Global Economic Commentary | January 22, 2026

Jet-Lagged Recovery

The global economy begins 2026 jet-lagged but moving forward.

Long trips rarely end at the airport. We arrive, but our internal clocks lag behind; the first day back is spent acclimating to the new landscape. The global economy enters 2026 in much the same way. Shifting rules of commerce, political stoppages and patchy data have left decision makers disoriented. The dataflow is returning, but it may be a while before we feel settled.

Major economies are advancing, but not in sync. Resilience carried economies through persistent uncertainty last year, and that quality should endure. Central banks are nearing a steady state, but conditions are unsteady. Renewed trade confrontations – like the recent threat tied to Greenland – would deepen that misalignment and harden fragmentation at a delicate moment.

Following are our thoughts on how top markets are faring.

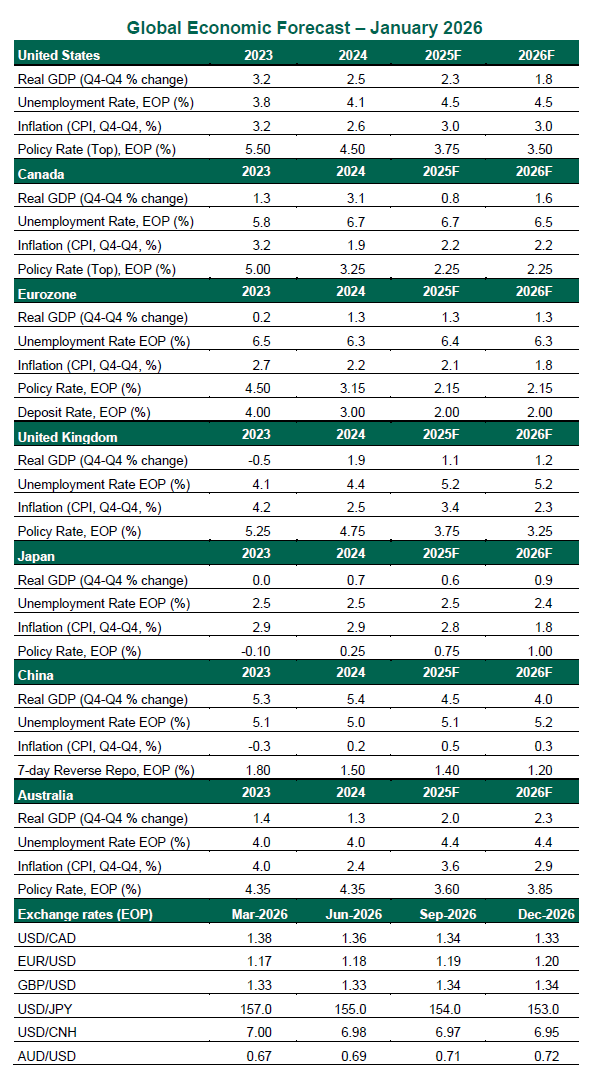

United States

- The U.S. economy is still feeling the effects of a record federal government shutdown, which disrupted key economic data releases. Consumption indicators, including the Fed’s preferred inflation gauge, remain delayed and will not normalize until March. Even so, we still hold the view that growth remains robust: the labor market has settled into a slower but stable equilibrium, tax refunds should provide near‑term support, and housing affordability proposals are gaining traction. While policy uncertainty has diminished to a degree, a return to calm remains unlikely.

- Inflation has eased, with the core measure steady at 2.6% year over year in December, down from 3.0% in September. Data distortions are suppressing this figure, creating uncertainty. The Fed cut rates by 25 basis points in December to a 3.50%-3.75% range, but the messaging underscored growing policy complexity. We expect one additional cut in the first half of the year, followed by a prolonged pause. Questions about Fed independence are likely to remain in focus but will not alter policy outcomes in 2026.

Canada

- Canada enters 2026 with recession risks reduced, but external uncertainty remains paramount. Higher United States-Mexico-Canada Agreement (USMCA) compliance and selective U.S. tariff exclusions have eased the terms of trade somewhat, lowering the likelihood of a downturn. Even so, the economy remains heavily exposed to U.S. trade policy. Industrial production, exports, and business investment are likely to stay subdued in the near term. We expect USCMA renegotiation to result in the removal of most U.S. tariffs by the third quarter, lifting a key drag on activity, but there is also a risk that negotiations prove difficult.

- Canada’s labor market improvement stalled last month, with the unemployment rate rising three-tenths to 6.8%. Emerging slack in the labor market has been contributing to disinflation. Against this backdrop, the Bank of Canada is likely to remain on hold, balancing weak domestic momentum against fiscal stimulus and shifting trade dynamics.

