuts, monetary and financial conditions should remain sufficiently loose to support the island’s economic output.

Australia

- Activity in Australia has firmed, with both household consumption and business investment picking up. Consumption has been supported by improving household finances, reflecting interest rate cuts, tax relief, cost‑of‑living measures, solid wage growth, and a still‑tight labor market. Business investment is beginning to recover, led by a surge in data center construction. Momentum is building toward stronger growth in 2026.

- Recent inflation readings have edged higher, drifting away from the midpoint of the Reserve Bank of Australia’s 2%-3% target band. Last year’s monetary easing contributed to accelerating house prices, further complicating the policy outlook. Firm growth, low unemployment and elevated labor costs all act to raise the risks of renewed inflation. Rate cuts are now off the table for 2026, and we expect the Reserve Bank of Australia to raise rates in the second quarter before moving to the sidelines.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.