Weekly Economic Commentary | January 16, 2026

Is Another Great Moderation At Hand?

Today's global conditions do not match the ideal setup of the 1990s.

By Carl Tannnenbaum

I am new to streaming music. So I was surprised when the platform I use offered a year-end summary of my activity. Included was an estimate of my age, based on my listening habits: the app thinks I am 42 years old. When I saw this, I kissed the screen and renewed my subscription for 10 more years.

The calculation was apparently based on my fondness for the music of the 1990s. I also have fond economic memories of the 1990s, an era when technological gains boosted growth and buoyed markets. Some are suggesting that we are on the brink of a repeat performance, but a close examination of the history casts some doubt over this conclusion.

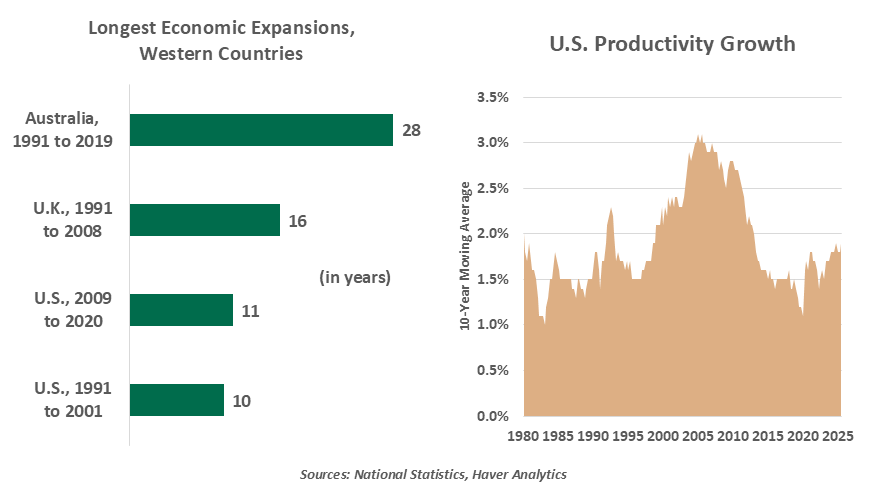

After the tumult of the 1970s, a range of countries enjoyed a series of very long expansions. Starting in 1982, the United States economy grew for 24 out of 25 years. The U.K. enjoyed a similar experience; Australia recorded 28 years of uninterrupted progress. Unemployment rates plunged, and asset prices soared. The period became known as “The Great Moderation.”

A series of factors contributed to these outcomes. Globalization was ascendent during that interval, opening new markets for selling and sourcing. The fall of the Berlin Wall expanded European vistas, and China entered the international trading community. Cross-border investment boomed, accelerating the advancement of emerging markets.

Technology was moving ahead as well, allowing information to travel faster and farther. Just-in-time inventory management, robotics and sophisticated logistics revolutionized manufacturing. The shift to services, which are typically less cyclical, also reduced fluctuations in economic growth.

Traditionally, strong growth and falling unemployment would put pressure on prices. Defying expectations, inflation continued to moderate throughout the 1990s. Productivity growth was central to this outcome; output per hour for U.S. workers grew at an average rate of 2.5% per year for an extended period, a very strong level.

Low and predictable inflation enhanced the clarity of corporate planning and made long-term investment more viable. Borrowing rates, which had carried a burdensome term premium, became more reasonable. Financial innovations further reduced the cost of credit.

Alan Greenspan, the Chairman of the Federal Reserve Board throughout the 1990s, made a very brave decision in the middle of that decade. The U.S. unemployment rate was closing in on 5%, for the first time in 20 years. This prompting fears of overheating and calls for tighter monetary policy. Greenspan resisted, and was vindicated when inflation remained tame even as joblessness fell to 4% at the end of the decade.

The Great Moderation truly was the best of times.

Central bankers were heroes during The Great Moderation. It appeared that their ability to assess and manage the business cycle had reached new heights of precision, to the point where recessions would occur only rarely. New peaks of prosperity seemed possible. Unfortunately, those visions were rudely interrupted by the Global Financial Crisis (GFC). We’ve been trying to recapture the magic ever since.

For the first time in nearly two decades, some see hope for another Great Moderation. We are in the midst of a tech-led investment boom supporting what some think is a transformational technology. The annualized pace of U.S. productivity growth was 5% in the third quarter of last year, well above the long-term average. Markets appear positioned in a way that assumes that this sort of performance will continue for a while.

Embracing this narrative, critics of the Federal Reserve are calling on the central bank to show the same courage that Alan Greenspan did during the Great Moderation and lower interest rates, even though inflation is higher than desired.

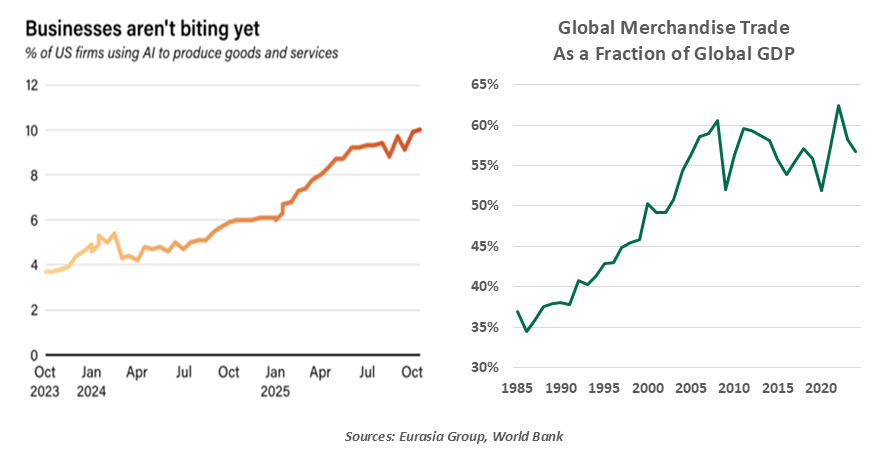

Much as we would love to see another Great Moderation, we do not think one is yet at hand. Recent productivity gains are impressive, but we need to see something more persistent to declare the foundation of a trend. As promising as artificial intelligence is, adoption of AI is still in the early stages; this suggests that AI has not been a major contributor to recent productivity gains.

Further, tailwinds for the Great Moderation are headwinds today. Global trade is stagnating, not expanding, and recent policy actions could ultimately prompt a retreat. There are no new reservoirs of resources and talent like Eastern Europe and China left to tap into. Postwar generations were at their productive peak in the 1990s and 2000s; today, they are retiring.

It is far too soon to declare another productivity boom.

Apart from the inflation risk, there is a further danger in taking interest rates down prematurely. The end of the Great Moderation came when excessive leverage and restrained financial supervision led to imbalances that ultimately toppled. Similar conditions may be developing in the present day; lower rates would add fuel to a flame that might need to be doused.

It has been interesting to see my streaming service learn my tastes and begin constructing playlists that suit them. While I’ve enjoyed many of the suggested songs, there have been others I don’t want to hear again. Musically and economically, I’d like to revisit the harmonies of the Great Moderation…and skip the dissonance that followed.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.