- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Weekly perspectives from Gary Paulin, Head of Global Strategic Solutions, on global market developments and their potential broader implications

November 18, 2023

LET'S TALK, COFFEE WITH JEREMY AND TRADE OF THE DECADE

Let’s talk

Despite being a long way from converted to ‘friends’ (Abraham Lincoln’s preferred tactic for defeating an enemy) and while many will question both Xi’s motives (domestic economy?) and his reliability (see 2005 promises), the fact the US and China are talking again is positive. Both countries benefit from stronger alignment, not least to help tensions from escalating in the Middle East. And keep an eye on potential ‘talks’ in Ukraine as well. As we’ve discussed, China has a likely role to play in brokering any ceasefire, an outcome that’s beginning to look more likely. Earlier this week the CIA boss headed to Kiev for urgent, secret meetings with Zelensky as Ukraine’s offensive looks to be faltering. And, as Pippa Malmgren writes on X, ‘on the back of the Xi-Biden meeting, look for the CIA to negotiate an armistice in Ukraine’. Should such occur, oil and wheat prices would probably fall (perhaps they are already anticipating such?). If we get a ceasefire – and yes, it’s a big "if" – it would support the deflation-duration narrative, and give those folks who bought the 10yr recently a wonderful opportunity to sell into strength.

But for the vast majority of plans who were adding in January on calls for recession, you might not be so fortunate. I still believe 10yr bonds will destroy value if held to maturity. There is far better value in Credit. And no, I’m not tempted by ARK or US growth stocks, although will stay with components of the Mag7 who will concentrate the spoils of the AI revolution. But price always matters, and there are potentially much better prices elsewhere. You just need a passport to find them for they are in the UK, Japan and Brazil.

Defused tensions

It may also pay to keep an eye on events in Taiwan. As mentioned in last week’s missive, nearly 50% of the world’s population goes to the polls next year, starting with Taiwan in January and ending with the US in Nov. With regard to Taiwan, note a joint ticket is forming that may defeat the pro-independence DPP. Recent polls suggest that combined these parties would attract a majority of voters and a decision to run on a joint ticket will be made today, 18th November. Should such emerge – and should they be successful – China could obtain Taiwan by cession, not conquest. And the US would no longer have to protect ‘independence.’ Such would, I suspect, remove Taiwan as a top geopolitical risk (until a new independent party is reinstated), and could reset the narrative on Sino-US relations. Is that too optimistic? Perhaps. Maybe I need to remind myself of Edward A Murphy’s (i.e. Murphy’s Law) quip that: “Anything that can go wrong will go wrong.” And then, when it has, say to myself: “Smile. Tomorrow could be worse.”

A growing French affair closer to home…

Even the French and English are talking! Post Prince Charles’ charm offensive, and despite Ridley’ Scott’s imminent reminder of defeat (Napoleon Movie), the French have decided to drop the restriction on Brits with second homes from staying more than 90 days per year. Although I think this might be less about love and more about money, for the Brits are the biggest tourist spenders in France. Still, good to see them talking, for as we argued recently, closer EU ties could help reverse some of the valuation discount that emerged post Brexit (c20-30%). Just another potential catalyst for UK stocks. And here’s a few more…

The UK – “Trade of the Decade? (and beyond)”

Ahead of the Autumn Statement on November 22nd, there is a big push to ensure UK Chancellor of the Exchequer Jeremy Hunt encourages greater participation in UK equity and growth markets. We’ve seen a number of proposals put forward, which this letter from The Capital Market Industry Task Force (CMIT) summarizes, and was sent to Hunt on Thursday. It covers the parlous state of UK equity ownership, the inclusion of a competitiveness objective in the FRC’s mandate, reforms of the pension market and changes to the ISA rules (see BRISA). My expectation is: all these points will be acted on, and in time, we will look back at these events as change catalysts for the UK equity market. This as UK equities remain detested, with fund managers about as "underweight" as they've ever been, relative to the rest of the world. It feels all US circa ‘81/82, just after the ‘Death of Equities’, just as rates peaked and just before 401Ks got going and lit the touchpaper on domestic equity ownership and a 40-year bull market. In terms of the suggestions put forward, the competitiveness objective is significant when combined with already enacted moves on removing wage caps, easier listing rules and research sponsorship (MIFID reform). The only thing we don’t have to attract would be listings – yet – is higher valuations. But that will come with time. And the following should help…

Tax breaks

Tax savings are, as we know, a powerful elixir. Should we get pension reforms in the shape of capital gains tax exemptions limited to +£20bn or so (per the recommendations of the William Hague/ Tony Blair Report), this could drive DC consolidation, while removing liquidity barriers to private and even smaller cap equities. Combine this with BRISA (the British ISA), just as rates peak and we could see a reversal of flows out of cash into equities, a la Japan and their NISA program (which is also expanded next year) and out of expensive, into cheaper UK assets. As an aside, Material World by Ed Conway is released in the US this week, reminding American investors that the scarcity of their technology and transition bets (and therefore the value) might not solely lie in the stocks they all know and love, but in those in the Material world (and claims thereon) which they all ignore. Great news, I believe, for the UK stock markets (and Japan and Brazil). Ok, and Canada and Australia too.

