US Economic Outlook | March 19, 2026

Watching The Smoke

The Middle East war has tilted risks toward weaker growth and persistent inflation.

“Smoke on the Water, Fire in the Sky,” the iconic Deep Purple refrain, endures because it captures a familiar dynamic: threats appear on the horizon before the heat arrives.

The momentum of the U.S. economy is positive, but a new haze is rolling in from abroad. The escalation of the Iran war has reintroduced energy price volatility and heighted levels of uncertainty. This has titled the balance of risks toward weaker growth and persistent inflation, complicating the Federal Reserve’s calculus.

The U.S. is a net exporter of petroleum and natural gas, making it far less vulnerable to supply disruptions than many of its peers. But geopolitical tensions in the Middle East are beginning to seep into the U.S. outlook indirectly, through higher energy prices, tighter financial conditions, and a more fragile external backdrop. While these influences remain secondary to domestic drivers, a longer conflict could strengthen those headwinds.

We are not materially altering our growth outlook, but a prolonged or escalating Middle East conflict will raise downside risks. Following are our thoughts on the currents coursing through the U.S. economy.

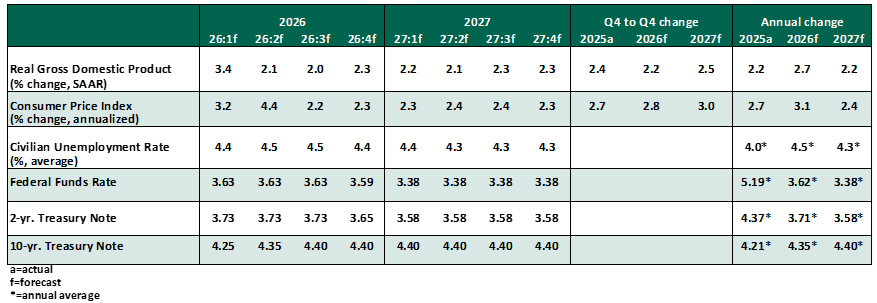

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

Oil prices have risen sharply since late February, creating a renewed headwind to real income growth and increasing downside risks to consumer spending at a time when the labor market is already soft. While higher energy costs complicate the outlook, they are not enough to derail the expansion on their own. Consumer spending should persist, supported by ongoing real income gains, still‑healthy household balance sheets and larger tax refunds.

Business investment will remain a key growth pillar, led by spending on artificial intelligence-related infrastructure. Heightened uncertainty could, however, weigh on capex decisions.

Headline consumer price index (CPI) inflation held steady at 2.4% overall and 2.5% core (excluding food and energy) for the year ending in February. By contrast, the Fed’s preferred inflation measure, the personal consumption expenditures price index, has increased by 3.1% on a core basis in the year to January.

The pass‑through of higher oil and gas prices will likely cause headline inflation to jump above a 4% annualized rate. Further out, we expect energy markets to settle at more stable levels, below recent peaks but modestly above pre‑war norms. This would allow disinflation to resume. But the risk of persistence has increased, given still‑elevated services inflation and the possibility that supply disruptions last longer than assumed in our base case.

Labor market rebalancing remains orderly, but the margin for further cooling without broader weakness is narrowing. Hiring momentum has eased, with an anomalous loss of 92,000 jobs in February. Job openings rose in January, reversing two months of decline, but not enough to put upward pressure on wages. Layoffs remain contained, and unemployment has increased only modestly, implying companies are still reluctant to shed labor aggressively. The U.S. labor force has declined by over 1 million persons since the start of the year, partly as a byproduct of more rigid immigration policies.

The labor market remains a stabilizing force amid an uncertain outlook, but it also represents a key channel through which a sharper confidence shock could propagate more broadly.

The Federal Reserve left the policy rate unchanged this week. But developments in the Middle East have made the Committee “attentive to the risks to both sides of its dual mandate.” Upside inflation risks are colliding with downside pressures to growth and employment, reinforcing the case for patience on rate cuts. Tighter financial conditions and elevated geopolitical risk argue against additional tightening. We continue to expect one rate cut in 2026, but we are positioning it late in the year.

Tariff uncertainty is resurfacing, even if it has slipped from the top headlines. Following the imposition of Section 122 tariffs, the reopening and expansion of Section 301 investigations signal an effort to preserve the existing tariff wall. The transition will renew concerns around goods prices and industrial activity.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.