- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | May 22, 2026

Bank Deregulation Taking Shape

Will easier regulations make bank loans more competitive?

By Ryan Boyle

This week marked the passing of former Massachusetts Congressman Barney Frank. His signature legislation, the Dodd-Frank Act of 2010, was the most recent increment in a long-running history of tighter financial regulation. Some of those rules are now coming under scrutiny, with the goal of making bank lending more competitive.

Classically, banks collect deposits and use them as the basis for loans. Fractional reserve banking allows banks to issue a volume of credit that exceeds the funds they take in. This leverage is a vital resource for economic growth, but leaves banks exposed to credit cycles and deposit flight.

Tremors in the banking sector have led to more regulations throughout the industry’s existence. In the U.S., the Office of the Comptroller of the Currency (OCC) was chartered in 1863 to create a uniform national currency and set of bank standards, followed by the Federal Reserve Bank (FRB) System in 1913 and Federal Deposit Insurance Corporation (FDIC) in 1933. Each took steps to reduce bank runs and other crises, but none could mitigate every risk.

The most recent tranche of regulations came after the Global Financial Crisis (GFC) of 2008. Easy lending standards contributed to the spread and severity of the crisis. The Dodd-Frank Act included restrictions on banks making speculative investments and added to banks’ capital requirements. Like previous responses to crises, these regulations improved the safety and soundness of the banking sector, but at the expense of limiting credit extension.

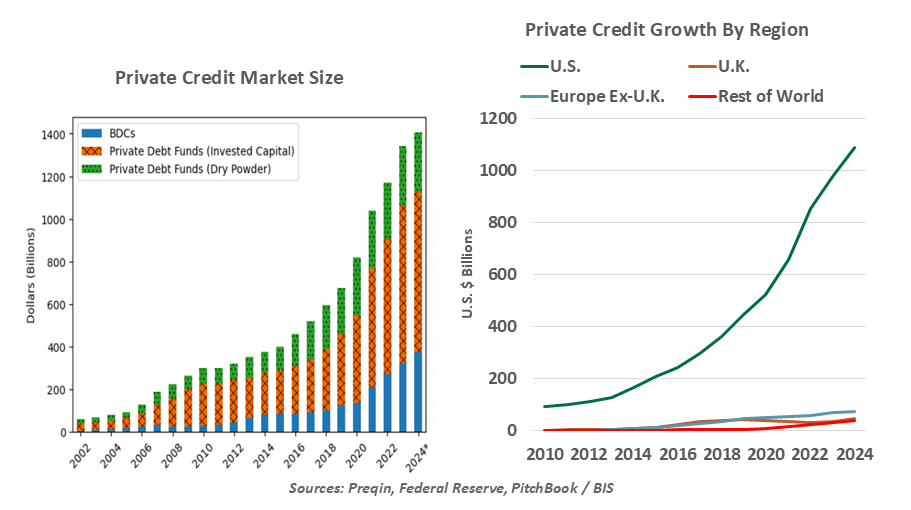

Higher reserve requirements made banks less willing to issue loans, especially to higher-risk firms, but demand for debt did not go away. Instead, markets created new funding channels. Private credit funds have grown rapidly over the past decade, now estimated to total $1.6 trillion in loans and unused capital. These funds have advantages over banks in their speed and flexibility. Loan approval and funding happen quickly, and loan terms can be renegotiated if conditions warrant. However, loans are priced to reflect a broader spectrum of risk; private loans are estimated to charge interest rates at roughly double the spread to benchmark rates that banks charge.

A new generation of Federal Reserve leadership is open to easing some of the regulatory burden. Vice Chair for Supervision Michelle Bowman has laid out a plan to modify the “four pillars” of bank capital: stress testing, leverage ratios, risk-based capital requirements, and the surcharge for systemically important banks. In recent comments directly addressing the rise of private lending, Governor Bowman proposed a reduction in capital requirements for lower-risk corporate loans.

Advocacy is most prominent from the Federal Reserve, as private credit has grown far more in the U.S. than in any other market. Banks have better retained their lending market share in other developed markets. Regulators abroad have presented more obstacles for non-bank financial intermediaries, and banks have been more willing to work with higher-risk borrowers; in the U.S., banks are less capable of taking larger credit risks.

Private alternatives filled the gap left by cautious bank lending.

Reforms will extend beyond credit. Under Bowman’s direction, bank examiners will apply a higher standard for formal notifications of bank shortcomings. Significant regulatory findings will only be raised where they present clear risk to a bank’s financial condition. She is also advocating to reform the accounting standards to calculate reserves for loan losses. Pressure from the Fed may clear the way to ease these rules, which have been most burdensome for smaller banks.

The FRB, FDIC and OCC are now in a comment period regarding these regulatory proposals. After the window closes June 18, agency leaders may finalize rules in the months to follow. Bank lending could then be less encumbered. Any stimulative effects will take time to appear; capital requirements are not the only reason for banks to take a more conservative lending posture. And any new risks from lighter regulation will be even slower to manifest.

After his time in Congress, the late Representative Frank brought his expertise to the private sector. He served on the board of directors of Signature Bank, which failed in 2023 alongside Silicon Valley Bank. Even for committed reformers, crafting controls that provide the right balance between risk and reward is very difficult.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.