Weekly Economic Commentary | May 1, 2026

India's Growth Story Meets a Boundary

Supply shocks will sting the subcontinent.

By Vaibhav Tandon

India has been the fastest‑growing major economy in recent years, supported by steady expansion, contained inflation and relative policy flexibility. What until recently looked like a comfortable innings now demands far more careful shot selection, with fewer easy runs.

The Middle East conflict risks shifting India’s economy from playing on a flat field to navigating hazards in the forms of higher energy prices, supply disruptions and a more adverse external backdrop.

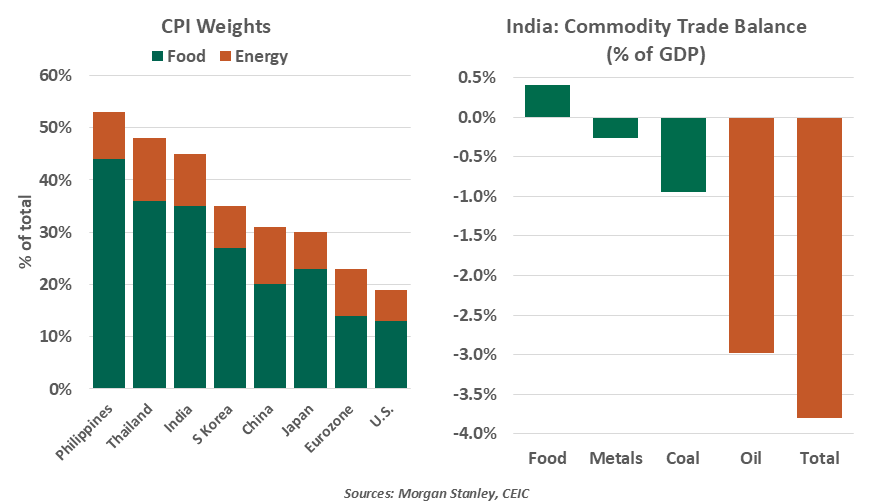

This vulnerability is most evident in India’s energy linkages. As the world’s third largest oil consumer, India imports roughly 90% of its needs, with over 40% sourced from the Middle East. The country is highly exposed to price spikes and supply disruptions. Oil is the primary channel, but not the only one: around 60% of natural gas and more than 90% of liquefied petroleum gas imports also originate from the region. Qatar, where energy infrastructure has been affected, has been a key supplier.

Compared with peers, India’s limited inventory buffers deepen this exposure. Japan’s stockpiles cover roughly 254 days of consumption, South Korea’s about 208 days and China’s around six months. India, by contrast, began with less than two months of reserves. With fossil fuels accounting for about 80% of its energy mix, India has limited scope to cushion the shock through diversification.

Higher energy prices would raise costs across fuel, transport and power, feeding into the costs of food, logistics and manufacturing. This is particularly consequential given India’s inflation profile, where food and energy together account for roughly 45% of the consumer price basket.

In India, food inflation is often the channel through which shocks endure. Fertilizers are a key link from global energy markets to domestic food prices. India imports about 85% of its fertilizer supply, making it vulnerable to disruptions. Because production relies heavily on natural gas, any shock to energy markets can quickly constrain availability and push up costs. Combined with the risk of a weak monsoon during the June sowing season, the shock could shift from temporary fuel inflation to something more persistent.

To date, the Iran conflict has not led to a surge in inflation. The government has absorbed much of the shock through cuts to fuel excise duties and the use of export taxes. In natural gas, it has prioritized household consumption over industrial use, effectively shifting an inflation problem into an activity constraint.

That said, these measures highlight a central trade-off: inflation control versus fiscal discipline. Leaning heavily on subsidies and tax cuts can shield households in the short run, but the cost ultimately falls on public finances. A rising fertilizer bill will add to the burden. Public investment has been a key driver of growth in India, in part because private capital expenditure has been subdued. Expanding fiscal support to offset energy shocks risks crowding out capital spending, turning short term relief into a longer term drag on growth.

Energy shock pressures are building for India.

External balances add further strain. Higher oil prices will widen India’s current account deficit. While India’s foreign currency reserves are adequate, they are not unlimited. Remittances, around $136 billion in 2025, could have been an important cushion. However, roughly 40% of India’s external remittances come from Gulf economies. With those countries hit by the conflict, remittance growth may slow, exposing a key income vulnerability.

The currency has also come under pressure. Rising oil prices and a stronger U.S. dollar are weighing on the rupee, which would amplify imported inflation. Persistent weakness is a growing concern for the Reserve Bank of India, given the country’s energy trade deficit, forcing regular interventions since the onset of the war.

The longer the disruption persists, the more inflation, fiscal pressures and external imbalances begin to interact. This risks turning an energy shock into a broader macroeconomic constraint that could shave as much as 1 full percentage point off growth.

In cricketing terms, India has moved from batting on a flat track to a sticky wicket. Even well‑placed strokes are no longer enough to keep the scoreboard ticking over with ease.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.