Mid-Year Themes

We pause at halftime to recap the highlights of this important year.

By Carl Tannenbaum, Ryan Boyle and Vaibhav Tandon

Editor’s Note: We pause at halftime to recap the highlights of this important year.

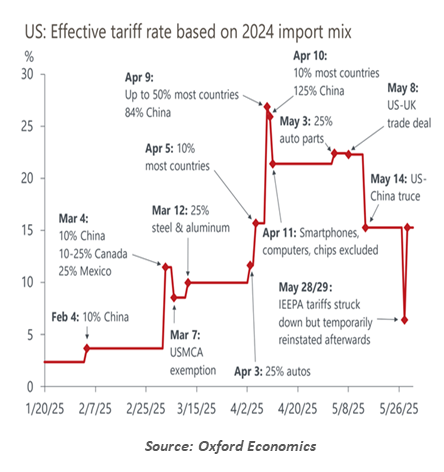

Tariffs have been the dominant theme in economic policy this year. While President Trump has long held protectionist views, his administration’s approach to international commerce has been more belligerent than was seen in his first term. The breadth and depth of frictions have exceeded most observers’ expectations.

Rapid and unpredictable decisions have led to elevated uncertainty. Tariffs have been threatened, escalated, suspended, and challenged in court. The President has changed his stance on tariffs more than 20 times in just five months of being in the office. At times, it has appeared that unintended consequences from tariffs have been appreciated only after they are announced.

Tariff measures implemented this year represent one of the largest tax increases in recent U.S. history. They will hamper growth and raise prices throughout much of the world.

Though boundaries have emerged as the administration steps back from extreme tariff levels, unwillingness to compromise on the 10% minimum is hindering further progress.

The U.S. administration has just two deals to show for its efforts. While structures for negotiations with the U.K. and China were established, concrete treaties remain elusive. Talks with major partners like Canada, Japan and the European Union are proceeding slowly, due to differences over sectoral duties and non-tariff trade barriers.

Recent communications from top U.S. officials suggest that a dozen accords covering America’s major trading partners are expected be completed before July 9. But comprehensive trade negotiations take time, generally spanning years rather than months. Any deals announced soon will likely be in the form of frameworks or narrow agreements. Even if this ambitious target is achieved, smaller nations will be left standing in line, facing harsh measures.

Reforming the global trading system reindustrializing the U.S. economy will be long and difficult undertakings. The year to date is perhaps only the beginning of a prolonged period of uncertainty.

Resilience Over Recession

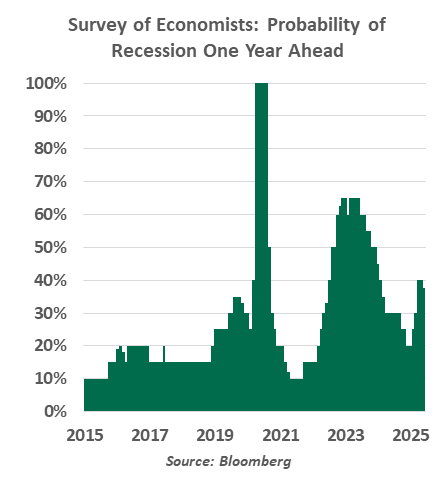

Even a stopped clock is correct twice a day. But for forecasters who expect an imminent recession, that hour has still not arrived.

Anyone who wanted to describe a worst-case scenario did not need to look far this year. The global trade system is in turmoil. The U.S. imports over $3 trillion of goods annually, which were targeted with import taxes that briefly reached 145%. We have receding from those extremes for now, but the effective tariff rate is high and escalatory threats are looming.

And trade is just one of many disruptions. U.S. research institutions are losing funding. Tourism to the U.S. is down. Conflict in the Middle East risked an oil shock or greater kinetic conflict. Enforcement of immigration laws could create a labor supply shock for some industries.

Thus far, outcomes are not living up to fears. The unemployment rate is steady, with jobless claims holding low and announcements of layoffs still rare. Soft data like sentiment surveys plunged as the trade war escalated, but the hard data did not follow its descent.

The pandemic recovery offers a useful guide. Risks in the recovery were legion. Inflation across developed markets reached 40-year highs, necessitating very tight monetary policy. Shortages of goods and workers were common. However, labor markets were resilient, forming a steady foundation for continued growth.

In 2019, we cautioned against conventional wisdom that a recession was “due” as the U.S. reached a record-setting span of economic growth. Cycles do not die of old age, but need a cause of death. In 2020, it was a pandemic. This year, though tense, has not brought about that kind of acute shock.

