Weekly Economic Commentary | March 13, 2026

China's Exposure To The Persian Gulf

Deeper partnerships create deeper fault lines.

By Vaibhav Tandon

China has relied heavily on exports to help underpin growth. That strategy, however, rests on a narrow set of implicit assumptions. One of these is uninterrupted access to energy supplies and shipping corridors far beyond the country’s borders. The war in the Middle East risks bringing that dependency into sharper focus, given the region’s central role in China’s energy security.

For now, China has been largely shielded from the immediate shocks from the conflict. But the spillovers are likely to build.

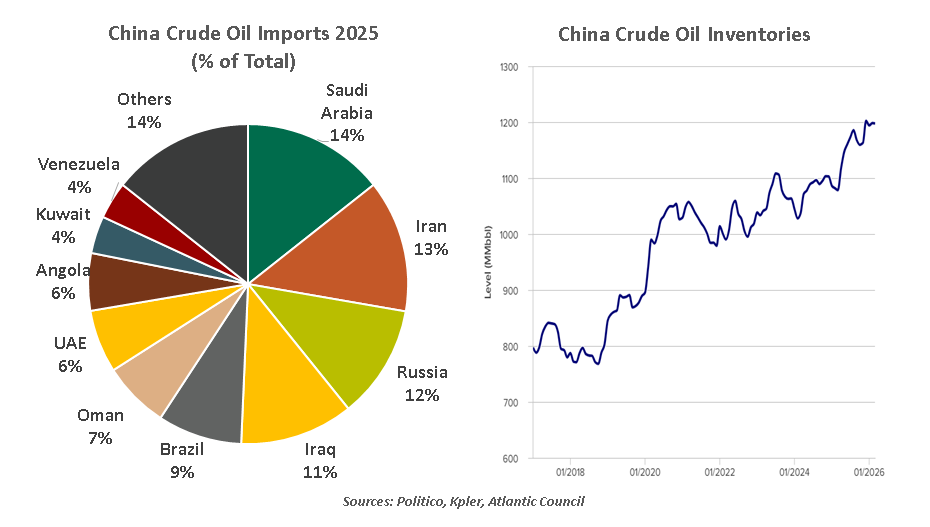

As the world’s largest importer of crude oil and liquefied natural gas, China is among the most exposed major economies to a prolonged energy shock. It sources around half of its oil supplies and around a third of its liquefied natural gas (LNG) from Saudi Arabia, Iraq, the UAE, Oman and Qatar. China is also the principal buyer of sanctioned Iranian crude oil, which is estimated to account for 13%-15% of its total crude imports.

The longer the fighting lasts, the greater the risks for China.

China is relatively well placed to absorb the initial shock. Years of aggressive stockpiling have left it with an estimated 1.2 billion barrels of crude in onshore reserves, equivalent to up to four months of import demand. This substantial buffer would help delay rationing or widespread disruption. China can further increase purchases from Russia, its largest source of crude. Beijing has also pre-emptively ordered refiners to curb fuel exports to preserve domestic supply.

