US Economic Outlook | June 23, 2026

Tug Of War

The U.S.-Iran deal reduces downside risks but doesn’t change the broader trajectory.

The U.S. economy is being pulled in competing directions. A temporary easing in geopolitical tensions has steadied sentiment, but tariff uncertainty is re-emerging as a headwind. Inflation remains mixed, with elevated headline readings but contained core pressures. Markets have shifted their expectations of Fed policy from easing to potential tightening.

AI-led investment remains a key source of support, but it hasn’t translated into a broad-based momentum. The economy is still advancing unevenly, with strength in one area offset by softness in another. The U.S.-Iran deal reduces critical downside risks but does little to change the broader trajectory.

Following are our thoughts on the outlook for the domestic economy.

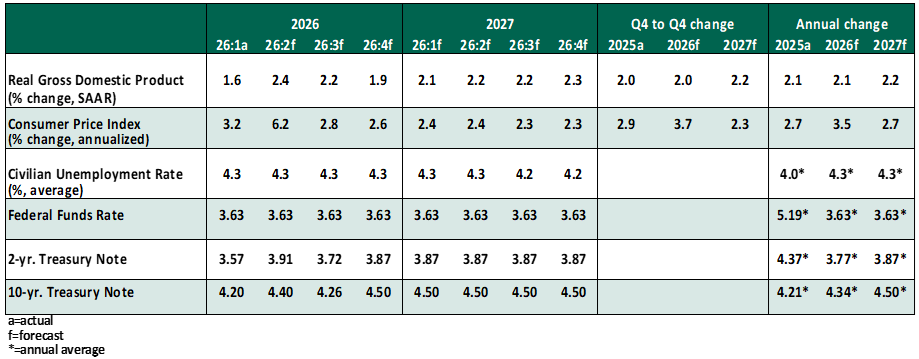

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- U.S. economic momentum remains resilient, even as growth in much of the world slows. Looser fiscal policy and an AI-driven boom in business investment are key drivers of activity. There were signs that higher energy costs were beginning to bite into household spending, yet the latest retail sales data highlighted the continued resilience of consumers. The U.S.-Iran truce has reduced the risk of further dislocations, with falling gasoline prices helping to support consumption.

- The labor market remains a central pillar of this resilience, with conditions still very much consistent with a healthy expansion. The May employment report showed little sign of stress, as payrolls rose by a stronger than expected 172,000, alongside upward revisions of 93,000 to the prior two months. Gains were led ng food and energy) edged up modestly to 2.9%, suggesting that second-round effects remain contained for now. With energy costs now declining, inflation should follow. But a return to the central bank’s target is unlikely anytime soon, given persistent price pressures in areas such as housing and AI-related infrastructure.

- The Fed, under new Chair Warsh, left the Fed Funds Rate unchanged in June. The Federal Open Market Committee (FOMC) post-meeting statement was notably pared down, with its forward guidance largely removed. However, it acknowledged that inflation remains elevated, partly due to supply shocks, and reiterated its focus on delivering price stability. Though the meeting had a hawkish tone, we think the Fed has room to remain on the sidelines, assessing whether inflation pressures broaden. Combined with a steady labor market, policy is likely to stay on hold for longer, with risks tilted toward further tightening rather than easing.

- Chair Warsh announced five new task forces to reevaluate the FOMC’s approaches to policymaking. Reforms to practices like the press conference are likely but will be studied and communicated in advance.

- Trade policy is re-emerging as a key source of uncertainty. President Donald Trump has signaled he does not intend to reauthorize , the North American free trade agreement. Rather than expiring, the pact would shift to annual reviews for up to a decade unless a country formally exists.;While full termination appears unlikely, uncertainty alone could be nearly as damaging for business, trade, and investment plans.

The U.S. administration has also revived its tariff agenda, with the Office of the U.S. Trade Representative proposing levies of up to 12.5% on 60 trading partners over forced labor, with limited scope for legal challenges. Taken together, the renewed tariff push reinforces that the external environment is unlikely to be smooth, adding another layer of risk to the outlook through this year and into 2027.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.