Weekly Economic Commentary | April 17, 2026

The Outlook From, and For, the IMF

The International Monetary Fund is more vital than ever.

By Vaibhav Tandon

Each spring, the International Monetary Fund (IMF) releases its World Economic Outlook (WEO), a review of global growth, and the key challenges confronting the world economy. This year’s edition followed the Fund’s usual structure, but the circumstances underneath it had shifted. Conflict was no longer treated as an external tail risk. It is now a core input embedded directly into the projections.

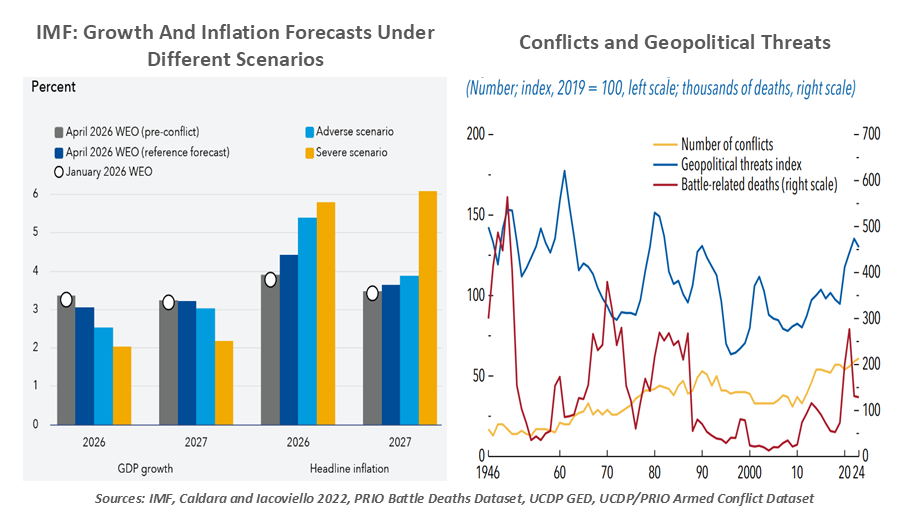

The IMF framed its outlook around a range of scenarios tied to the evolution of the Middle East war. The storyboards ranged from a relatively swift normalization to a worst case in which energy prices remain structurally higher for longer.

Under the baseline, where hostilities ease relatively quickly, the Fund shaved 0.2 percentage points off global growth for 2026. It lifted its inflation projection by 0.6 percentage points compared with its prewar baseline.

The downside scenarios are far more sobering. If the conflict proves more protracted, the IMF estimates global growth would be reduced by 0.8 percentage points under an adverse scenario and by as much as 1.3 percentage points under a severe adverse case in 2026. The drags are likely to extend into 2027. These outcomes are driven by sustained energy price pressures and tighter financial conditions, as central banks respond aggressively to renewed inflation risks.

The severe adverse scenario flirts with outright global recession, defined as growth below 2%. That threshold has been crossed only four times since 1980, most recently during the global financial crisis and the pandemic. In that case, the IMF assumes oil prices rise from an average of roughly $110 per barrel in 2026 to around $125 in 2027. Inflation would remain meaningfully higher, nearly two percentage points above baseline in 2026 and 260 basis points (2.6 percentage points) higher in 2027. As in most past shocks, emerging markets would bear the brunt of the adjustment, facing greater macro pressures than their developed peers.

