Weekly Economic Commentary | January 23, 2026

Are Bubbles Brewing?

Investors must learn to manage through bubbles and corrections.

By Carl Tannnenbaum

We got a chance to visit our grandson during the holiday season. To give his parents a break, I took bathtime duty one night. At the end, I was soaked and exhausted.

The little guy loves bubbles in the tub. Bubbles in the financial markets aren’t nearly as amusing. When they burst, the consequences can be immense. But diagnosing bubbles is very difficult to do, and it isn’t clear what can be done to prevent them. As we watch asset valuations stretch further and further, it’s worth refreshing understandings of how bubbles form, and how policy has attempted to deal with them.

The seminal text on bubbles is “Extraordinary Popular Delusions & the Madness of Crowds,” written by Charles McKay in the middle of the 1800s. It illustrates the role that information and psychology play in building market excesses. The examples cited by McKay—which centered on Dutch tulips, South Seas real estate, and the early development of North America—may seem ancient, but the drivers behind them are very much present today.

Bubbles are a product of behavioral economics.

Classical economics suggests that information is readily available, and is assimilated quickly and accurately. Reality is not that neat: the discipline of behavioral economics has consistently demonstrated that human beings are prone to a series of biases and miscalculations.

In the present day, there is an overwhelming amount of information (and misinformation) that reaches us, too much for most people to process. In situations like these, we often fall into herd behavior. We think that others, or the market collectively, know something that we should. We follow along, driven by a fear of missing out (FOMO). Confirmation bias leads us to place more weight on news that is aligned with our positions, and to discount contradicting ideas and warning signs. The greater fool theory can be used to justify buying assets that are likely overvalued.

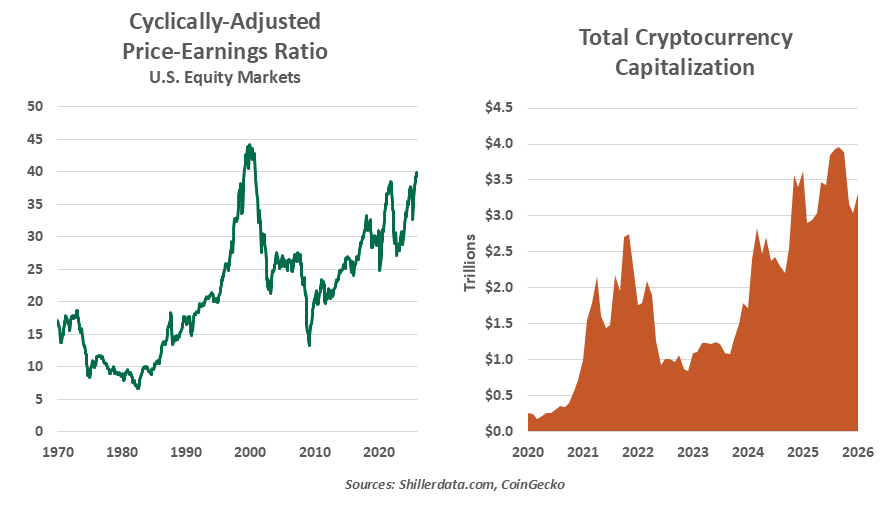

This makes us vulnerable to what Alan Greenspan called “irrational exuberance” in a 1996 speech. That phrase became the title of a book by Nobel Laureate Robert Shiller, who has devoted his career to studying financial excesses. Shiller and his collaborators have constructed measures of asset prices that are intended to identify periods of stress; one of them, a cyclically-adjusted price-to-earnings ratio, is nearing the peak set during the Dot-Com bubble 25 years ago.

In another arena, cryptocurrencies have reached new peaks. According to CoinGecko, there are more than 19,000 of them trading actively, with a market capitalization of over $3 trillion. More than 20% of Americans and Britons own them, despite extreme volatility in their values.

Artificial intelligence (AI) may prove transformational, and the technology companies developing it are attracting justifiable interest from investors. Similarly, the expansion of digital payments will increase demand for digital currencies that can be used on digital ledgers. The question is whether all of the assets in these two spaces are worthy of the valuations currently assigned to them.

Even the best investment professionals struggle with this question. AI and digital currencies are new innovations whose capitalization cannot easily be benchmarked against past precedents. Portfolio managers are vulnerable to their own biases and client demands, which may lead them to be more fully allocated to these markets than is optimal.

Bubbles are very difficult to diagnose, and even harder to recover from.

Speaking in the wake of the Dot-Com crash, Ben Bernanke (who had just joined the Fed’s Board of Governors) gave a speech on how policy makers might address potential bubbles. He argued that diagnosing them was a fool’s errand, and that using interest rates to combat them carried risks to the economy.

Instead, he pressed for a macroprudential approach in which financial supervision ensured that the system was resilient enough to handle a shock. Bernanke succeeded in implementing this concept after the Global Financial Crisis; today, however, oversight of the financial system is in retreat.

About a third of those surveyed recently by Oxford Economics think that AI-related stocks will face a correction in the next twelve months, which could precipitate a broader sell-off. Having experienced the 2008 crisis from inside the Fed, I am loath to go through anything like that again. If I am going to get soaked, I would prefer it to be at the hands of my grandson.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.