Coffee with Jeremy Hunt

I ran into Jeremy Hunt on Thursday morning (literally!) at a London café. A mix-up with the coffees ended up him taking mine, so I chased after him to swap. He thanked me and walked off before I had a chance to quiz him on the Autumn Statement. I wonder if he would agree with me that it might be time to buy UK equities, before the Canadians, private equity (see another deal Wednesday), trade buyers (two more on Thursday, one at 160% premium) or the companies themselves (buybacks currently at record highs) beat us to it?

Challenging the 3 D's

No, not “Dackle, Dackle, Dackle” (rugby joke: ask me later) but “Demographics, Decarbonisation and Deglobalisation.” Gaze into your crystal ball and can you see a world where Sino-American relations are such that FDI returns, as do supply-chains, ‘de-coupling’ is replaced with ‘re-coupling’ and China helps to export disinflationary pressures to the western world – much like it has for the past few decades? It’s not a zero-probability, although I would question if the benefits, lest from a cost perspective, are as good as they once were when compared to other areas (and even subsidies back home). But let’s assume it happens. Could this alter the assumed narrative around supply chains, around inflation and therefore interest rates? I’m not sure. For it’s not the direction of price as much as the uncertainty around it that causes the biggest issue. Yes, we might get more disinflation. Deflation even. But equally, the chances of inflation, stagflation or hyper-inflation have not been eliminated, meaning inflation and rate volatility will be a defining feature of our future. Such will cause the most critical component of the most critical supply chain – the cost of money and the money supply – to remain elevated, as it must to compensate for the risk (and the unprecedented $8.2tn of US government debt maturing in the next 12 months, as per Bloomberg).

A higher structural risk premia is now required for holding bonds at the end of credit cycle. Historically, real 10yr yields averaged 2%. Should core inflation settle around 3% (the 50-year average) a 5% yield seems fair. I suggested buying bonds for a trade a few weeks back. I didn’t expect them to rally quite as quick as they did. They are bonds, not penny stocks after-all. There are better alternatives that are no one else’s liabilities. Like gold.

Borrow from pessimists

I would rather not own liabilities at this stage of the cycle. Nor would I want to be a borrower (if you have to, “borrow from a pessimist. He won’t expect it back” – Oscar Wilde). Gold could be safer to hold, and yet it seems very few of us hold it. According to Bank of America and Crescat Capital, 71% of investment advisors hold 0-1% of gold in their portfolios today. And keep in mind that in 1980, gold constituted 75% of global central bank assets, whereas now it accounts for less than 20%. Will bitcoin serve a similar purpose for future generations? Note: Coinshares report over $1bn in institutional inflows in less than two months, with AUM up 99% year-to-date.

Global fiscal reactions

Turning now to the other D’s: decarbonisation and demographics – and the interplay between them, it’s worth remembering we are about to embark on the world’s largest ever construction project (the green transition) at a time of near-full employment and when demographics are such that we retire far more construction workers (and spot welders!) than we can ever hope to replace or reproduce (AI). Running 6% fiscal deficits at a time of full employment is inconsistent with price stability. And you can expect a muscular reaction function from other governments to counter the hoarding effects of things like the Inflation Reduction Act. Japan recently approved a $113bn stimulus to ease impact of inflation. We know the Labour government has penned a £28bn green infrastructure plan, which in relative terms is even bigger than the IRA. Europe has its Green Deal and now Australia is being pressured to have a stronger response to the IRA, likely before the end of this year. Looking to 2024, I expect manufacturing activity recovers as a number of head-winds – de-stocking, Germany’s energy issues, China slowing – fade if not reverse.

Competition for scarce resources tends to be good news for the prices of those resources, and the countries and companies that control them. This is especially so after a period of capital constraint, like now. This at a time when most allocators ignore them – which will change over time, I believe. It has to, save us missing our net-zero targets.

