Look Both Ways

Patient policy choices will support the outlook for growth.

While many lessons have evolved over time, one maxim has never changed for children: look both ways before crossing the street. I reinforced with my children to then look again. We might not see everything on a quick glance, and traffic can change quickly.

Leaders around the world are dealing with risks emerging from all directions. Many nations are finding domestic consumption is receding, with export prospects also limited by a difficult trade environment. Prospects for stimulus are constrained by stretched fiscal budgets. Central banks are increasingly finding their objectives in conflict, most recently in the U.S.; economic data can be parsed to make the case for both cutting and holding.

The key to pedestrian safety is patience. Don’t rush into the street, as a safe opportunity to cross will eventually appear. Policymakers are shifting toward a similar posture of patience. Tariff escalations from the U.S. have slowed, and central bank rate cuts have tapered. After many rapid movements created stress over the past year, a slower and more stable outlook is taking shape.

Following are our thoughts on how top markets are faring.

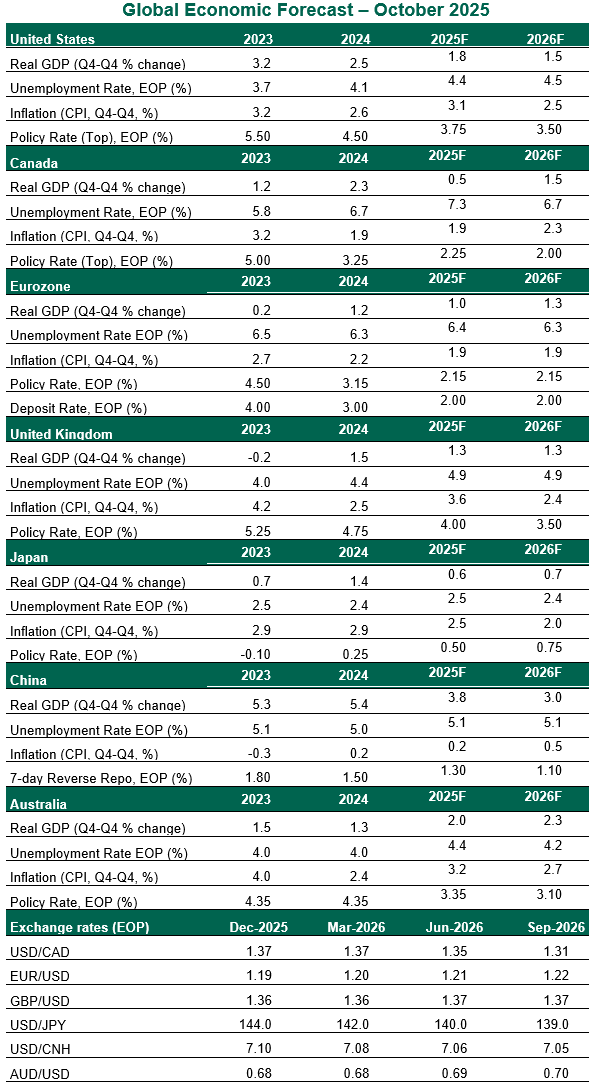

United States

- A prolonged government shutdown has compounded the complexity of assessing the state of the U.S. economy. Private data sources confirm the slowing labor market trend that official statistics had begun to reveal over the summer. The consumer price index (CPI) for September – compiled as a special effort to inform next year’s Social Security payments – showed inflation remained stuck at 3.0% year over year. Though the rate of inflation leaves room for improvement, markets were cheered that it has not accelerated as rapidly as feared.

- U.S. policy has become somewhat more stable. Tariff escalations are less frequent than they were earlier in the year, with the focus of new tariffs narrowing to specific products. The Federal Reserve is also on a more predictable path in the near term. A sluggish labor market clears the way for two more cuts in the remainder of the year, with more to follow in 2026 depending on the path of inflation.

Canada

- Canada’s economy has lingered on the precipice of recession in the year to date. Gross domestic product (GDP) contracted by 0.4% in the second quarter, dragged down by sluggish exports and business investment. Unemployment remains elevated at 7.1%, and while September saw a modest gain of 60,000 jobs, hiring intentions among businesses remain subdued. Calm inflation and a cool economy will allow the Bank of Canada to make one more rate cut this year. Absent reflation, one more reduction in 2026 will likely conclude the cycle.

