Weekly Economic Commentary | March 27, 2026

Tax Refunds Supporting U.S. Households

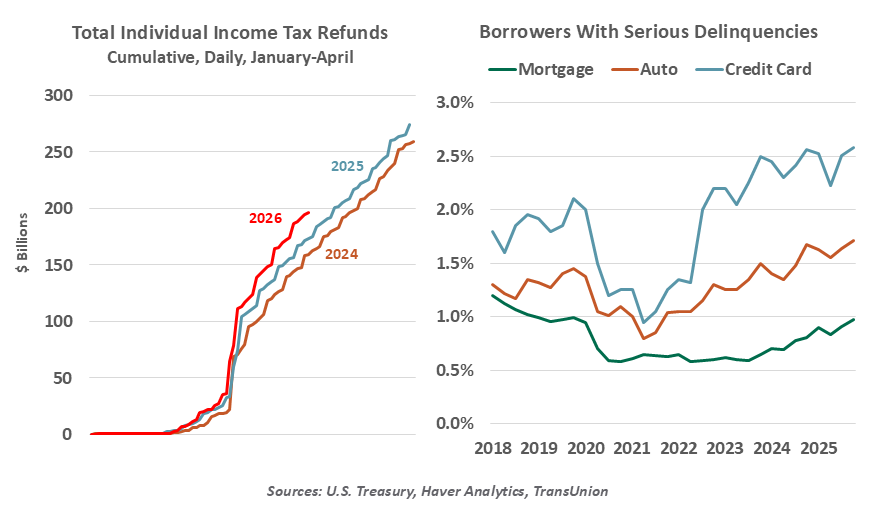

Tax refunds can help stretched American budgets.

By Ryan Boyle

Rationally, no one should feel happy about an income tax refund. The refund is a correction of a tax overpayment; the recipient effectively gave the government an interest-free loan over the course of the prior year. But behavioral economics shows otherwise: an annual tax refund feels like a windfall, a burst of income that provides more satisfaction than a slight increase in routine paychecks. Refunds have averaged over $3,000 per household in the past two years, providing a significant boost to American taxpayers. This year brought the potential of even larger windfalls to households, coming at a time that many can use the relief.

The “One Big Beautiful Bill” (OBBB) reconciliation package passed last summer locked in several tax benefits. Incentives included a quadrupled state and local tax deduction, an inflation-adjusted standard deduction, a bonus deduction for seniors, a larger child tax credit and exemptions for taxes on tips and overtime. However, tax withholdings were not changed in the balance of 2025, creating expectations of a refund “boom.”

To date, refunds have indeed exceeded recent years’ flows. Through mid-March, total individual tax refunds are running more than 12% above last year’s level. Individual circumstances will vary widely, but the Tax Foundation estimates that the OBBB generated an average of $611 in additional tax refunds in 2025, a 20% gain from prior levels.

Larger tax refunds will help American households to offset the energy shock.

The stimulus is not broad-based. The tax policy worked through higher refunds for those who paid higher taxes and interest. Its benefits will skew more toward higher earners, who are less likely to spend a windfall. While this compounds an uneven spending dynamic, it hedges the inflationary risk of putting money rapidly into circulation.

Recent developments have tempered our hopes for a near-term lift to discretionary spending from tax refunds. Oil prices have entered a new range that is about a third higher than the average of the year preceding the Iran incursion. U.S. consumers see the consequence directly in gasoline prices, which are up by about $1 per gallon. In aggregate, motor fuel represents about 2% of household consumption, a proportion which varies widely depending on vehicle and lifestyle choices. Consumers will feel ripple effects of higher goods prices to offset transportation costs, and in food prices as fertilizer becomes more costly.

Today’s energy disruption is comparable to the shock of Russian sanctions in 2022, after the Ukraine invasion. Consumers groused about high prices but did not stop spending. A difference today is a softer starting point. The U.S. labor market has cooled, with limited hiring prospects. Pandemic stimulus payments are a distant memory. Borrowing costs are higher. Student loans are due. Wealth effects are supporting consumption, but unevenly.

A growing share of U.S. households are showing some strain. Credit bureau TransUnion reports the share of consumers with subprime (highest risk) credit scores increased by 2.4%—over four million people—over the past four years. The share of consumers with serious mortgage, auto or credit card delinquencies are all stepping up to cycle highs.

Measures of consumer sentiment remain depressed, though we learned in 2022 that low sentiment does not always equate to lower spending. Excluding the auto sector, monthly retail sales have shown slow growth in recent months, with no evidence of an imminent slowdown. Limited layoffs will help consumers to maintain their spending.

Annual tax filings follow a pattern: Those who expect a refund complete their taxes quickly, while those who owe will submit their filings and payments closer to the April 15 deadline. The irrational excitement of refunds has peaked; the rational worries about the costs of living carry on.

Related Articles

Meet Your Expert

Ryan Boyle

Chief U.S. Economist

Ryan James Boyle is the Chief U.S. Economist within the Global Risk Management division of Northern Trust. In this role, Ryan is responsible for briefing clients and partners on the economy and business conditions, supporting internal stress testing and capital allocation processes, and publishing economic commentaries.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.