There are no winners in trade wars. The U.S. will face higher inflation from the costs of tariffs; all other nations will see their exports fall as U.S. trade barriers rise and alliances deteriorate. We have marked down our forecasts accordingly.

Risk of a recession is higher this year than last. But the resilience shown throughout this cycle gives us confidence that time may once again be on our side[CT1] .

Fiscal Frictions

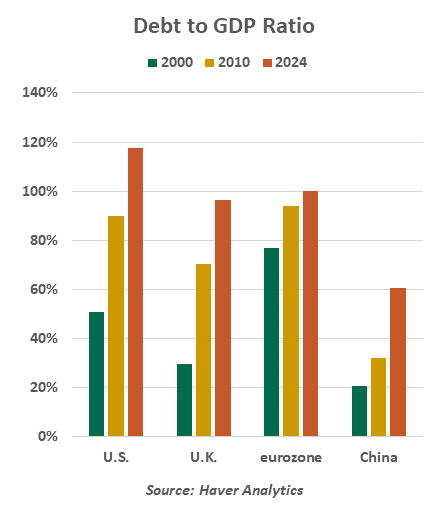

Governments around the world find themselves deeply in debt. The consequences of this position are being more keenly felt, as interest rates have reverted to more normal levels after spending more than a decade hovering near (or in some countries below) zero. In some places, budgets are being pinched; in others, deficits seem to have no limits.

Nations extended themselves in 2020 to head off worst-case scenarios. But even after the pandemic crisis passed, governments were unable to re-center their fiscal positions. Deficits have continued virtually unabated, despite strong economic performance. Debt servicing costs have become the fastest-growing components of many national budgets.

Europe was given a new spending imperative early this year when the U.S. signaled reduced support for NATO. Germany, among other countries, opened its purse strings to seek a new deal for continental security. But the euro area will need to balance its need for increased security spending with the budget limits that keep the common currency credible.

The United Kingdom is contemplating tax increases later on this year, to avoid a repeat of the 2022 gilt crisis. Growth in Britain has been sluggish, and fiscal restraint will not help.

In the United States, debate over the One Big Beautiful Bill Act is in the final stages. The outline will add trillions of dollars to the national debt over the coming decade. Many (including ourselves) have decried the lack of fiscal discipline, but markets have shown little objection to the prospect of enormous increases in Treasury borrowing. Somehow, the U.S. is still getting something of a free pass.

Given the influence of demographics and a world that seems much less secure, all arrows on national debt are pointing up. We may soon find out what the meaning of “sustainable” really is.

The End of Exceptionalism?

When I was in year 7 of primary school, one of my teachers decided that the traditional A-B-C-D-F grading system was too confining. She began giving out marks of “exceptional” to those whose work went above and beyond the top end of the scale. The practice generated quite a stir in the principal’s office, as there were no standards for what constituted exceptional status.

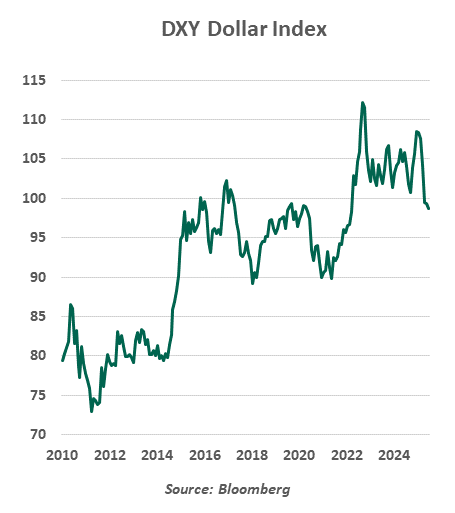

The same can be said for economies which are considered exceptional. The United States has claimed that designation, and not without grounds. Productivity and innovation in the U.S. have advanced at a pace that is well above what has been seen in other developed countries. U.S. markets have performed exceptionally well, with the S&P 500 returning 94% over the past five years. The U.S. dollar continues to hold the mantle as the world’s reserve currency.

But during the first half of this year, questions about American exceptionalism have arisen. The partial retreat by the U.S. from the global trading system and the change of tone surrounding security arrangements have cast the country in a new light internationally. In the financial arena, investors have been taking a look at their exposures to the U.S. in light of recent developments, and some have moved some capital to other locations. Others have increased their holdings of gold to hedge against high levels of uncertainty.

Some analysts have pronounced this the beginning of the end of U.S. hegemony, but this conclusion may be premature. The U.S. dollar has lost about 10% of its value since January, but that was from one of the highest levels in more than 20 years. The term premium within U.S. Treasury securities has risen, but 10-year yields were lower at midyear than they were in January. American equity and bond markets had bouts of extreme volatility in April, but both have settled and performed well since then.

