- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Tariff Turmoil Redux

Trade tensions spread to the copper and pharmaceutical markets.

By Ryan Boyle and Vaibhav Tandon

Tariff drama was our top theme for the first half of the year. After tension and dread peaked in early April, the theater surrounding world trade calmed following the deferral of the reciprocal tariff plan and successful talks with China. During this relative quiet, markets recovered and growth prospects improved. But the intermission has concluded, and the drama has resumed.

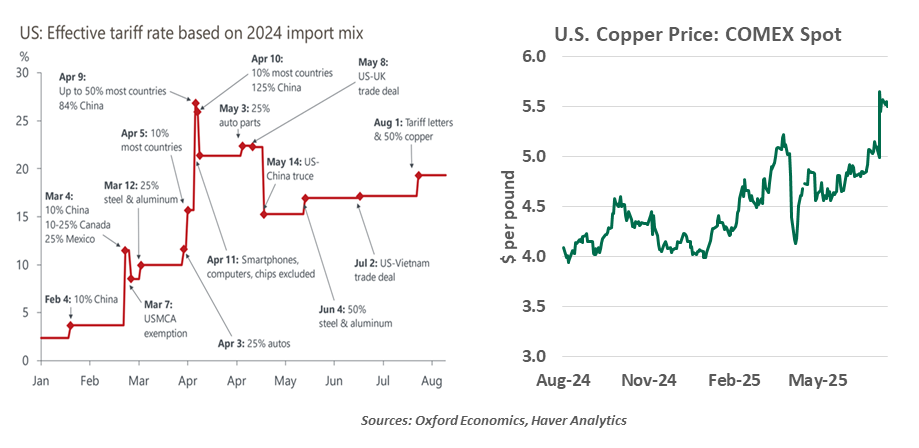

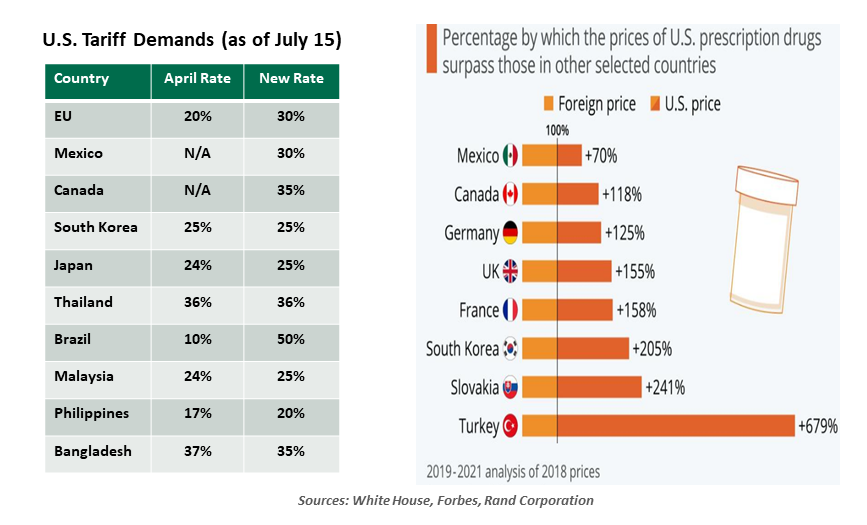

As we discussed last week, the reciprocal tariff plan is set to come back into force on August 1. The White House sent letters to 24 governments, specifying the terms that will take effect on that date. Targeted countries can still negotiate, but they have been threatened with even higher levies if they retaliate. No nation that is in scope has escaped with less than a 20% rate.

Sector tariffs are also back in play. The Trump administration is assessing specific products on national security grounds, employing the same Section 232 provision that was used for steel, aluminum and autos. Levies of 50% on copper and 200% on pharmaceuticals are the latest entries in this series. These penalties, if implemented, will have a significant impact on both the U.S. economy and the economies of nations that ship these critical products to America.

The U.S. is able to generate about half the refined copper it consumes each year, relying on imports for the other half. China dominates global copper refining, but more than 90% of U.S. copper imports come from the western hemisphere. Chile, Canada and Peru are the biggest suppliers.

The base metal has been in heavy demand amid technological advancements and the energy transition. An ideal electrical conductor, it is critical to consumer goods, defense equipment, construction and transportation. Traders have been racing to build their copper stockpiles since the first tariff threat was floated in February. The recent announcement drove the prices of copper future contracts up by more than 12% to an all-time high, and they have continued to hover around those levels since then.

Uncertainty related to country-based and sector-based tariffs has returned.

With demand for copper expected to outstrip supply within the next decade, such high import duties would create shortages and raise costs for U.S. manufacturers. A 50% import duty on copper alone could add up to $110 to the cost of a traditional car and as much as $700 to an electric vehicle, adding to the discomfort of existing tariffs related to the auto industry. Homebuilders will also face higher costs for wiring, on top of on the impact that tariffs are already having on building materials.

Medical products have long been spared from trade wars. While other goods have substitutes and more elastic demand, many essential drugs have no ready replacements.

Major pharmaceutical firms have global operations; medicines are light and easy to ship. The U.S. pharmaceutical industry has thus become highly reliant on imports. Around 40% of the drugs consumed in the United States are produced overseas. Of the more than $200 billion worth of annual U.S. drug imports, almost three-fourths come from Europe (primarily from Ireland, Switzerland and Germany).

Americans already pay much more for prescription drugs than households in other markets. A 200% tariff on active ingredients would lead to massive increases in healthcare costs, borne by insurers and households, further exacerbating disparities. Markets appear to have shrugged off the threat of eye-watering pharma tariffs, as stock prices of drug companies were largely stable.

Higher tariffs would force drug companies to consider moving production to the United States. But building sophisticated facilities from the ground up is a lengthy process, requiring regulatory approvals and substantial investment. According to an analysis conducted by EY, a 25% levy would push up the cost of drugs by nearly $51 billion annually, flowing through to 13% higher costs of medications in the U.S.

Sector tariffs won’t end here. Section 232 investigations are underway for lumber, semiconductors, aircraft, heavy trucks, drones and polysilicon (the raw material in solar panels). Escalations are not limited to matters of trade fairness or national security, as we saw in the early announcements of fentanyl tariffs, and the recent intervention into Brazilian political matters.

Unlike his first term, the current Trump administration has not placed much emphasis on dealmaking. Negotiations have been limited. Free trade agreements are no longer a priority: The few deals that have been announced kept tariffs in place. Bilateral talks are underway between the U.S. and the European Union, India and Mexico, with little to show thus far. Expectations that the U.S. will back down before enactment are starting to feel too optimistic.

Specifics of tariffs are evolving, but their upward trajectory is clear.

The volatility surrounding trade policy is likely to persist. Tariffs are clearly President Trump’s preferred policy tool, and he will continue threatening them as long as he occupies the office. We may get periods of relative calm, but they may prove the exception and not the rule.

Tariffs introduce costs; U.S. businesses cannot make investment decisions while those costs remain uncertain. The tax incentives in the One Big Beautiful Bill fiscal legislation may allow businesses to see a clearer case to invest in domestic production, prompting the repatriation that the administration is hoping for.

Companies and consumers have been forced to endure considerable suspense so far this year, as the Trump trade agenda progresses. The stage has been set for a significant degree of deglobalization, which will be detrimental to a range of audiences. Plot twists will remain frequent, and the ending is still unwritten.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.