Weekly Economic Commentary | July 17, 2026

The Relationship Between AI and Inflation

Technology investment carries rising costs.

I really struggle to understand my utility bills. They often run to several pages, with sections describing just how difficult it is to get water from the source to your faucet, or internet service from a satellite to your home router. At the end, there is a long list of charges from a range of payors that adds up to an astronomical sum.

I have been tempted to assume that greed was the main driver behind rising utility costs. But I am coming to understand that the artificial intelligence (AI) boom is also at play. AI is adding to inflation in the current day, while the question of whether it will reduce inflation in the longer term remains open.

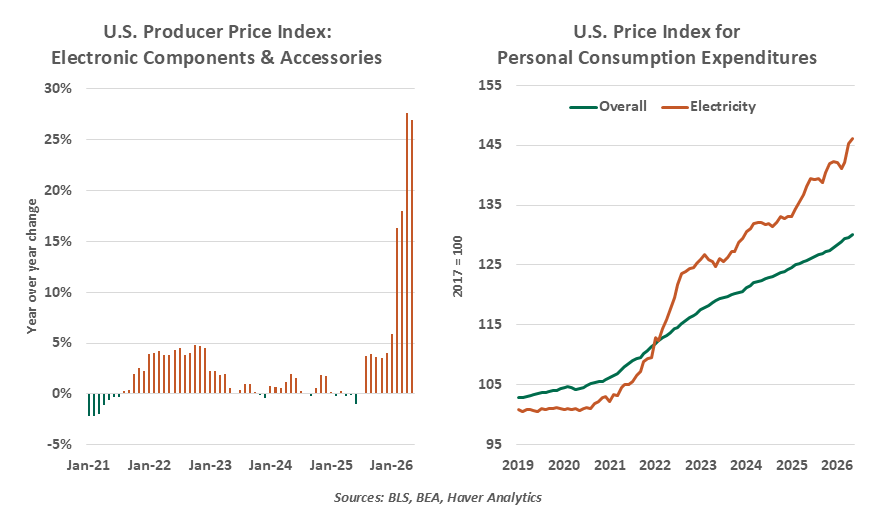

The AI boom affects a range of consumer prices. Utility costs lead the list: while some data centers have integrated power sources, most do not. The toll taken on transmission networks requires additional maintenance and investment. Bloomberg has reported that electricity rates in areas with heavy data center concentrations have more than doubled over the past five years. Data centers also require extensive cooling systems, raising water rates for the surrounding locale.

As part of a backlash against data centers, an increasing number of communities around the world are pressing AI developers to insulate residents from the demands placed on utilities. Providers are being asked to finance expansions of capacity and infrastructure, and to underwrite rate caps for residents. But these costs will undoubtedly be recouped through the pricing of AI-related services, which consumers and businesses will pay.

A wide range of firms are rushing to put AI into broader usage. To do so, they have to secure capacity for their models to run. These costs of computing are rising very quickly, as major AI providers switch from flat rates to usage-based billing. This will raise the prices of everything from Uber rides to cellular telephone service. In some instances, AI algorithms are costing more than the workers they are designed to replace.

Finally, the equipment that goes into data centers is in high demand. The chips and servers that create memory for processing are in short supply, and their prices have jumped. Electronic equipment has experienced deflation over many past intervals, as the power of components has increased while prices did not. That era now seems to be over.

Gauging the pass-through to consumer prices is complicated. The categories most obviously affected, like personal computers and utilities, have low weights in the consumer price basket. But 81% of the contributors to the National Association for Business Economics forecast survey expect AI to be inflationary over the next twelve months. Goldman Sachs estimates this impact at 0.5% by year end for the U.S., with a smaller effect for other developed markets. This increment will make it even more challenging for central banks to hit their inflation targets.

AI is adding to inflation.

AI proponents note that upfront investments will pave the way for important productivity gains in the years ahead, which will limit inflation. The prospective size and timing of these benefits is the subject of active debate.

As we discussed in an essay entitled “Automation and Anxiety,” this is far from the first time that machines have made inroads into the global economy. Past periods of technological advance created the same kind of mixed feelings that are present today, but they eventually paved the way to higher productivity.

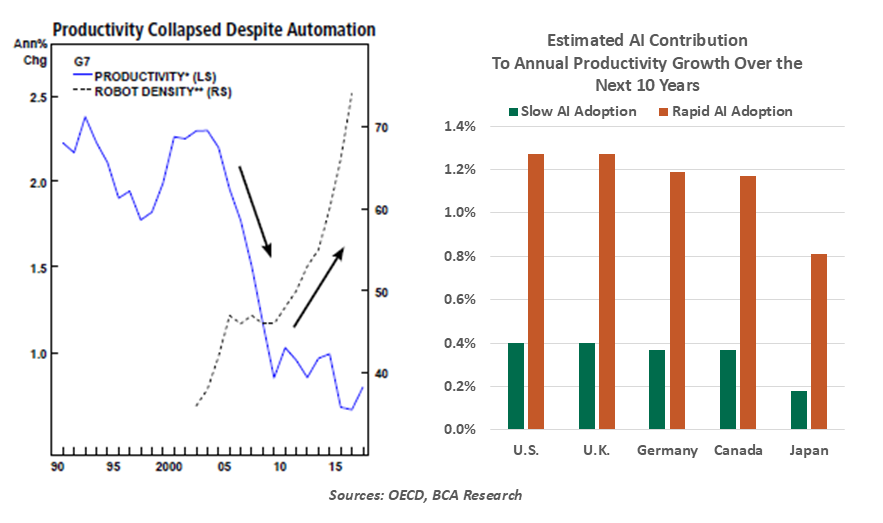

But not all transformations produce the desired effects. Starting in 2009, the number of industrial robots in service around the world grew geometrically. But instead of improving, productivity collapsed. Installing the machines was straightforward, but adapting processes and personnel to maximize their application proved difficult. AI will face similar challenges.

The influence of new technology on productivity depends on a series of factors. Adoption is the most critical one, as it usually takes considerable time for usage to reach a critical mass that truly affects business processes. Industrial composition is another: AI is expected to produce bigger productivity gains in countries with larger service sectors. At this early stage of the AI age, it is difficult to size the outcomes. Most projections of the incremental productivity to be derived from AI are expressed as very wide ranges.

The translation of productivity to inflation is also not straightforward. Goods and services that are created more efficiently can be expected to experience smaller price increases. But workers often capture their increased productivity in the form of higher wages. Firms may choose to bank their productivity savings as higher profit margins. Those improved earnings could bolster stock prices, creating wealth effects: the resulting increase in demand can keep prices high.

New technology doesn’t always lower inflation.

These issues will be a focal point for one of the task forces established by Fed Chair Kevin Warsh. The group will “assess the economic impact of new general-purpose technologies, including artificial intelligence.” Warsh is on record anticipating that AI will usher in an inflation-reducing productivity boom, and the leaders of the task force (all of whom have tech backgrounds) are likely to agree with him. But the risk that productivity gains take longer to realize, or will be smaller than anticipated, must be respected.

I am hoping that AI might one day help me better manage my utility bills. I suspect there are many opportunities to optimize our use of power and water. But if the algorithm suggests that we use less air conditioning in the summertime, my wife will save electricity by unplugging ChatGPT.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.