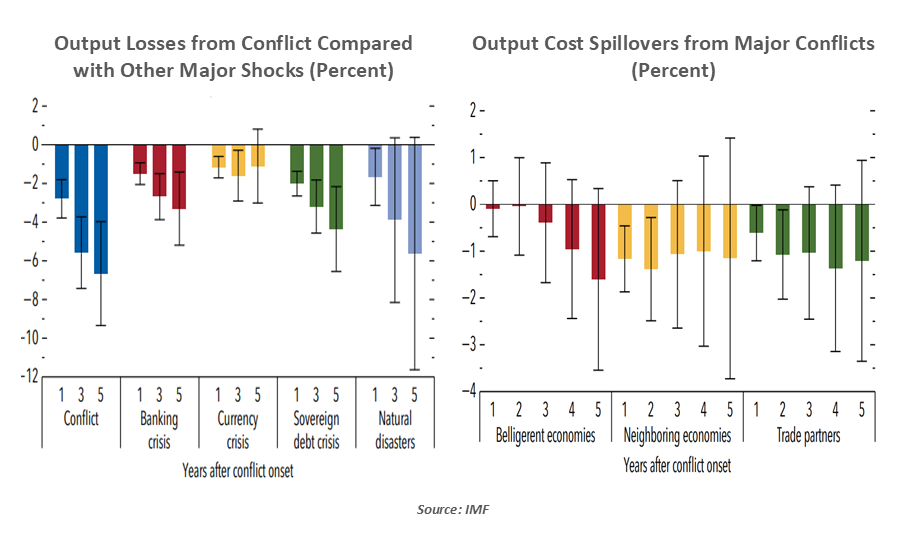

These projections are backed by a deeper analytical point made in the Chapter 3 of the WEO. The number of conflicts worldwide has risen sharply since the 2020s, reaching historically elevated levels. Conflict, the IMF argues, generates output losses that are larger and more persistent than those associated with financial crises or severe natural disasters. Output typically contracts sharply at the onset of hostilities, with cumulative losses approaching 7% within five years.

Conflict slows growth and pushes inflation higher.

These projections are backed by a deeper analytical point made in the Chapter 3 of the WEO. The number of conflicts worldwide has risen sharply since the 2020s, reaching historically elevated levels. Conflict, the IMF argues, generates output losses that are larger and more persistent than those associated with financial crises or severe natural disasters. Output typically contracts sharply at the onset of hostilities, with cumulative losses approaching 7% within five years.

The macroeconomic transmission channels are well worn. Inflation accelerates, exchange rates come under pressure, reserves are depleted and fiscal balances deteriorate. These stresses are compounded by political constraints that make economic adjustment harder to implement.

Even where fighting does not take place, neighboring economies and key trading partners are rarely insulated. Trade disruptions, commodity price volatility, heightened uncertainty and population displacement ensure spillovers are broad and material.

Recoveries from conflict tend to be slow and uneven. The scars often persist for a decade or longer. Even when peace holds, rebounds rarely offset wartime losses. In a nutshell, conflict leaves economies not just smaller, but structurally weaker.

This analytical backdrop helps explain why the IMF’s role now matters more, not less. The Fund’s core mandate is to stabilize fragile macro situations and prevent local crises from cascading into global ones. Heavier debt burdens have left many countries with limited fiscal space and fragile market access. Stabilization is therefore no longer episodic or inexpensive, but increasingly larger in scale and longer in duration.

It is in this context that IMF Managing Director Kristalina Georgieva warned that near‑term demand for IMF financing could rise by $20-50 billion as spillovers from the Middle East war intensify. That would come on top of an already heavy caseload. Before the conflict escalated, the IMF had roughly $140 billion in active programs; including credit outstanding and approved but undisbursed lending, total commitments now stand near $250 billion. Between May 2024 and March 2025 alone, new IMF lending exceeded $35 billion.

The IMF’s lending capacity rests on quota resources provided by over 190 member nations. Quotas form the Fund’s permanent capital base are denominated in Special Drawing Rights (SDRs), an international reserve asset linked to a basket of major currencies.

The IMF is more vital than ever.

Under the 16th General Review of quotas, approved in December 2023, total quotas are set to rise by 50%, lifting permanent resources to roughly SDR 716 billion (around $960 billion). However, the increase has yet to enter into force because the required 85% voting‑power ratification threshold has not been met. Past experience suggests this delay may be protracted: the previous major quota reform took nearly five years to clear the U.S. Congress before taking effect in 2016.

The obstacle is not technical capacity or financial need, but politics. Multilateral institutions face heightened scrutiny, particularly in Washington. Some advanced economies remain wary of future quota realignments that could shift voting power toward large emerging markets, even though the current review does not alter vote shares.

At the same time, regional financial safety nets have expanded. The European Stability Mechanism, the Chiang Mai Initiative Multilateralization and China’s bilateral swap lines offer alternatives that can provide quicker access to financing. Yet these arrangements vary widely in scale and usability and cannot substitute for a globally anchored institution with near universal membership. For lower income countries, a fragmented financial safety net risks leaving protection uneven precisely when demand for stabilization is rising.

Whether the IMF is adequately resourced, and politically supported to meet that demand, is no longer an abstract institutional concern. The backstop provided by the organization is of benefit to investors around the world, not just to the recipients of support. With global hotspots multiplying, we need as many cool heads as we can get.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.