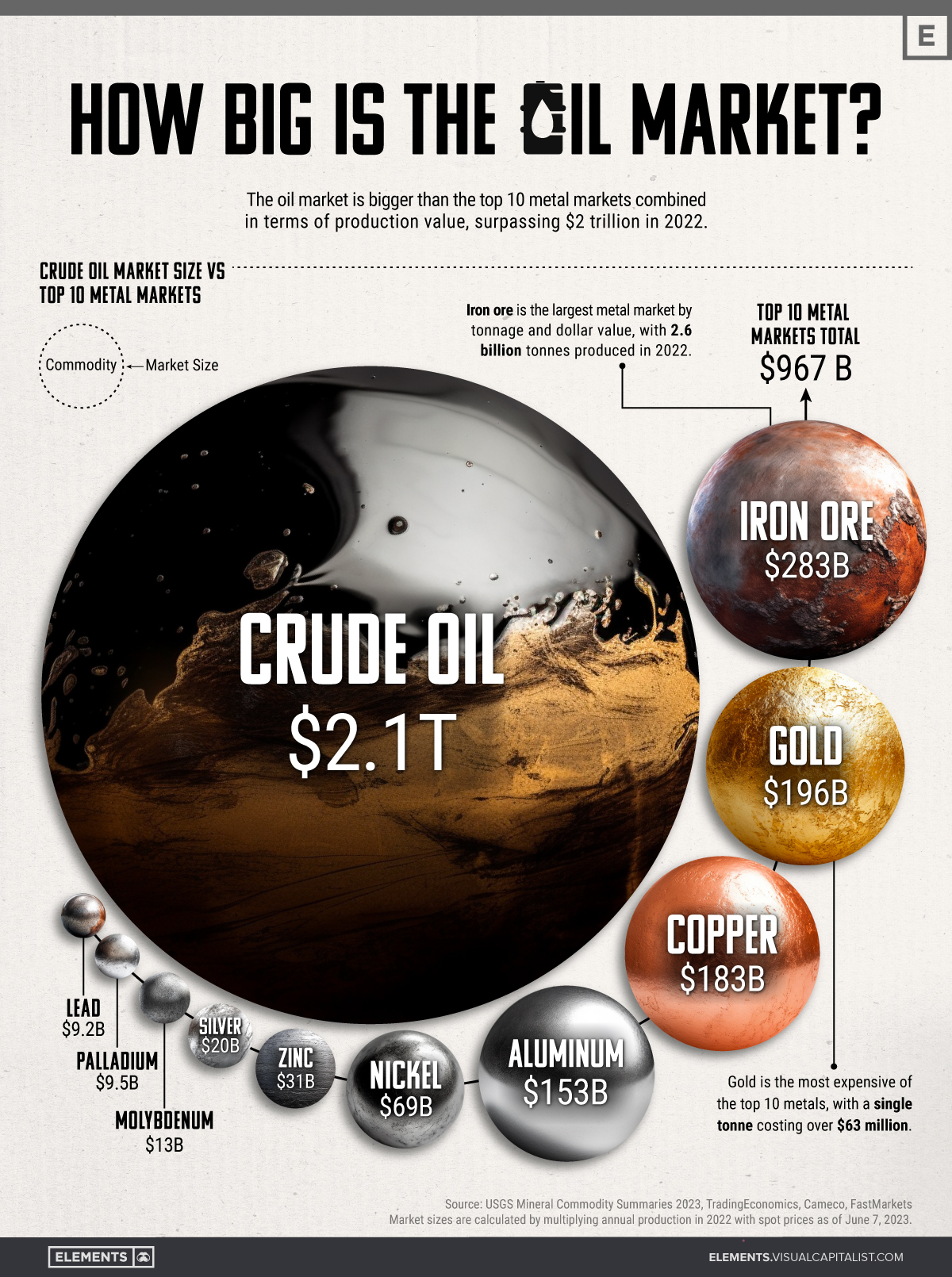

Here’s a great way to visualise the transition (although I may not be selling oil to fund these purchases, as it looks like we will need a lot more of that too in order to effectively transition. And eat).

Source: Elements Newsletter

Passing shots

Here’s a thought: if there was any evidence of alien activity, then I reckon Elon Musk, with more satellites and rockets and having been closer to Mars than anyone, might have seen them according to his latest conversation with Lex Fridman. And yet, he hasn’t. Not a beep. No Martians, no flying saucers, no alien cadavers. Makes you wonder what we are spending all that money on? Talking tech, here’s my latest prediction: Apple is about to launch the Apple Car. Well, I’m not sure that it’s really my prediction. It’s no secret Apple is working on Car Tech and has been in talks with Hyundai and others already. But Apple needs growth and there really are only a handful of industries big enough that would move the dial, the auto-sector being one of them (AI, healthcare, and financials the others). The latest bet on Metaverse with its Vison Pro headsets was a bit of a flop, although I can’t help thinking this was a massive head-fake to make way for something else. Something bigger. Something not to wear. But to drive…

And finally: did you see Rolex and Patek Philippe prices fell to two-year low amid waning demand for expensive watches. Only time will tell if this is the bottom….

Gary Paulin

Chief Investment Strategist, International

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.