Driving Through Fog

The shutdown compounded a sense of uncertainty.

The Northern Trust U.S. Economic Outlook predates our team members’ tenures at the bank. We have maintained a long tradition of offering perspective on recent economic data releases. This month, we have much less data to react to. We are not the only ones dealing with this difficulty.

Federal Reserve governors have shared differing opinions around the metaphor of driving through the fog. In his October Federal Open Market Committee (FOMC) press conference, Chair Powell suggested that fog should cause drivers to slow down and take extra precaution before making any decisions. Governor Waller borrowed the same context to offer a counterpoint: fog doesn’t change the destination or slow motorists to a standstill. We would add that fog is among the most dangerous conditions for driving, with risks of costly mistakes at their highest.

As we write, the government shutdown has just concluded. The resumption of data will be sporadic and potentially incomplete, offering unclear guidance at a pivotal moment.

Available data do not alter our view of the state of the economy. After a volatile start, the year is settling into a stable rhythm, but lingering uncertainty is keeping some sectors below their potential. We have no cause to alter our forecast.

Following are our thoughts on the U.S. economy.

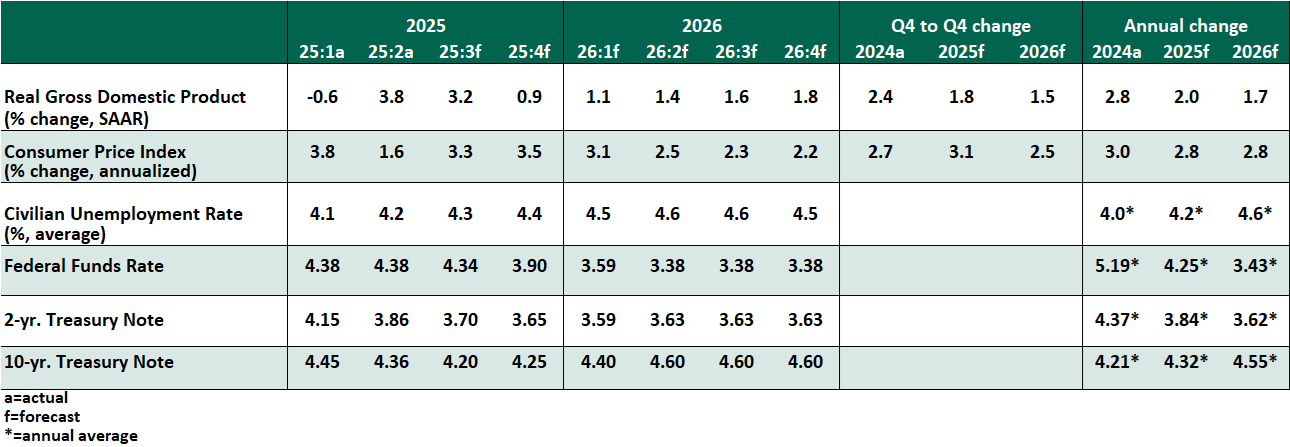

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- Bureau of Labor Statistics staff were summoned back to work to complete the September consumer price index (CPI), needed for annual cost of living adjustments to Social Security payments. The report revealed a 3.0% price gain over the past year, neither cooling as hoped nor reheating as feared. After a prolonged stretch of gains, tame shelter costs are helping to keep overall inflation in check. Import-dependent sectors like furniture, appliances and apparel are showing modest price gains; many tariff costs are being absorbed into margins and have not yet entirely flowed through to final prices.

- At their October 29 meeting, the Federal Open Market Committee (FOMC) cut the overnight rate by 25 basis points. However, expectations for future meetings were shaken. The decision included two dissents in different directions, with one member pushing for a larger cut and another preferring to pause. At the subsequent press conference, Chair Powell emphasized that a cut at the upcoming December meeting is "not a sure thing, far from it."

Powell's reason for hesitation, as well as President Schmid's defense of his dissent, hinged on the uncertainty of sustainably lower inflation. Labor market strains may prove to be temporary, and the committee should not disregard the risk of persistent inflation. Powell also observed that an overnight rate below 4% brings it within the long-run range of estimates of neutral. More cuts are likely in store, but at a measured pace.

We believe the sluggish labor market has not changed, and should offer reason for the FOMC to ease again in December. Recent messaging signals a pause thereafter. The timing of another cut in 2026 will depend on inflation’s path.

The Fed also announced an end to its balance sheet rundown. After December 1, the Fed will cease to roll off Treasury holdings, with a modest expansion as maturing mortgage-backed securities are reinvested into Treasuries. Tight overnight funding could compel a resumption of Treasury purchases next year.

- With the Bureau of Labor Statistics on hiatus, the monthly estimate of private employment from payroll processor ADP gained greater attention. The October report showed a return to job gains of 42,000, following a loss of 29,000 in September; larger employers hired while smaller firms were challenged. The report was neither strong enough to ensure a Fed pause, nor weak enough to compel a path for rapid cuts.

- A handful of prominent defaults have increased concern around credit risks over the past month. From what we have learned thus far, these appear to be idiosyncratic shocks and not systemic events. Financial conditions like credit spreads and volatility have not repriced.

- The shutdown did not affect operations of the U.S. Treasury. Longer-term yields have risen slightly in the face of heightened fiscal uncertainty and rapid debt issuance. We expect these factors to persist as the shutdown concludes, pushing up yields, though the timing has proven difficult to forecast.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.