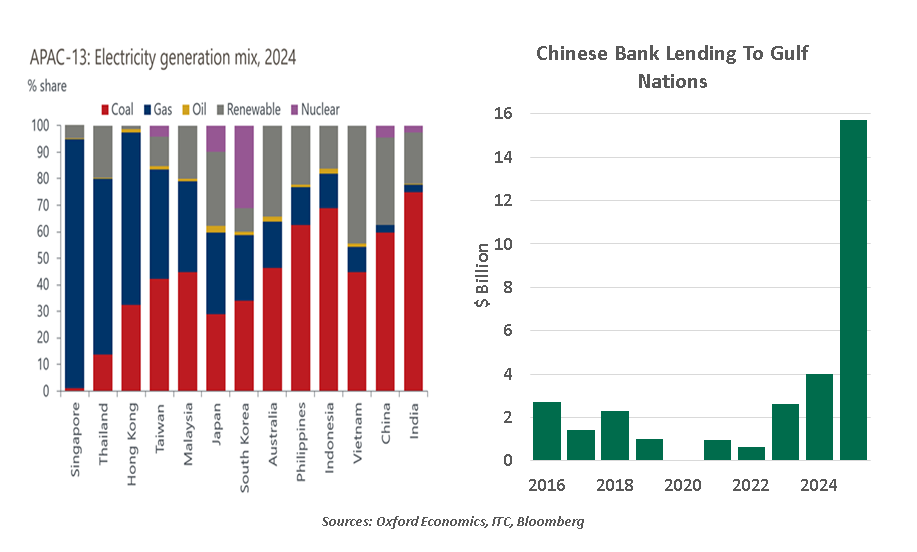

China’s broader energy mix offers additional insulation. Although China imports around a quarter of its LNG from Qatar, natural gas plays a smaller role in its industrial base than in many peer economies. Coal and renewables are the backbone of its power systems, with oil and gas accounting for only about 4% of its electricity generation, far below the 40%-50% share seen across much of Asia.

That said, a prolonged disruption in the Strait of Hormuz raises the risk of physical shortages that could weigh on industrial activity and supply chains. While Iranian barrels could be replaced over time, other Gulf dependencies would be far harder to offset.

To soften the blow on households, China has already raised its regulated fuel price caps. While administered prices help cushion consumers, the adjustment ultimately shifts the burden onto fiscal balances and eventually to corporate margins. Second‑round effects such as higher transport costs, elevated shipping insurance premiums and pressure on fertilizer markets are also on the horizon. Energy‑intensive sectors such as chemicals would be among the most exposed to volatility in crude prices, while fertilizer shortages would pose additional risks across food supply chains.

Over time, the stress would extend beyond energy into exports, investment and credit. A disruption lasting several months would take a severe toll on global consumption, compressing demand for Chinese goods. That environment would weigh directly on China’s external performance at a moment when export resilience is already being tested.

China’s widening global footprint adds to further indirect exposure. The Middle East has assumed greater significance for China in the wake of its trade confrontation with the United States. The UAE has emerged as the fastest‑growing destination for Chinese auto exports. Demand for Chinese steel has also surged across the Gulf, led by Saudi Arabia. Taken together, China’s exports to the six Gulf Cooperation Council (GCC) nations expanded at twice the pace of its shipments to the rest of the world in 2025.

China has a lot riding on the Gulf.

Investment and financial links are deepening in parallel. Heightened scrutiny of Chinese funds in major economies has pushed capital flows toward the Gulf as an alternative destination. Between 2019 and 2024, China invested close to $90 billion directly into the region and is the leading foreign investor in critical areas such as desalination. Chinese capital is increasingly involved in financing, building and operating infrastructure, power grids and petrochemical facilities across the Gulf.

The Middle East now accounts for roughly 10% of China’s global stock of overseas loans and grants. Chinese banks extended a record $16 billion in loans to GCC economies last year, marking a near four‑fold increase from around $4 billion in 2024. Some of these credits may be at risk if the conflict continues on.

All of this comes as China’s leadership recalibrates its economic ambitions. At the recent National People’s Congress, Beijing set a 2026 growth target of 4.5%–5.0%, the lowest in more than three decades. This is being seen as a tacit acknowledgement of diminishing returns from traditional growth drivers. A sustained Middle East war that pushes input costs higher and drags on global demand would complicate efforts to stabilize growth even at this reduced pace, especially given China’s limited policy flexibility and its continued reliance on supply side stimulus.

The longer the Middle East war persists, the more it will start eroding the very assumptions that have allowed exports to sustain economic momentum: stable energy inputs, reliable logistics and healthy external demand. China may have buffers to absorb the initial shock, but it cannot stockpile its way out of a sustained disruption.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.