Eurozone

- The eurozone ended 2025 on firmer footing, with growth modestly stronger and inflation back at target. In 2026, activity will start unevenly but should gradually converge. Germany will begin to stir from stagnation while France’s recent strength fades amid persistent political and fiscal strains. Consumption should provide some support amid tight labor markets and accommodative financial conditions, but growth is unlikely to exceed potential. Risks remain skewed to the downside with the transatlantic trade environment once again looking more conditional. Even as tariff pressures have eased, lingering policy uncertainty and structural weaknesses leave European industries exposed to renewed trade frictions.

- With inflation subdued and activity steady, the European Central Bank is expected to remain on hold through 2026. Geopolitical shifts, including a more assertive U.S. posture, may accelerate debates around European defense. Higher security spending would have implications for the bloc’s fiscal outlook.

United Kingdom

- Data released around the turn of the year reinforced the downbeat tone that prevailed through late 2025. The U.K. economy has been kept afloat by the public sector, with government consumption and investment providing the bulk of recent growth. Current spending plans imply that this support will continue into 2026. The outlook for the private sector remains fragile: a sharp deceleration in real income growth and weak corporate profitability are likely to limit any meaningful pickup in private demand. Taken together, we expect another year of subdued growth. Britain’s political situation and public finances remain fragile. The back-loaded nature of measures announced in the Autumn budget has not fully restored credibility in the fiscal framework, leaving the risk of renewed market volatility in the run‑up to the next budget elevated.

- A softening economy is reinforcing disinflationary pressures. Inflation expectations appear to have peaked, and data point to a continued loosening of the labor market. The unemployment rate has drifted higher in recent months, alongside slowing private‑sector pay growth. All of this has strengthened the case for further easing from the Bank of England. We continue to expect two more cuts during the first half of the year.

Japan

- Japan’s real gross domestic product contracted 0.6% on a quarterly basis in Q3, reflecting broad‑based weakness across domestic demand and exports. Consumption should recover as real incomes improve. Headwinds from high U.S. tariffs and trade‑policy uncertainty are likely to fade in the second half, supporting exports and machinery investment. Political frictions with China have risen following comments by Prime Minister Takaichi on Taiwan. Further escalation is not our base case, but any deterioration would be disruptive for Japanese industry and could weigh on bond yields and the yen.

- Prime Minister Takaichi’s announcement of a February 8 snap election has unsettled markets, rekindling concerns about looser fiscal policy and renewed downward pressure on the yen. With headline inflation likely to dip below 2% in coming months due to negative food price base effects, the Bank of Japan (BoJ) is expected to hold policy steady for now. But persistent currency weakness, if reinforced by post‑election fiscal expansion, will have implications for BoJ policy. For now, we expect the central bank to hike following Shunto wage negotiations, with risks titled toward one additional increase later in the year.

China

- China met its “around 5%” growth target in 2025, helped by strong first‑half momentum that offset a softer finish to the year. Exports have continued to surprise to the upside, supported by resilient global demand and trade rerouting. Manufacturing indicators are pointing to sustained industrial momentum. The external outlook remains relatively constructive as supply chain reconfiguration continues to favor Chinese producers. Rising geopolitical tensions and expanding trade and investment frictions beyond the U.S. pose downside risks.

- Domestically, conditions are less supportive. Persistent weakness in domestic demand in the second half of 2025 is likely reinforcing low inflation expectations among both households and corporations. Weaker retail data reflects slower auto sales and the fading impact of consumer trade‑in programs amid funding constraints. Property market woes persist. We expect policy support in 2026 to remain measured rather than forceful. Policy will likely aim to stabilize activity, rather than deliver a significant growth impulse.

Australia

- Activity in Australia has firmed, with both household consumption and business investment picking up. Consumption has been supported by rising real disposable incomes, reflecting interest rate cuts, tax relief, cost‑of‑living measures, solid wage growth, and a still‑tight labor market. Business investment is beginning to recover, led by a surge in data center construction. Momentum is building toward stronger growth in 2026.

- Recent inflation readings have edged higher, drifting away from the midpoint of the 2%–3% target band. Last year’s monetary easing contributed to accelerating house prices, further complicating the policy outlook. Firm growth, low unemployment and elevated labor costs all act to raise the risks of renewed inflation. Rate cuts are now off the table for 2026, and we expect the Reserve Bank of Australia to raise rates in the second quarter before moving to the sidelines.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.