Like my 7th grade teacher, markets grade on the curve. Investment alternatives elsewhere in the world are hardly risk-free, and U.S. assets still look relatively attractive. But in the long term, events of the first half suggest that the U.S. may need to work harder to maintain an exceptional grade.

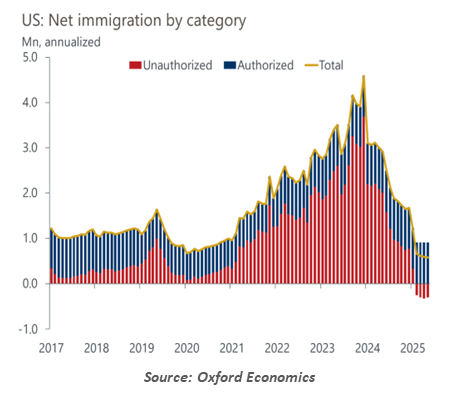

Building A Wall

“Give me your tired, your poor, your huddled masses yearning to be free” is the widely-noted line from Emma Lazarus’ poem The New Colossus. It is imprinted on the base of the Statue of Liberty. But U.S. immigration law is more rigid than the plaque in New York Harbor would suggest. Current policy is especially stringent, with economic consequences in store.

Immigration was an acrimonious issue in the 2024 election. Permissive policy in the U.S., combined with instability in several nations to its south, leading to a surge of new arrivals. Donald Trump ran on a platform of tighter borders. From day one of his second term, controls were reinforced and migration fell. The administration has now shifted its focus to removals. Enforcement has been provocative, to say the least.

The law is the law. But the targeting of certain workplaces to round up undocumented workers shows how important immigrants are to certain sectors of the economy. Further, immigrant-heavy areas are seeing lower activity as residents try to stay out of the spotlight.

Pushback against immigration is hardly limited to America. Canada tightened its policies last year after exceeding targets. European leaders faced backlash after refugees fled the Arab Spring revolutions a decade ago.

Moderate voices will note the need to update immigration policy to offer a path for people who want to work and contribute to their new nation. Legislators have found this goal elusive, and incondite immigration systems continue to limp along.

In the near term, we will watch indicators like job openings and wages to track any labor shortages in immigrant-dependent sectors like agriculture, construction and healthcare. Higher wages could add to inflationary pressures, just as central banks are trying to time the pace of easing. However, a smaller labor supply will help to hold down the unemployment rate and may improve prospects for marginally-attached and discouraged workers.

Lazarus’ poem was not an original feature of the Statue of Liberty, but its spirit inspired immigration policy for generations. The tone has changed, however. The loss of immigrants’ contributions may prove to be colossal.

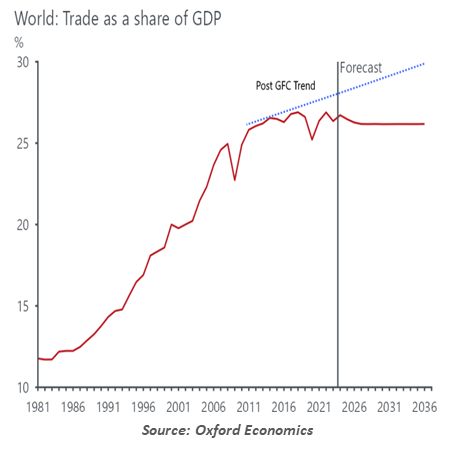

Globalization Rewired

Globalization is on the back foot. This trend did not begin during the first half of 2025; nations have been pulling away from one another since the 2008 financial crisis. Supply chain ruptures during the pandemic added momentum to movements aimed at putting home countries first.

The threat of tariffs and sanctions from the U.S. administration has taken things to a new level. American companies are rethinking everything about where they source and produce goods. Amid pressure on trade with China, U.S. firms are seeking to arrange sourcing from alternative suppliers. Rerouting supply chains for goods like apparel will not be difficult. But businesses could struggle in finding lower tariff suppliers for items like electronics.

Instead of focusing solely on negotiations with the United States, most of America’s trading partners are hedging their fortunes by boosting their ties with other nations. Countries are building stronger partnerships within their own geographic regions, creating blocs of aligned nations that the U.S. may not be a major part of in the future. Many of the world’s fastest growing trade corridors have not included the United States. Global goods flows will be rewired rather than simply reduced.

With the U.S. no longer fully committed to the old global order, rewiring of globalization towards a multi-polar and regionally fragmented global economic system will continue to gather pace. The transition promises to produce considerable shock.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.