- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Trend Lightly

Systematic vs. Discretionary Styles

Traditional public equity strategies can broadly be sorted into three categories: active discretionary (fundamental stock picking), quantitative (systematic or data driven), and passive. Active equity managers generally underperform their passive counterparts net of fees. But what about discretionary versus quantitative strategies? A recent paper by AQR titled “A New Paradigm in Active Equity” dives into this question.

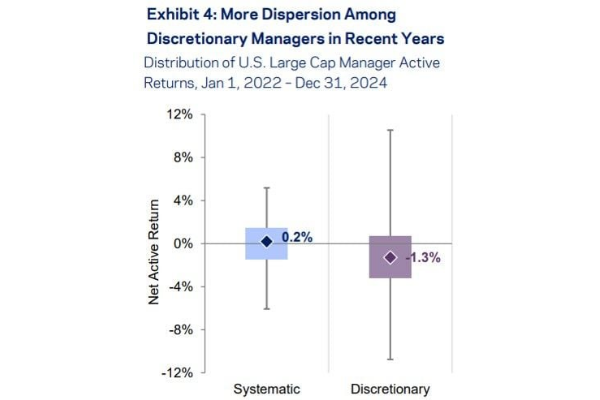

Over the past three calendar years, AQR found that systematic strategies have generally performed better, both in absolute performance delivering 20 basis points in net active return after fees and in terms of volatility with lower dispersion in returns as well. The latter point seems logical, as quantitative funds generally hold a more diverse and less concentrated basket of securities compared to discretionary strategies.

Source: AQR, eVestment Whiskers show maximum and minimum values, box shows the inter-quartile range, and marker is the median value. Manager returns are for U.S. Large Cap Equity managers in the eVestment database. See Disclosures for a description of the universe. Discretionary and Systematic refer to managers who have reported their primary investment approach as fundamental and quantitative in eVestment respectively. We remove managers who do not have returns over the full period shown. Manager active returns are calculated by eVestment relative to manager preferred benchmarks and are reported either gross or net of fees. For managers who report returns gross of fees, we convert the returns to net using the median fee of the universe. Time period is January 1, 2022 to December 31, 2024. Past performance does not predict future returns.

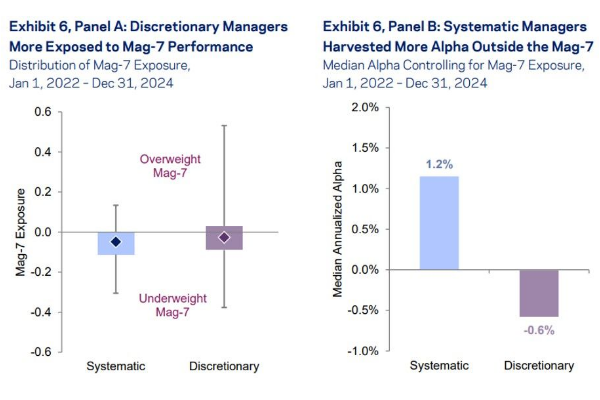

The authors in the AQR paper theorize that discretionary managers have struggled in recent years as the US stock market has become more concentrated, especially given the dominance of the Mag 7 stocks. In fact, what their analysis discovered is that systematic strategies were actuallymore successful in delivering alpha from outside the Mag 7. These findings seem counterintuitive. The AQR authors believe these results are inherent in more diversified portfolios, writing that "a small advantage spread across many unique bets provides a quant manager with conviction, rather than relying on a concentrated 'all eggs in one basket' strategy."

Source: AQR, eVestment Manager returns are for U.S. Large Cap Equity managers in the eVestment database. See Disclosure for a description of the universe. Discretionary and Systematic refer to manager who have reported their primary investment approach as fundamental and quantitative in eVestment respectively. We remove managers who do not have returns over the full period shown. “Mag-7 exposure” is calculated based on a returns based regression of manager active returns on returns on the S&P 500 and a market neutral “Mag-7 Factor”. “Alpha controlling for Mag-7 exposure” is annualized alpha from the same regression. Time period is January 1, 2022 to December 31, 2024. Past performance does not predict future returns.

In other words, the key differences in the structure of quant versus discretionary strategies is increased diversification. A higher degree of diversification allows the quant fund to have more conviction because they are making so many small bets. Moreover, the ability to build and harness models with unique data inputs or signals can be leveraged to further improve conviction, a trend likely to become more potent with AI

It turns out discretionary strategies can also improve their conviction while staying more concentrated, which is critical as I still believe that active stock picking is a key ingredient in efficient markets and deserves consideration as part of an overall equity strategy. For these reasons, Northern Trust continues to invest in solutions to support fundamental investing. Our partnership with Equity Data Science (EDS) and Essentia Analytics is a manifestation of our commitment to active management.

EDS supports the integration of systematic elements into traditional stock picking, leveraging quantitative and data driven solutions to deliver a “best of both worlds” approach to fundamental equity strategies. One of the key points made by AQR is around conviction, and EDS provides a data-driven platform to codify and evaluate conviction.

Essentia Analytics helps portfolio managers understand behavioral biases to instill more discipline into the investment process. With better situational awareness of biases and data-driven feedback, Essentia enables an improved ex-ante decision process that more resembles that of quantitative funds.

These tools, I believe, improve conviction without increasing diversification and will keep discretionary equity strategies relevant, enabling evolution in a world with increasing reliance on data and modeling.

Meet Your Expert

Grant Johnsey

Grant is responsible for delivering capital market solutions to institutional clients across agency brokerage, transition management, security finance, and foreign exchange.

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure

Business Continuity Notice- Northern Trust Securities, Inc.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.