Weekly Economic Commentary | June 5, 2026

Fertilizer and Food

A break in fertilizer supplies will be felt around the world.

By Vaibhav Tandon

“As you sow, so shall you reap.” The phrase works as a life lesson, but also holds on the literal level: what a farmer plants determines the harvest. But the outcome is shaped just as much by inputs to the growing process. Shortages of those inputs are sowing inflation that will be reaped at the checkout counter later this year.

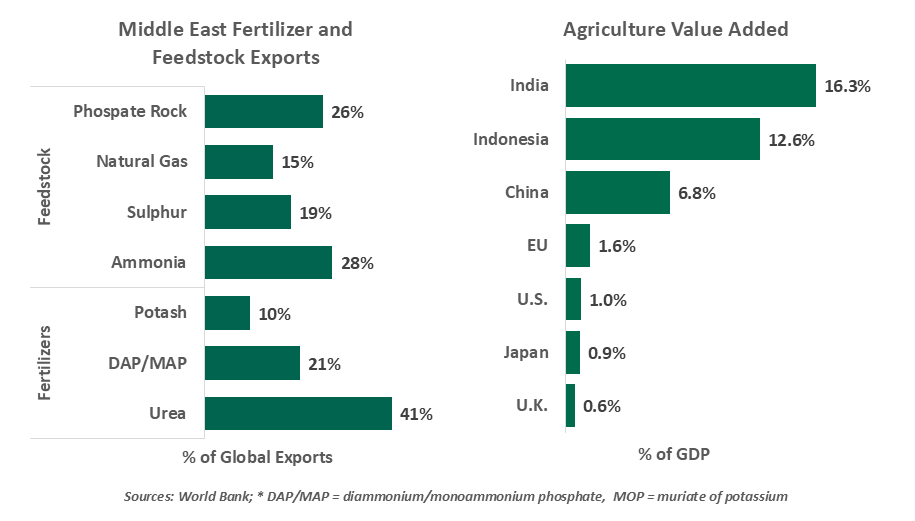

Fertilizers sit at the center of this transmission mechanism. As much as a third of the global supply of these commodities passes through the Strait of Hormuz, which has largely been closed for three months. This has triggered shortages and a price spike: the World Bank’s fertilizer index rose over 12% in the first quarter of 2026, reaching its highest level since October 2022.

The timing is particularly sensitive across key agricultural regions. In North America, spring planting is underway. In Asia, especially India, the growing season is now beginning, while European farmers are making input decisions for the summer. Industry estimates suggest the EU corn planting area could fall below 8 million hectares in 2026 for the first time this century, reflecting rising input costs, weak margins and growing climate risks. The Food and Agriculture Organization estimates that cereal production may be 5% lower in 2026, and may not regain last year’s levels for some time.

Economies that are heavily dependent on fertilizer imports and areas where agriculture constitutes a larger share of output are particularly exposed. India imports up to 30% of its urea and diammonium phosphate. Agriculture also makes up about 17% of India’s gross domestic product (GDP), amplifying the macro impact of input shocks. By contrast, advanced economies like the United States are far less vulnerable. Agriculture represents less than 1% of GDP and domestic fertilizer availability is relatively ample.

Today’s input shock is tomorrow’s food price inflation.

Food is a critical economic and political issue. Public anger over the availability and cost of their daily bread has toppled regimes through the centuries, peacefully and not so peacefully. It is not surprising that policy responses to the fertilizer crisis are already visible. Asian governments like India and the Philippines are using subsidies and diversifying imports to avoid stress. Australia has provided public funding, offering loans and insurance support for private fertilizer imports.

European policymakers have responded with a Fertilizer Action Plan, which aims to safeguard the bloc’s food security by mixing immediate financial relief for farmers with long-term initiatives to reduce import dependencies for fertilizer. The European Union also intends to use its budget to boost agricultural reserves and roll out a support package before summer to provide liquidity ahead of the next production cycle.

Buffers do exist. European and American farmers entered this period with some inventories of fertilizer already secured. But these are temporary. Unlike oil, fertilizer markets lack large scale strategic reserves, limiting the ability to smooth prolonged disruptions. China, one of the world’s top fertilizer producers, has banned exports ahead of the spring planting season.

Even if the Strait of Hormuz were to reopen, the effects of today’s constraints will echo into future harvests. According to Oxford Economics, it typically takes around two and a half years for commodity prices to normalize after a shock. Weather dynamics are adding another layer of stress, with a potential super El Niño on the horizon. Heatwaves across several key growing regions could further amplify the impact of higher input costs, tightening the balance between supply and demand.

The fields may seem distant, but the impact will not be. What is being sown today will define the next harvest, and soon, the trajectory of inflation.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.