- Trade uncertainty lingers, with tensions recently renewed and negotiations stalled; the nation’s vast trade relationship with the U.S. remains an exposure. However, Canada’s prospects are not entirely dependent on trade. New fiscal stimulus and lower interest rates should propel the economy through 2026. A federal budget to be released in November should include new fiscal spending that will keep a floor under the economy next year.

Eurozone

- While euro member nations have generally weathered a challenging economic environment well, their fortunes will depend on a shift toward growth support. Retail sales are tame, and industrial production readings from Italy and Germany confirm a low level of activity. Purchasing Managers Index (PMI) surveys suggest a modest rebound ahead, a helpful omen as fiscal constraints will prevent a stimulative surge of government spending, or even bring about government failures. Growth will need to stem from a rebound in business investment and domestic consumption.

- The eurozone economy continues to navigate a delicate balance between disinflation and sluggish growth. Inflationary pressures have largely subsided, with core inflation (excluding energy and food) measuring a stable annual gain of 2.4% or less for the past five months. The unemployment rate remains stable near record lows, holding in a range of 6.2%-6.4% for more than a year. These conditions do not warrant any further easing by the European Central Bank (ECB); we expect no rate changes for the year ahead.

United Kingdom

- Upward revisions to national accounts data show that the U.K. economy has carried momentum through the year 2025. However, the growth outlook for the year ahead remains sluggish and challenged by persistent price pressures. In September, consumer price inflation held steady at 3.8%, defying expectations of an uptick but still too hot for comfort. Food prices fell for the first time in six months, offering some relief to households. Labor market data paints a mixed picture. Unemployment edged up to 4.8%, and wage growth remains elevated at 5%, maintaining inflationary pressure.

- The U.K. fiscal situation is fragile, with deficits through September exceeding the forecast of the Office for Budget Responsibility. Tax hikes in the November budget proposal are a near certainty if the government intends to maintain its fiscal rules, a further headwind to growth. Governors of the Bank of England Monetary Policy Committee will remain challenged by stubborn inflation and a slowing economy. The mix calls for a cautious and gradual path of easing. We expect no further rate cuts this year, and two reductions of 25 basis points in 2026.

Japan

- Growth in the second quarter was revised upward, reflecting healthier consumption and inventory investment; we have upgraded our growth outlook for this year accordingly. However, this has not changed the outlook of Japan facing a slow environment for exports, leaving a challenging outlook for the business sector. Japan has been a frontrunner in its efforts to negotiate a more sophisticated deal with the United States, pledging $550 billion of future investment. However, even the most generous concessions are unlikely to restore its former terms of trade.

- Support for growth will need to come from Japanese consumers, but they will be challenged by persistent inflation and a weakened currency. Inflation gained 2.9% in September, or 3.0% excluding fresh food and energy. Average earnings have not kept pace with the rising cost of living. After tightening its balance sheet holdings, the Bank of Japan is positioning for a further increase in the overnight rate. We anticipate one quarter-point hike early next year, with risk of further tightening if inflation fails to moderate.

China

- China’s economy is holding steady, with GDP growing 4.8% year-on-year in the third quarter, keeping the government’s 5% annual target within reach. Growth is being driven by high-tech manufacturing and exports, which have offset weak domestic demand and a deepening property slump. Retail sales rose just 3.4% in August; consumer sentiment is cautious, and unemployment among young people is high. Deflationary pressures persist, with CPI hovering near zero. The People’s Bank of China has maintained a steady policy stance, focusing on targeted stimulus and trade-in programs to support consumption.

- Chinese policymakers are aware of their growth challenges and are making plans to guide the nation’s momentum. In advance of the 15th Five-Year Plan, the communique of the Central Committee of the Communist Party of China maintained a high priority for supporting industrial production, but also noted that social welfare and equitable growth are essential for long-term stability. This may presage policies to support consumption and rural development, though the timing of any stimulus does not appear to be imminent.

Australia

- Australia’s economy is sending mixed signals. Inflation is trending downward, with headline CPI showing a flat trend from July to August, though still stuck at the upper end of the Reserve Bank of Australia’s (RBA) target range at 3.0% year over year. Unemployment rose to 4.5% in September, the highest level in four years, suggesting the labor market is softening. Despite the rise in unemployment, hours worked increased in September, hinting at a potential rebound in productivity. Domestic demand will stay resilient amid global uncertainty.

- The RBA remains focused on achieving sustained inflation within its 2-3% target band; the current pace of inflation should give the central bank reason to move cautiously. Slower household spending should help to limit inflation going forward. Following three rate cuts in 2025, we expect one further reduction in 2026.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.