Dog Days Ahead

The U.S. economy is growing accustomed to elevated uncertainty.

Summer is a time for many of us to take a break, get away from work, and travel to see something new. But with so many unresolved questions going into the season, we may need to stay close to our screens.

Policy uncertainty remains the leading economic risk. Trade negotiations with nearly all U.S. counterparties are ongoing; tariff reprieves have been limited in their time and scope. Fiscal legislation remains a work in progress, but all indications are that it will widen the deficit. Prospects for lower interest rates are limited.

Worries about recession are elevated, but economic measures are still resilient. “Soft” readings like sentiment surveys are up from their recent lows. In the pandemic recovery, the economy overcame widespread fears of a downturn; a repeat performance may be in store. If worse-case trade outcomes are avoided, we believe the economy can continue growing through the heat.

Following are our thoughts on the U.S. economy.

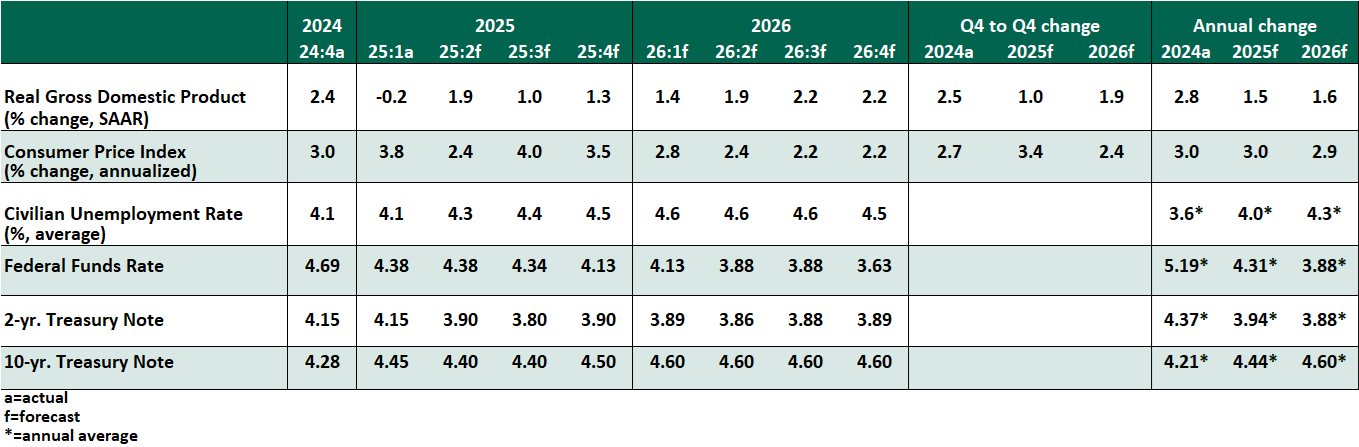

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The labor market has cooled marginally. In May, the economy gained 139,000 jobs, with the unemployment rate unchanged at 4.2%. The details of the report were less encouraging, with substantial negative revisions to prior months, and sectors like manufacturing and retail trade showing job losses. Initial unemployment claims have edged higher, though announcements of mass layoffs remain rare. We expect limited hiring and occasional job losses going forward.

- Inflation remains modest, with the consumer price index (CPI) growing 2.4% over the past year, or 2.8% on a core basis (excluding food and energy). The price index on personal consumption expenditures, the Fed's preferred measure, was similarly contained in April, growing 2.1% overall and 2.5% on a core basis. Shelter remains a key driver of price pressures, but housing cost increases have receded from a very high rate.

Tariff-driven goods inflation is widely anticipated but slow in arriving. Tariffs are a new tax on imports that will flow through to final prices. However, front-loading of inventories has allowed sellers to hold off on price increases. Durable goods prices declined in the May CPI, though a rise in fresh food prices may be a first hint of tariff effects.

- Gross domestic product (GDP) contracted slightly in the first quarter due to a very wide trade deficit, as imports surged to stay ahead of new tariffs. These flows have stopped, and trade will be less of a damper on second quarter GDP. Consumer and business spending gained momentum in the first quarter, and we expect their growth to continue at a moderate pace.

There is a growing belief that the U.S. administration will not push the trade war to recessionary extremes. However, the effective tariff rate has already increased more than tenfold since the start of the year, with lingering risk of escalation. These costs and uncertainties, combined with many purchases already pulled forward, will create slower growth conditions in the second half of the year.

- With inflation above target and the labor market still performing reasonably well, the Federal Reserve can stay patient. Tariffs have added to inflation risk, but several policymakers have characterized them as a one-time shock, not a structural source of inflation. Absent a dramatic rise in prices, we anticipate a next cut in September, and two to follow in 2026.

In recent cycles, Fed leadership has been impervious to political pressure and steadfastly focused on containing inflation. We do not expect this posture to change.

- Yields on longer-tenor U.S. Treasuries have been responsive to policy developments. A fiscal trajectory further out of balance is adding to risks of Treasuries falling out of investors' favor. The recent downgrade by Moody's reflects concerns that are not new and have no easy resolution. We expect yields to remain generally rangebound, with elevated volatility.

- Higher yields have flowed through to higher mortgage rates. Current rates are starting to feel normal to buyers, and purchase activity is thawing. House prices in most markets have continued to appreciate. Reforms to the mortgage lending market could put further upward pressure on rates but will take years to enact.

- The "One Big Beautiful Bill Act" of 2025 is on track to maintain tax rates and fund some spending priorities. Most importantly in the near term, it will raise the debt ceiling, which became binding again in January. The U.S. will be at risk of technical default later in the summer if the ceiling is not raised.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.