Weekly Economic Commentary | November 21, 2025

Affordability: Easy To Criticize, Hard To Change

Inflation motivates voters and challenges policymakers.

By Ryan Boyle

A year ago, we were digesting a year of change elections. A majority of the world's population voted in 2024; incumbent candidates and their parties fared poorly. The world had just lived through a cycle of inflation, and voters took out their frustrations at the ballot box. To a marginal voter struggling to make ends meet, candidates promising improvements in affordability sounded appealing.

Special elections in the U.S. at the start this month have reinforced this point. Each race had local characteristics, and none were national referenda. The common message of many winning candidates was that prices are too high and need to be contained.

Policies to control prices, however, will be difficult to craft. Elected leaders have few levers to pull once in office. As fervor around affordability grows, we want to offer a review of past attempts to keep prices in check.

The U.S. endured a long and painful inflationary cycle throughout the 1970s. President Richard Nixon tried to arrest it through price controls, demanding temporary halts to all price and wage increases in 1971 and 1973. These actions dislocated markets. Farmers and ranchers elected not to raise crops rather than sell their wares at a loss; store shelves developed gaps; inflation did not abate.

Nixon's successor Gerald Ford took a softer tack, championing the "Whip Inflation Now" (WIN) campaign. The program encouraged households to be thrifty and retailers to limit price increases, hoping that reminders to tame inflation would lead to better outcomes. But WIN lapel pins could not influence commodities like the price of oil, the core of the inflation challenge at the time. The effort was a flop.

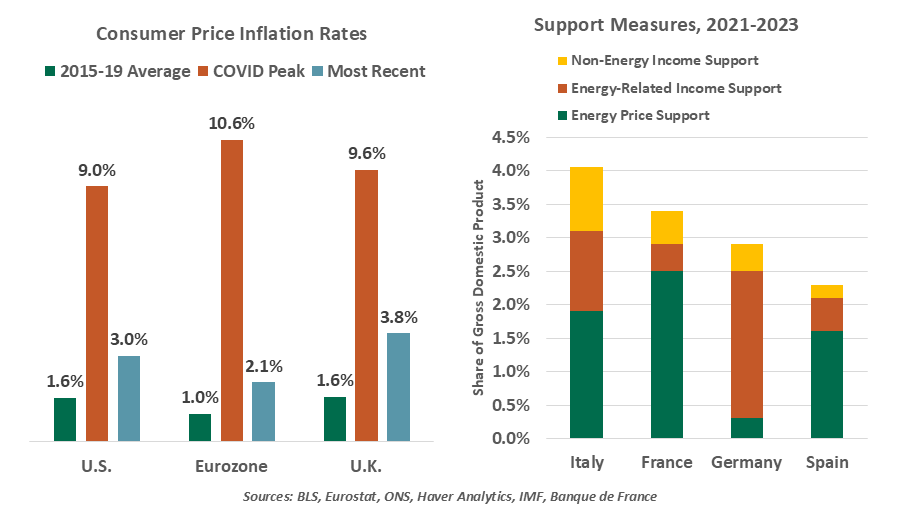

We are still reeling from the inflationary cycle that started the decade, sparked by COVID lockdowns, stimulus payments and the Russia-Ukraine conflict. Leaders around the world heard their constituents' concerns and tried to take action, but they again learned the limits of policy interventions.

Energy prices are critical to the way consumers experience inflation.

European nations undertook a host of measures to contain energy costs, the locus of inflation as Europe's supplies of Russian oil and gas were disrupted. Strategies included price caps for natural gas and electricity, windfall taxes on energy companies' higher revenues, and temporary tax cuts on energy purchases. Some nations like Germany offered vouchers directly to households to pay energy bills, while France intervened by subsidizing fuel prices.

