- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | May 8, 2026

Powell's Legacy

The outgoing chair did not back down from a wide array of challenges.

By Carl Tannenbaum

“Thank you very much, everyone. I won’t see you next time.”

With those simple words, Jerome Powell departed his final press conference as Federal Reserve Chair. Powell’s eight years at the helm have been anything but simple, however. A review of his tenure includes some hits, some misses, and some important lessons in leadership.

Powell’s appointment in 2018 was not universally applauded. This was no offense to him; Janet Yellen had served ably as Fed chair, and many thought she deserved a second term. Powell was the first Fed leader in more than 30 years to assume the role without a Ph.D. in economics, leading some to question his understanding of the business cycle. Over time, however, he demonstrated command of the key issues facing the institution. Degrees don’t always confer competence.

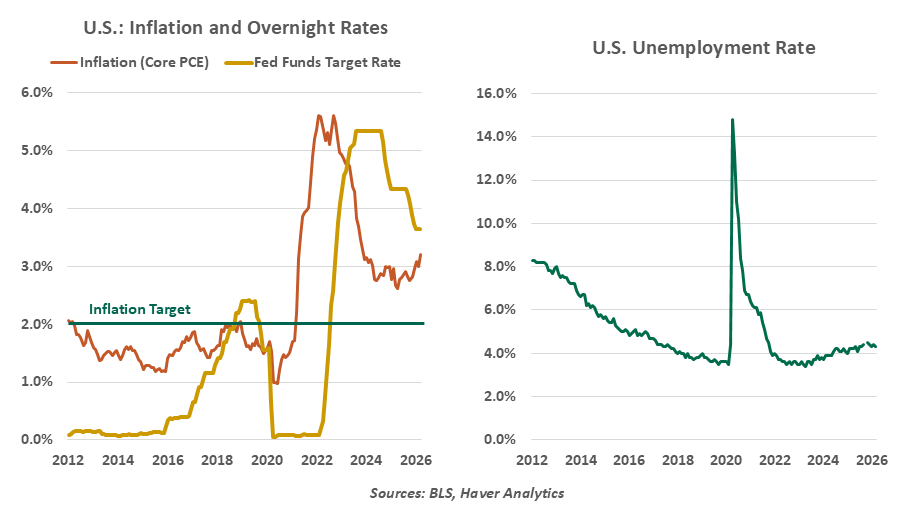

Powell inherited a minor inflation problem: annual increases in the price level had fallen below the Fed’s 2% target for a good portion of the 2010s. This led some members of the Federal Open Market Committee (FOMC) to conclude that monetary policy was unnecessarily restrictive. During a regional listening tour in 2019, Powell was moved by messages that job creation doesn’t often reach underprivileged communities until labor market conditions get sufficiently tight.

These impressions informed the update to the Fed’s operating framework, which advanced the concept of a “flexible average,” allowing inflation to run a little above the targeted level to compensate for periods where it was below that target. That meant somewhat lower interest rates in many environments.

The new outline was released in August 2020, during the depths of COVID-19. At the time, the pandemic presented significant humanitarian and economic challenges. Economic dashboards expanded to include infection and mortality rates. The needs to safeguard public health placed a series of businesses at risk of failure; employment fell by 20 million people in a single month; and U.S. equity markets lost a quarter of their value in the space of four days.

Powell’s biggest triumph was followed by his biggest disappointment.

The Fed’s reaction was swift and substantial. Interest rates were reduced to zero in less than two weeks, and quantitative easing was initiated at an unprecedented scale. Support programs for credit markets, drawing on designs developed during the 2008 financial crisis, were rolled out quickly. The result was the shortest recession in American history, covering just two months.

Some have suggested that the Fed went too far, but it didn’t seem that way at the time. Given the stakes and uncertainties facing the country in 2020, the monetary response had to be powerful. Powell and his colleagues moved decisively, and deserve praise for doing so.

