Weekly Economic Commentary | May 1, 2026

Stagflation Suspense

Will the challenges of the 1970s return?

By Ryan Boyle

Automotive enthusiasts have coined the phrase malaise era to describe U.S. vehicles made from roughly 1973 to the early 1980s. New emissions and safety standards, plus high gasoline prices following the 1973 oil crisis, permanently reshaped the market. Automakers needed years to engineer more efficient vehicles. In the interim, they hurried out vehicles with detuned motors, lookalike bodies and poor build quality.

The cars of the 1970s were just one component of a regrettable interval. Nations subject to the oil embargo, including the U.S., U.K., Canada, Japan and the Netherlands, saw their unemployment rates roughly double from 1973 to 1975. Inflation rates spiked and struggled to calm down, with inflation in the U.K. exceeding 20%. The circumstances were summarized as stagflation: a combination of stagnant growth, uncontrollable inflation and elevated unemployment.

Worries of stagflation are on the rise again today. Oil prices are adding to the cost of living, while cooling job markets have put households on edge. The risks run globally: regions dependent on energy imports, especially Japan and Europe, are at high risk of an energy-driven inflation cycle. Memories of the 1970s malaise spring to mind, but we do not yet anticipate history to repeat.

A temporary price shock does not always lead to stagflation.

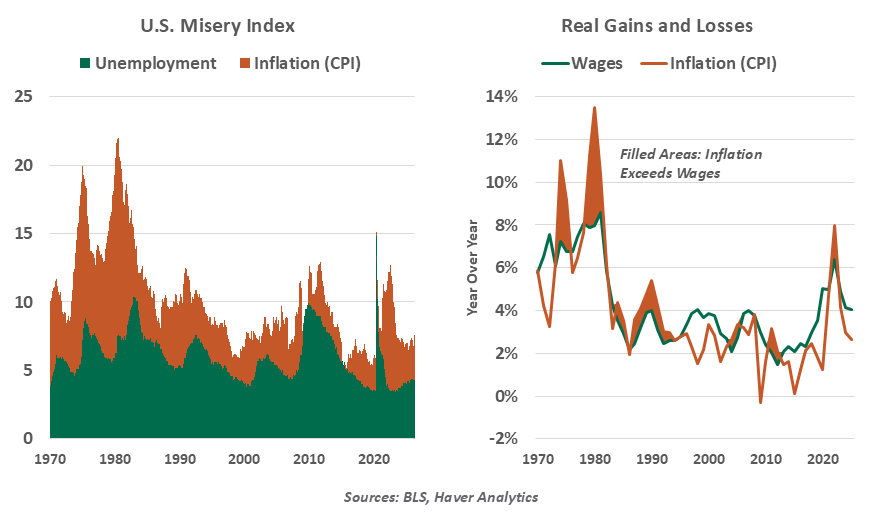

Stagflation can be difficult to define. By the numbers, it’s not a recession: economic growth stays positive during these episodes, and the unemployment rate may even improve mildly, though from a higher starting point. To a typical person, however, it feels like a recession. Inflation makes most households feel they are falling behind, while persistent unemployment makes them feel they can’t get ahead. A simple measure that took hold in the 1970s was the misery index, the sum of the unemployment rate and the rate of inflation. The higher the index, the worse the malaise.

The trigger for a stagflation cycle is typically an inflationary supply shock. While it may prove temporary, stagflation takes hold if the shock meets already-elevated inflation, a slowing economy and a weak policy response. A wage-price spiral can then sustain the cycle: workers demand higher pay to meet the cost of living, which allows prices to rise further.

The 1973 oil embargo was a clear shock to global energy markets. It sparked stagflation because the decade had gotten off to a sluggish start, with many nations seeing an industrial slowdown and higher unemployment. In the U.S., a politically-swayed Federal Reserve could not achieve inflation below 3%, though government spending on the Vietnam War and Great Society did not make stable prices any easier to achieve.

Stagflation cycles cannot be cured without some pain. A stimulative push for growth would risk adding to inflation. A recession can arrest inflation, allowing growth to reset sustainably. High interest rates and the recessions of the 1980s were the tough medicine needed to change course.

Today’s global energy shock invites comparisons to the 1970s, but conditions are not as amenable to starting a cycle of stagflation. Energy reserves are higher, and global production is more dispersed, while energy intensity is lower. Central banks responded forcefully to the inflation of 2021-22 and will do so again if needed. Fiscal policy is not stimulative in most nations. Unemployment has held low even as demand has slowed; today’s misery index does not compare to past episodes. And wages have not ascended in a manner that raises risks of a spiral.

The discomforts of the 1970s did not prove to be permanent. Interest rates, inflation and unemployment all reached a better trajectory. And in the auto sector, vehicle designs and performance stepped up, safety features proliferated, and emissions and efficiency vastly improved. Patience and prudent policy can help us all get through a rough ride today.

Related Articles

Meet Your Expert

Ryan Boyle

Chief U.S. Economist

Ryan James Boyle is the Chief U.S. Economist within the Global Risk Management division of Northern Trust. In this role, Ryan is responsible for briefing clients and partners on the economy and business conditions, supporting internal stress testing and capital allocation processes, and publishing economic commentaries.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.