Downshift

U.S. growth is shifting into a lower gear.

The U.S. economy is like a finely tuned sports car—powerful, tough, and built for speed. It has managed to climb steep inclines in recent years, competently maneuvering past multiple roadblocks.

But the road ahead is winding. Higher tariffs, persistent inflation, and a cooling labor market are creating new complexities. Financial markets are optimistic, yet consumer and business sentiment is beginning to falter. The Federal Reserve may have to follow a different route. Meanwhile, expansionary fiscal policy provides a supportive backdrop, helping to offset some of the costs associated with disruptive trade measures.

We believe this expansionary cycle still has fuel in the tank, but it won’t be a joy ride as the nation navigates a landscape filled with self-created speed bumps.

Following are our thoughts on the U.S. economy.

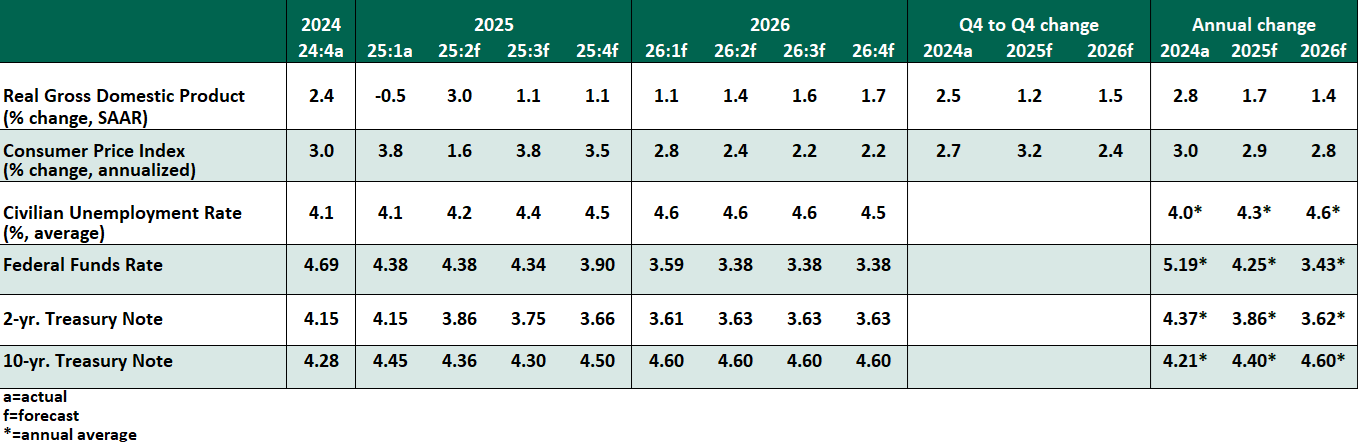

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- Real gross domestic product rebounded in the second quarter, rising at a 3.0% annualized rate after contracting by 0.5% in the first three months of the year. However, the headline figure masks underlying economic fragility. Much of the growth was driven by trade distortions, as the effects of front-loaded purchases faded. Consumer spending rose a modest 1.4%, while business investment decelerated to 1.9%, reflecting some hesitancy to commit to capital expenditures. The core U.S. economy is expected to remain in the slow lane.

- New tariff rates on the vast majority of U.S. goods imports have now taken effect. The average effective tariff rate has surged from just under 3% before February 2025 to 18.3% — a level not seen since the depths of the Great Depression in 1934. While businesses have absorbed much of the initial cost burden, evidence of price increases to consumers is starting to emerge in sectors like furniture, apparel and toys.

- July consumer price data showed further signs of gradual tariff pass-through to inflation, with prices rising for heavily taxed goods such as clothing and certain electronics products. Recent duty hikes are expected to continue feeding into inflation. However, domestically generated price pressures are set to ease, led by improved demand-supply dynamics in the housing market and emerging slack in the labor market.

- The U.S. labor market is showing clear signs of softening. The July jobs report revealed a much more modest employment gain than expected, with only 73,000 jobs added. Even more striking were downward revisions to May and June, which subtracted a combined 258,000 jobs, suggesting the labor market is weaker than previously thought. That said, the labor market is cooling, not collapsing. Wage growth remains robust, with average hourly earnings up 3.9% year over year; an unemployment rate of 4.2% is far from alarming. Job openings are falling, but layoffs remain relatively stable. We expect the labor market to remain in a low-hiring, low-firing phase.

- The Federal Reserve left its benchmark interest rate unchanged at the July meeting. While neither the statement nor the press conference provided direct guidance on the likelihood of a cut in September, we believe conditions are in place to resume easing. Internal policy consensus is also weakening: two members of the Board voted in favor of a cut, marking the first dual dissent since 1993. All eyes will be on the Chairman’s address to this month’s Jackson Hole conference.

The central bank faces a tough balancing act between the threat of another bout of inflation and the rising risk of a hard landing due to deteriorating labor market conditions. Core inflation (excluding food and energy) remains elevated, with the Fed’s preferred measure stuck in a range of 2.6% to 2.9% year over year. Tariffs and expansionary fiscal policy will further complicate interpretation of price dynamics. Given the growing downside risks to growth, we are revising our Fed call to a more active strategy: three consecutive 25 basis point reductions starting in September, followed by one additional cut in March 2026.

- Fed Chair Powell is facing intense pressure from the White House to lower borrowing costs. But the central bank is not the only institution under political scrutiny. In a controversial move, President Trump abruptly dismissed Commissioner of the Bureau of Labor Statistics following the release of the July employment report. The firing has raised concerns about the independence of federal statistical agencies, which play a critical role in informing both policy decisions and financial markets.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.