Weekly Economic Commentary | February 13, 2026

Japan-China: Bound, Not Just By Geography

Neighboring economic powers have more to gain from collaboration.

By Vaibhav Tandon

You can choose your friends, but you can’t choose your neighbors. Few idioms capture the tie between China and Japan more neatly. Geographical proximity, history and trade make them economically inseparable. That reality has long shaped a fragile equilibrium. Economic interdependence has acted as a brake on escalation, but if restraint thins, these links may become a transmission channel for retaliation.

Last weekend’s election in Japan has drawn renewed attention to China‑Japan relations. Prime Minister Sanae Takaichi has signaled a more forward‑leaning foreign policy, including constitutional revision and higher defense spending, that could reshape Japan’s security posture. This has prompted concern that a more assertive Japan may add strain to an already delicate relationship with China.

The risk played out not long ago when tensions over the East China Sea triggered widespread boycotts of Japanese goods in China. Autos and related products were stung, motivating a de-escalation. Tensions rose again late last year, as remarks by Japan’s prime minister led China to reimpose a ban on seafood imports, tighten controls on exports of dual‑use items, and discourage Chinese citizens from travelling to Japan. The impact was immediate: the number of Chinese visitors to Japan fell by nearly half last December compared with a year earlier.

Chinese visitors are Japan’s biggest spenders, accounting for roughly a fifth of the country’s more than $50 billion in tourism revenue in 2024. A further decline in arrivals would compound the damage. A repeat of the 2012 consumer boycotts alone could shave up to 0.4% off Japan’s 2026 gross domestic product.

Trade ties and domestic constraints will prevent a full-blown trade war.

China has used its advantage in rare earth minerals as leverage over both Japan and the United States, and could use this tactic again. This would strike at the heart of Japan’s automotive, electronics, and high‑tech manufacturing sectors, which are heavily reliant on Chinese rare earth magnets, motors and advanced components.

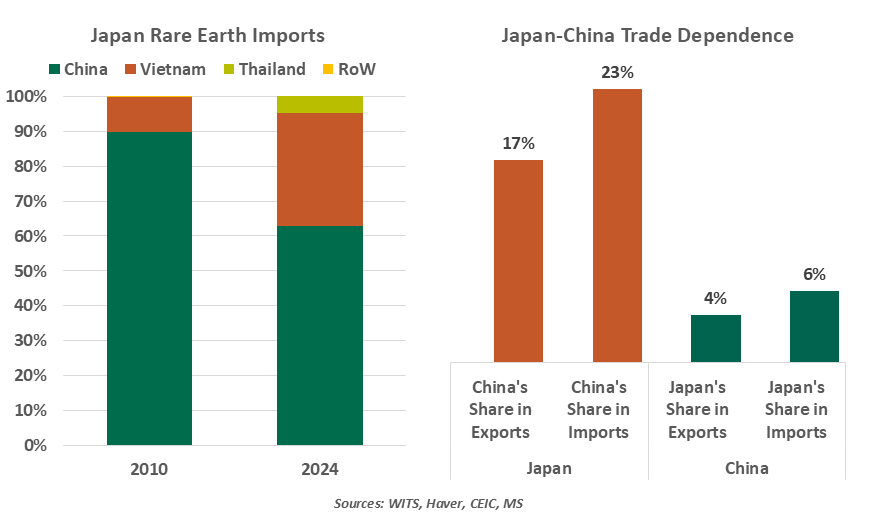

Although Japan has reduced its reliance on critical minerals from China (from around 90% in 2010 to 63%), the strategic importance of these materials has grown substantially, arguably leaving Japan more exposed than before. To respond, Japan’s rare earth supply has been diversified toward other countries, such as Vietnam and Thailand, while national reserves have expanded under more flexible stockpiling policies.

China retains other options, including restricting investment flows, imposing anti‑dumping duties or launching trade remedy investigations. Taken together, this gives Beijing considerable leverage.

The broader economic fallout of frictions with China would be challenging for Tokyo, given Japan’s dependence on China for trade. China is Japan’s top trading partner and its top source of imported goods. By contrast, China relies only modestly on Japan, both as a supplier and as an export destination. China is a critical node in Japan’s manufacturing supply chains and an unavoidable market for corporate earnings, accounting for close to 5% of revenues for listed Japanese firms.

Japan is not without leverage of its own. It could curb exports of equipment crucial to the production of advanced semiconductors. With deeply integrated supply chains, severe disruption would ricochet back onto China itself. China’s property sector remains fragile, and the macroeconomic backdrop is weak; as a result, the domestic economic cost of aggressive retaliation is materially higher for Beijing today than in past cycles.

With growth in both economies underpinned by trade, neither side has much appetite for a large‑scale economic confrontation. That reality should push both capitals toward calibrated responses rather than actions that sharply raise the costs of retaliation.

Neighbors may quarrel, test boundaries and even trade blows. But neither can afford disengagement. That reality does not eliminate the risk of retaliation. The mutual risks to growth, supply chains and domestic stability should motivate China and Japan to mend fences.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.