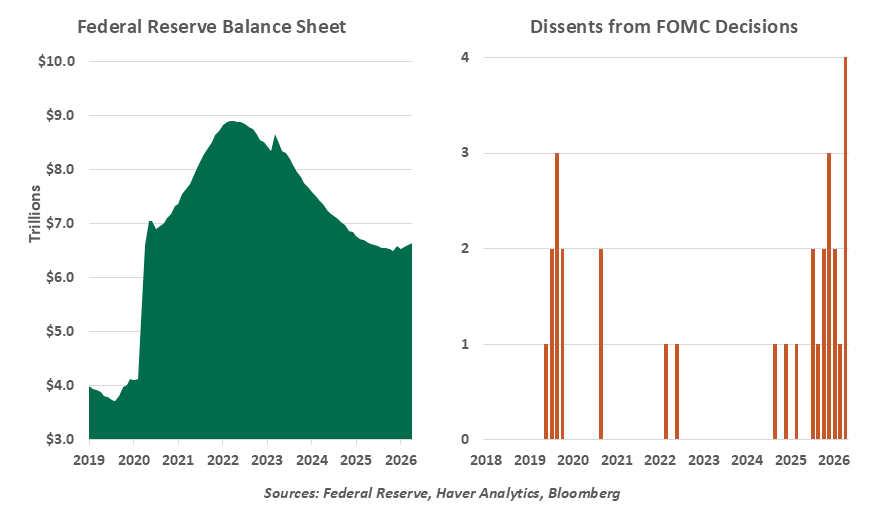

The most notable achievement of the Powell Fed was followed by its biggest miscalculation. The Fed’s insistence that post-pandemic inflation was transitory, along with its commitment to its new operating framework, led to policy that was too easy for too long. Conditions were tightened starting in 2022, but four years later, inflation has yet to return to its 2% target. The Fed’s balance sheet remains immense, something that incoming Chair Kevin Warsh has promised to have a look at.

Warsh, if confirmed, will need to manage differences of opinion within the FOMC. Dissents have been more numerous of late, the product of diverging ideologies and inconsistent data. Chair Powell has been very effective at forging consensus; perhaps that is something he can still help with as he steps away from leadership.

Powell’s decisions have been challenged persistently by the President who had nominated him. It started early, but mildly, with a late 2018 observation that the Fed Chair was a golfer who could not putt. Since then, the President has called Powell a “bonehead,” a “loser,” a “moron,” and other indignities. Earlier this week, Donald Trump posted an image of the Fed Chair being deposited into a dumpster.

Pressure from the White House on Fed leaders is hardly new. But the style and public nature of recent criticism is unprecedented. Powell was frequently questioned about the invective at his press conferences, but always took the high road. Last week, he asserted that the name-calling wasn’t troubling to him.

But efforts by the White House to influence the Fed did not stop at disparagement. The second Trump Administration has taken the extraordinary steps of attempting to remove a sitting Fed Governor and opening an investigation of Powell. The latter action prompted an equally unprecedented Sunday evening video message from the Chair, suggesting that the effort was primarily motivated by a wish to bring monetary policy under the control of the executive branch.

His staunch support of central bank independence may be Powell’s lasting legacy.

Those efforts ultimately convinced Powell to stay on as a Governor of the Fed at the end of his term as Chair. His term will expire in January 2028, with the option to resign sooner if he is satisfied that legal matters are settled. His support of central bank independence has earned him a series of standing ovations and plaudits from the press. In the long run, this may be his most important legacy.

Powell gave some memorable speeches. His first address to the Fed’s Jackson Hole conference in 2018 questioned the use of long-run interest and unemployment rates (known to economists as r-star and u-star) in setting a course for monetary policy. These ethereal quantities, he argued, are observable only in retrospect; this makes it hard to use them as the basis for policy in real time.

His 2022 Jackson Hole address centered on the concept of rational inattention, the tendency of people to overlook minor developments until they become more major. This explains why long-term inflation expectations in the United States remain well-anchored, despite the myriad price shocks that have occurred in the last five years. For this, the Fed should be thankful.

During his last visit with the press corps, Powell suggested that he would be keeping a low profile in the remainder of his tenure. That is just and proper. But I hope that he will continue to exercise his influence behind the scenes as the Fed works through the challenges that lie ahead.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.