Weekly Economic Commentary | April 10, 2026

Currency Concerns

Questions about the U.S. dollar are becoming more frequent.

By Carl Tannenbaum

To maximize my spending power when I travel internationally, I arrange to have the U.S. dollar increase in value against the currencies of the countries I will be visiting. Don’t ask me how I do it: you don’t want to know.

I was overseas for two weeks last month, and the dollar was pretty strong during that interval. But its standing wasn’t attributable to any manipulation on my part. During the fortnight in the United Kingdom and Ireland, I got a lot of questions about the dollar’s status; here are a few of the most frequently-asked, along with the responses I provided.

1. How has the conflict in the Middle East affected the dollar?

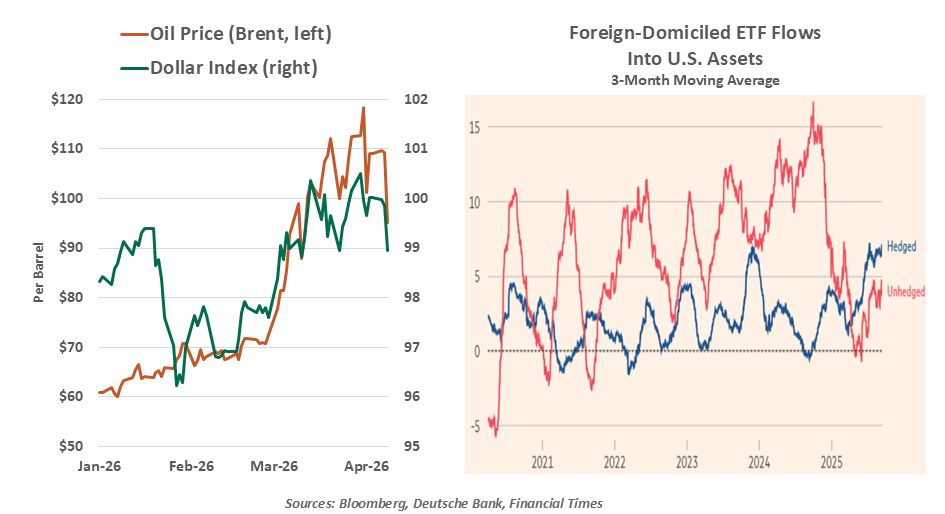

The dollar has gained strength in the last five weeks. A significant driver has been its role in global energy markets. The correlation of the dollar and oil prices is variable, but it has been very strong since the end of February.

The dollar remains the primary currency used to trade crude oil, accounting for about 80% of transactions worldwide. In recent years, sanctioned countries such as Russia and Iran have been selling oil in non-dollar currencies, with the Chinese yuan most prominent. China would certainly like to increase the share of global sales that are denominated in yuan, but that currency isn’t as fluidly traded as the dollar is.

2. Some countries are reducing their dollar reserves. Does that reflect a loss of confidence in the United States?

Russia and China, once significant holders of U.S. dollar reserves, have reduced those positions over the past decade. The primary motivation has been to limit their vulnerability to sanctions that would restrict access to those resources. Fortunately for the United States, other countries have picked up the slack by increasing their holdings of U.S. debt.

There have been recent reports of dollar selling by countries seeking to bolster their local currencies. India has been in the forefront here. These efforts reflect a desire to preserve purchasing power, not to reduce exposure to the dollar.

Overall, the dollar’s share of global central bank reserves has been stable, and it is double the share of its closest competitor.

3. Have recent global frictions caused international investors to reconsider their holdings of dollar-based assets?

My previous trip to Europe coincided with the “Liberation Day” tariffs. Across countries, I was challenged to explain exactly what was so liberating about them. And I was also challenged with questions about the wisdom of allocations to dollar-based assets.

Fortunately, the trajectory of tariffs moderated during the balance of 2025. The performance of U.S. markets remained strong. With very limited exceptions, global investors have maintained their holdings of U.S. assets. There has, however, been more interest in hedging the currency risk of the dollar, which has weighed on its value.

Despite concerns, investors haven’t dumped dollar assets.

4. Longer-term, is the dollar at risk of losing its status as the reserve currency?

The U.S. national debt is large, and policy makers may allow higher inflation to devalue it. This would debase the currency. The volatility of American policy setting has also been a source of concern for domestic and international audiences. To some, the bedrock underneath U.S. markets is cracking.

These points are not to be dismissed. But the question remains: what currency stands ready to assume the mantle of leadership? None stand out. And as a result, measures of the dollar’s role in world markets do not reflect any warning signs.

Of course, I am kidding about my power to manipulate exchange rates. If I had that ability, we would publish my travel schedule for clients to use in trading currencies.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.