Weekly Economic Commentary | March 6, 2026

War In The Middle East: Economic Implications

Energy market disruptions will be felt worldwide.

By Carl Tannenbaum and Vaibhav Tandon

The opening months of 2026 have been hectic. A partial inventory of major developments during the year to date would include the removal of Venezuela’s leader; a government investigation into the Chairman of the Federal Reserve; tension with Europe over Greenland; and a broad swath of U.S. tariffs stricken down by the Supreme Court. It’s been a lot to digest.

And then last weekend, the outlook was complicated again by events in the Middle East. Israel and the United States attacked Iran, which has subsequently retaliated against a series of regional targets. It appears that hostilities will continue for at least the next several weeks.

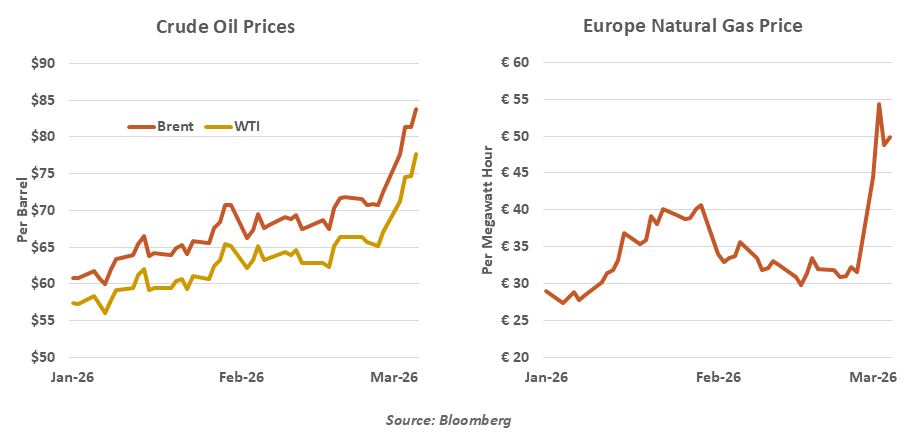

Energy prices are the primary transmission mechanism for economic consequences. The closure of shipping lanes, a pause in production of liquified natural gas (LNG), and attempts on energy infrastructure have reduced daily supply and raised risk premiums in energy markets. The price of oil has risen by about 18%, and the cost that European and Asian markets pay for natural gas has skyrocketed.

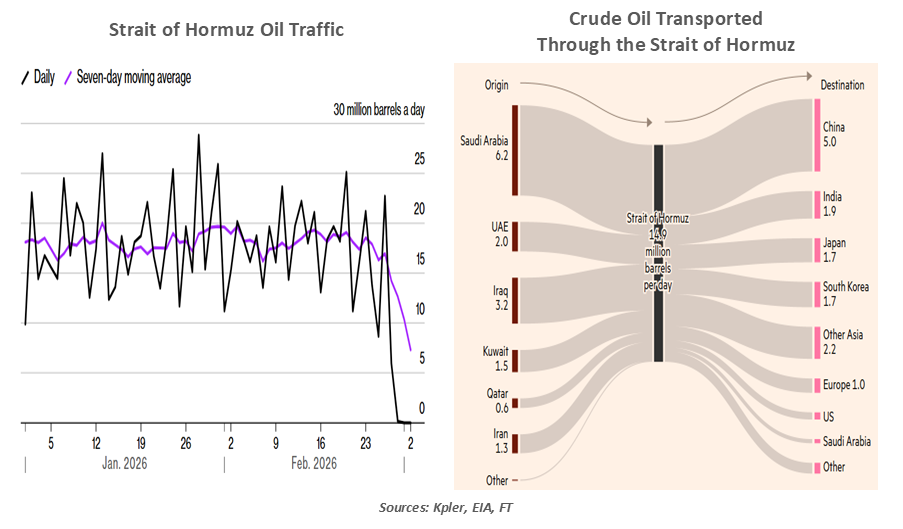

About a fifth of the world’s oil consumption and a quarter of LNG pass through the Strait of Hormuz. The waterway is one of the narrowest passages in the world, barely two shipping lanes wide. Its size and location make it the world’s most important energy transit chokepoint.

Maritime traffic through this vital waterway has ground to a halt since last weekend, stalling about 20 million barrels per day of oil shipments. This will affect global producers and consumers alike, with the impacts most acute in Asia. Major regional energy importers like China, India, Japan, and South Korea are among the most reliant on this conduit, receiving more than 60% of the supplies that pass through Hormuz.

Qatar, the world’s second largest LNG producer, has halted operations following Iranian attacks at its plant. Qatar and the UAE account for more than half of India’s LNG imports and around a third of China’s. These energy‑dependent, energy‑intensive economies aren’t involved in the fighting, but they are major stakeholders in the outcome.

Hoping that a transportation problem doesn’t turn into a production problem.

Global output is much less dependent on energy than it once was. But higher prices act as a tax on consumers, and reduced availability can hinder production. At present, the war is creating transportation problems; if there is damage to production capacity, the fallout will be longer-lasting and more severe. In this event, fiscal and monetary policy around the world may have to be recalibrated.

It is not in any party’s interest to target energy infrastructure. Aggression from Iran would almost certainly provoke retaliation, damaging export revenues for all. Iran is the world’s sixth‑largest oil producer and the third‑largest within the Organization of the Petroleum Exporting Countries. While spare capacity in Saudi Arabia and the UAE could replace some lost Iranian output, alternative routes can handle only about a third of normal Hormuz flows.

The global economy has been very resilient, but the war will provide a stern test.

For the United States, strikes on Iranian oil facilities would remove meaningful volumes from an already fragile global balance. This would produce a spike in inflation that would be at odds with U.S. preferences for lower fuel costs and looser financial conditions. The war effort is an expensive one, costing an estimated $5 billion per week.

Europe is not directly involved in the conflict, yet the situation risks creating the most severe energy shock since the Ukraine war. Europe sources only about 10% of its LNG from Qatar, though the share rises to one-third for Italy. An immediate shortage this winter appears unlikely, given continued pipeline flows from Norway.

However, disruptions in Hormuz would intensify competition for alternative supplies, echoing dynamics seen during the 2021-23 energy crisis. Unlike East Asia, where a larger share of supply is locked into long‑term contracts, Europe relies more heavily on spot markets, leaving it exposed to sharp price swings.

China relies on Iran for about 13% of its petroleum needs. With another 5% sourced from Venezuela, China finds a significant fraction of its supplies at risk. Electric vehicles make up over half of new car sales in China, but oil is critical to a range of other industries. Reduced supplies from Iran could make it difficult for China to sustain targeted rates of economic growth.

Japan is also exposed to near-term stagflation risks if energy prices surge while wage growth lags. This would be an especially uncomfortable mix for an economy that has only recently re-engaged with inflation. Economic activity and financial markets have shown admirable resilience amid the maelstrom of policy uncertainty over the past year. The most recent economic outlook from the International Monetary Fund characterized the global economy as being “Steady Amid Divergent Forces.” But the situation in the Middle East is very serious, and it will present challenges for individuals, firms, and portfolios.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.