Dust Is Settling

The global economy can move past peak trade uncertainty, but restrictions are here to stay.

The year to date has been complicated by a cloud of uncertainty as a new U.S. administration took the world economy by storm. Over the past month, U.S. policy has settled into a steadier state. The outlook for global markets is becoming somewhat clearer. There are still ongoing negotiations and outstanding issues to be resolved, but the trade landscape is better defined.

Trade restrictions will be a consideration for the foreseeable future, weighing on the outlook for all nations. Consumption across the world has slowed; no advanced economy is thriving. Exporters may struggle to replace a reliably eager U.S. consumer market.

Most markets have escaped recession in the year to date, and lower volatility is a favorable omen for continued growth. But lower demand and higher costs raise the specter of stagflation.

Following are our thoughts on how top markets are faring.

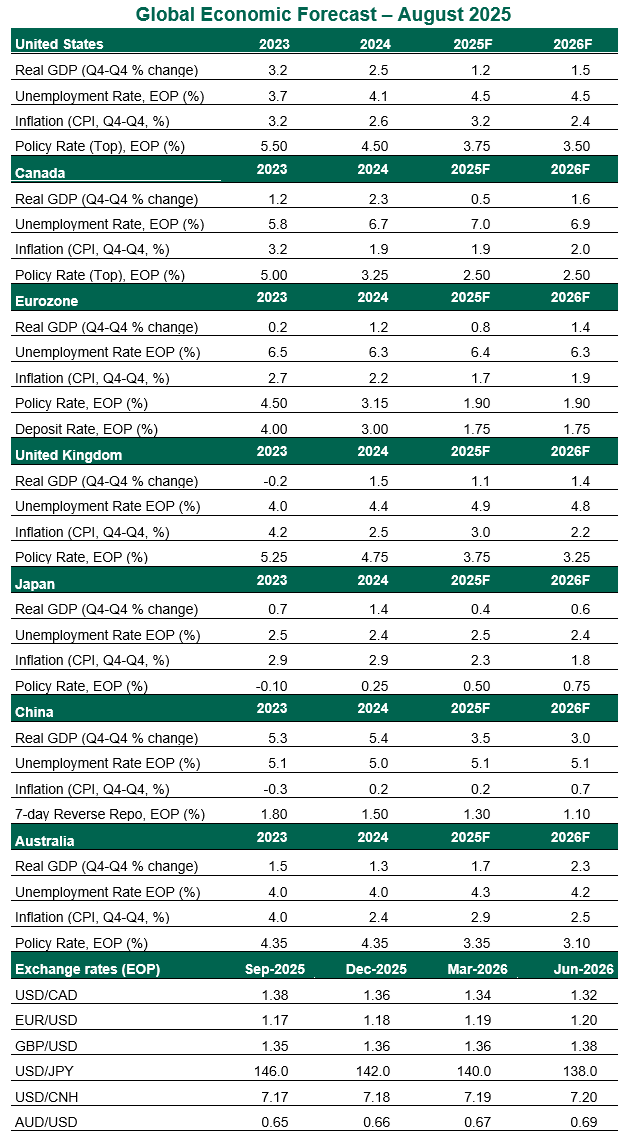

United States

- After a years-long stretch of outperformance, the U.S. economy has faltered in the past month. The weak job creation and significant downward revisions in the July employment report illustrated a stagnating labor market. The Consumer Price Index (CPI) for July showed firming prices for import-intensive goods, though a cooling housing market is helping to keep overall inflation contained.

- The slower labor market clears the way for the Federal Reserve to resume rate cuts. The Fed had the luxury of waiting for inflation to heal as the rest of the economy held up well; if the job market is no longer thriving, support through lower rates is justifiable. At his highly-anticipated Jackson Hole keynote speech, Fed Chair Powell conceded a shifting balance of risks and expressed hope that tariff-driven inflation would be a one-time event. We now expect rate reductions at the next three meetings. However, inflation remains too stubborn for a prolonged or steep easing cycle.

Canada

- Throughout the year, Canada has persevered through unexpected challenges with its neighbor and largest trading partner. A détente that preserves tariff-free trade under the U.S.-Mexico-Canada Agreement should help to renew activity, supported by Canada easing some of its retaliatory measures. The flash estimate of unchanged gross domestic product (GDP) in the second quarter defied fears of recession, and the front-loaded plan for greater defense spending is likely to stimulate activity going forward. The unemployment rate also showed an encouraging tick down by one-tenth from a peak of 7.0% in May, and is likely to hold in a steady range going forward. Core inflation (excluding food and energy) has slowed over the past three months, and now stands at 2.4% year over year.