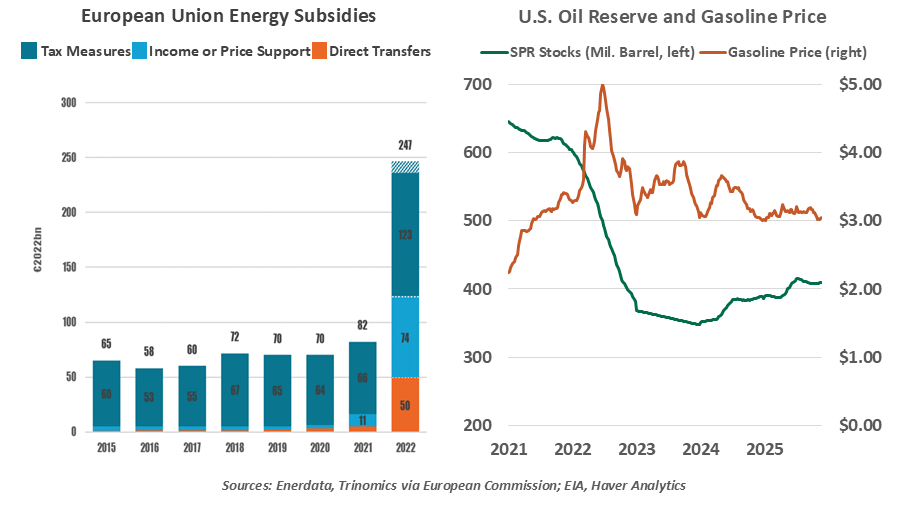

A European Commission study found that energy subsidies reached €390 billion in 2022. An International Monetary Fund analysis estimated that these efforts helped to reduce eurozone inflation by as much as two percentage points in 2022. But to a struggling household, the difference between 8% and 10% inflation is not significant, and higher price levels will persist regardless.

A challenge of temporary supports is that they create a shock when they expire. German fuel prices jumped by €0.25 per liter overnight when retail subsidies expired in 2022, and the end of a fuel tax break for farmers sparked protests.

The U.S. took a different approach, drawing down nearly half the stock of the nation's Strategic Petroleum Reserve. While this ensured a stable supply, it didn't alter global oil prices or relieve the bottlenecks in the fuel supply chain. Prices stayed elevated, and the effort left the reserve depleted.

We list these interventions not to criticize their good intentions, but to illustrate their difficulties and shortcomings. Price controls may prove unworkable and can create unintended consequences. Cutting taxes also cuts government revenue, and subsidies further challenge fiscal balances. Lower taxes and cash support to buyers maintain demand, compounding inflation. And the pain of high prices can motivate change; dulling the price mechanism hinders progress against inflation.

The ongoing sensitivity to the cost of living is somewhat surprising. The rate of inflation has stabilized, and wages are generally keeping pace. However, once we become attuned to prices, the feeling of bad inflation lingers.

Politicians are trying to respond. The platform of the incoming mayor of New York City included a rent freeze, which will discourage residential investment and upkeep. The White House is also floating new ideas. Tariffs have been a source of new government tax revenue: could they fund a round of stimulus rebates to offset inflation? But adding to consumers' spending capacity will keep prices moving up. The cost of housing is a pain point; could a 50-year mortgage make payments more affordable? Unfortunately, the fundamental shortcoming with housing is supply, not credit.

Fiscal measures to control inflation sometimes make the problem worse.

At its simplest, inflation is the result of demand exceeding supply. Buyers bid up prices for scarce goods and services. Inflation can be tamed by increasing supply or reducing demand. Durable policy remedies to these ends are difficult to design and implement.

Cooling demand is the intent of central bank rate strategy. Paul Volcker's massive rate hikes in the early 1980s arrested inflation, but at a painful cost. Marginally reducing demand can escalate to a major recession. Governments can also cool demand by raising taxes, an unpopular proposition.

Increasing supply is easier said than done for most categories. Shelter costs are top of mind, but housing construction is never rapid. Selective tariff reductions, such as on food, may promote imports to offset domestic shortages. Most other markets offer few possibilities for policy to increase supply; cost challenges in sectors like healthcare have no easy answer.

The best remedy to inflation is to increase output and productivity, allowing incomes to advance beyond the prevailing rate of inflation. Technology optimists herald artificial intelligence (AI) as a tool that will unlock new productivity gains. AI is in its early stages, and we cannot yet conclude that it will alter productivity in a widespread manner that overcomes inflation.

The year ahead for major markets features few national elections, though snap elections for tenuous governments like in France are possible. Recently-elected leaders will have time to enact their inflation-fighting agendas. But we do not have high hopes that they will be successful.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.