Weekly Economic Commentary | June 12, 2026

Canada’s Economic Woes

Canada’s paths to growth have frozen.

By Vaibhav Tandon

I grew up watching the Looney Tunes cartoons. My favorite gag was when characters would sprint ahead with confidence, only to realize that the ground beneath had slipped away.

The Canadian currency is known as the “Loonie” because one of the country’s favorite birds appears on the dollar coin. True to that nickname, the Canadian economy has shown a touch of Looney Tunes imagery. After sprinting confidently for a number of years, the economy is now in a state of suspense.

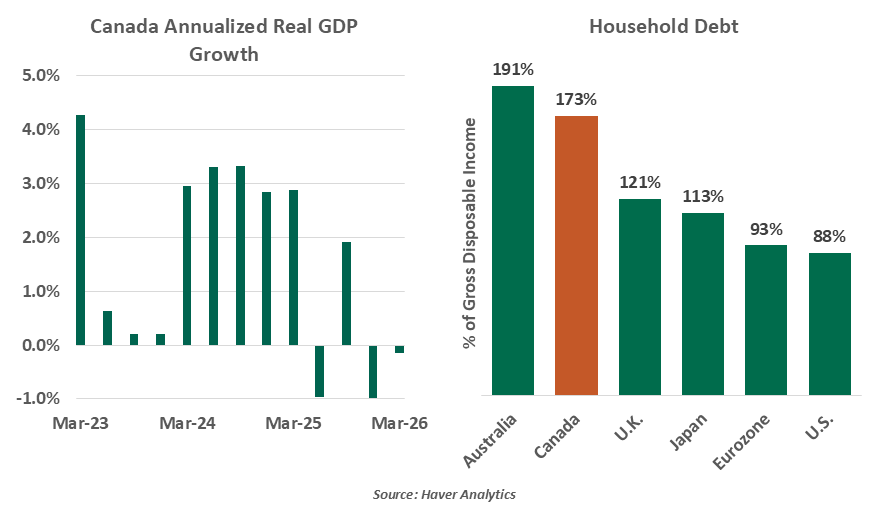

Canada’s real gross domestic product (GDP) contracted 0.1% annualized in the January–March period, marking the second consecutive decline and the third drop in the past four quarters. The slowdown has been broad-based. Business investment has declined for five consecutive quarters. Trade has weakened ever since the 2025 inauguration of President Trump and the rollout of new U.S. tariff policies. The labor market has been loosening, signaling softer demand, even as personal consumption has shown some resilience. At the same time, the Middle East-driven energy shock has added another layer of costs for consumers.

Housing, once a pillar of strength in Canada, is no longer providing the same support. Prices have declined steadily and now sit about 20% below their post-pandemic peak. For households already carrying elevated debt burdens, the housing slowdown comes at an inopportune time. While the debt service ratio for Canadian consumers has eased, households still held $1.73 in debt for every dollar of disposable income at the end of last year. This overhang is likely to constrain consumer spending, with knock-on effects for the labor market.

Population growth has long been a key driver of Canada’s economic cycle. Estimates suggest that a one-percentage-point decline in population growth reduces potential GDP growth by roughly the same margin, all else equal. Tighter immigration policy led the population to contract last year, and it is set to decline further as non-permanent residents depart. Unless immigration policy shifts meaningfully, this engine of growth will be stuck in reverse.

That said, the picture isn’t entirely bleak. Labor market data offered a welcome surprise in May, with job gains of 88,000 following four months of cumulative losses. The unemployment rate edged down three-tenths to 6.6%, helping to steady recession concerns for now.

Fiscal policy is turning more supportive. The 2026 Federal Spring Economic Statement introduced measures worth roughly 1.2% of GDP for the next five years, aimed at cushioning the burden of higher energy costs and sustaining consumption. Programs like the Canada Groceries and Essentials Benefit and the temporary suspension of fuel excise taxes should also provide relief, though the bulk of the impact may not be felt until the third quarter.

Canada’s old growth engines are now becoming its key vulnerabilities.

Housing-related measures like tax adjustments and the planned cut to municipal development charges will help stabilize construction activity, but are unlikely to drive a swift turnaround. Modest job growth alongside fiscal support will underpin demand and provide a floor to house prices.

For its part, the Bank of Canada is keeping its options open. Interest rates were held steady at this week’s meeting, but could move in either direction as geopolitical risks and trade developments unfold. With inflation likely to remain contained, an extended pause with policy in neutral territory remains the most likely path, setting it apart from some of its peers.

Canada is not in an economic downturn, at least not yet. But the economy is struggling, and the conditions that could tip it into a genuine downturn are present. These include a potential breakdown in the North American trade pact.

Unlike my favorite cartoon chases, the Canadian economy hasn’t lost its footing. There is still some ground underneath…for now.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.