- The Bank of Canada acted swiftly to support the domestic economy. We expect one additional cut this year to maintain the recovery. However, with inflation calming, unemployment stabilizing, and growth persevering, further easing is unlikely.

Eurozone

- While the evolving trade agreement between the European Union and U.S. helps to remove uncertainty, it also codified high tariffs and did not resolve questions around pharmaceuticals. Slower export prospects will challenge an already sluggish marketplace. The eurozone eked out a marginal GDP gain of 0.1% in the second quarter. Job gains have been slow but steady, while the unemployment rate is holding at a historic low of 6.2% for the past three months. Consumer price inflation is also holding steady at around 2%.

- The European Central Bank (ECB) is encountering an outlook of stable inflation, steady employment gains, and easing external uncertainty. Rates appear to be at an appropriate level for current conditions, and we no longer expect any further easing. If the outlook deteriorates, the ECB has signaled willingness to offer further support.

United Kingdom

- The U.K. also had a better-than-expected second quarter. The economy grew 0.3%, though not evenly; government investment made up for a decline in business fixed capital formation, while households treaded water. Though noisy, the unemployment rate has increased mildly this year. Inflation is on the rise, with the core measure returning to 4% year over year in July. The British economy is less exposed to U.S. trade and instead faces domestic headwinds. The policy of raising taxes on employers is likely to slow wage gains, which could support disinflation.

- The August meeting of the Bank of England’s Monetary Policy Committee illustrated the difficulty of setting policy in the current environment. Higher inflation calls for higher rates; rising unemployment argues for easing. For the first time, the Committee had to re-vote after a tied outcome, narrowly choosing to cut. We expect the Committee’s concerns about sticky inflation will take priority going forward, leaving a cautious path of easing in the reminder of the year.

Japan

- Japan’s trade deal with the U.S. offers some clarity, but few other benefits. The high tariff rates leave the nation’s exports at a disadvantage relative to old norms, especially in the crucial automotive sector. A mildly improving outlook for the rest of the world will help to keep the nation growing at a sluggish pace. The continued decline of the yen is also supportive of exports, though it raises risks of domestic inflation. Consumption stalled in the second quarter after five quarters of growth; renewed domestic demand will be key to keeping the Japanese economy growing. Core prices grew by 3.4% year over year in the past two months, not far from the peak rates seen in the inflationary cycle of 2023.

- The Bank of Japan (BoJ) is in a steady state, holding its policy rate steady and only gradually altering its purchases of Japanese government bonds. While higher inflation and clarity on tariffs could argue for a rate hike, the BoJ will be cautious about further slowing the economy during an uncertain interval. We expect rates to hold steady into next year. In the near term, political upheaval as the ruling coalition is renegotiated could lead to more household stimulus, adding to inflation and pushing yields higher.

China

- Trade volatility benefitted the Chinese economy in the first half, with overall economic growth of 5.3% year over year, led by exports. However, industrial activity and investment fell in July. Tariffs are unlikely to ease, denting U.S. export demand in a more sustained manner. Sluggish demand is evident in rising inventories, which will challenge corporate profits. The U.S. crackdown on transshipment is yet another strike against demand for Chinese exports. The domestic economy is not filling the gap, with employment growth slowing and the property market continuing its correction. Inflation remains very low due to weak aggregate demand: consumer prices were flat year over year in July, and producer prices remain in a decline that began in 2022.

- The People’s Bank of China has provided support to the economy in small but steady increments, which we expect to continue. Central banks cannot generate demand. Moderate efforts to support durable goods purchases were helpful but are unlikely to deliver a sustained boost to growth, and we do not expect much further fiscal accommodation. Policy will also be applied to maintain currency stability.

Australia

- Australia’s economy continues to hold steady amid an uncertain global context. Unemployment has arrested its rise, and incomes are gaining, though the outlook for job creation is mixed. Combined with lower taxes and falling interest rates, domestic demand should remain sufficient to support growth, but not to a heightened extent that could renew a cycle of inflation. Although Australia’s direct exposure through trade with the U.S. and manufacturing supply chains is low, a global slowdown or crackdown on transshipment could have implications for Australia through its impact on its trading partners.

- With inflation calming, the Reserve Bank of Australia (RBA) cut rates again at its August meeting. With consumer price inflation most recently registering 2.1%, near the low end of the RBA’s target, we expect limited further easing. Current rates leave ample room for the RBA to ease further if external conditions deteriorate.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.