Fed Preview: How Low Can You Go?

Cuts are in store, but decisions will be weighed carefully.

By Ryan Boyle and Vaibhav Tandon

The Caribbean custom of limbo spread around the world as a party game: Contestants gyrate forward under a bar that is moved lower with each turn. The winner is the last person to pass without falling or touching the bar. The game requires balance, patience, focus, and a fair amount of humility.

At its upcoming meeting on September 16-17, the Federal Open Market Committee (FOMC) is all but assured to resume its cycle of rate cuts. The question facing Committee members will be how low rates can go without losing balance. Holding higher could suppress economic activity; going too low risks reigniting inflation.

Fed Chair William McChesney Martin famously quipped that the Fed acts as the chaperone who pulls the punch bowl just as the party is warming up. After a break, the limbo pole at this party will soon move a notch down. Calibrating its descent will be the FOMC’s challenge. Below, we compare the cases for caution and for rapid easing.

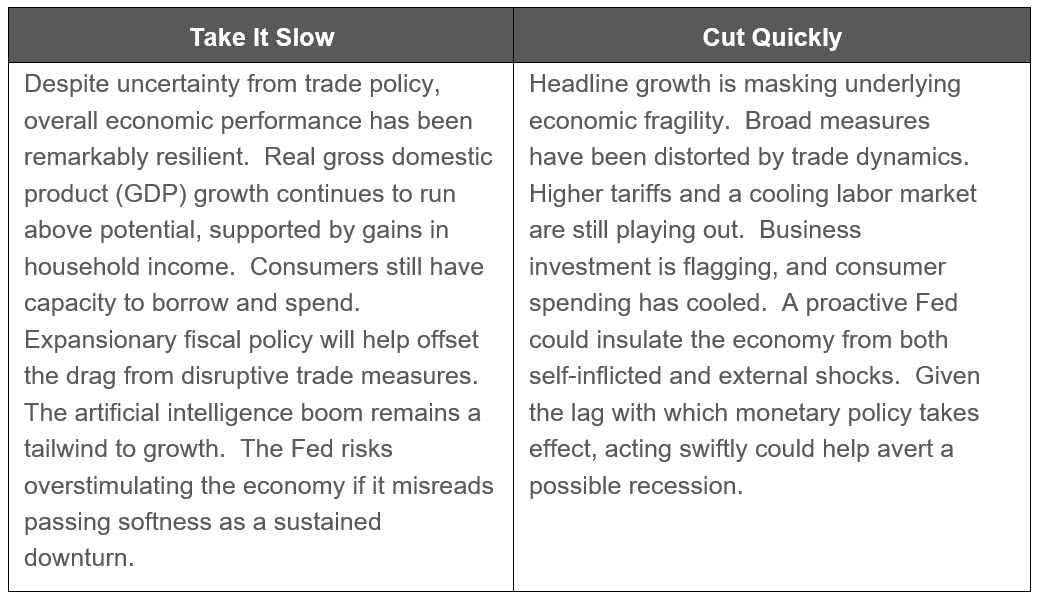

Economic Growth

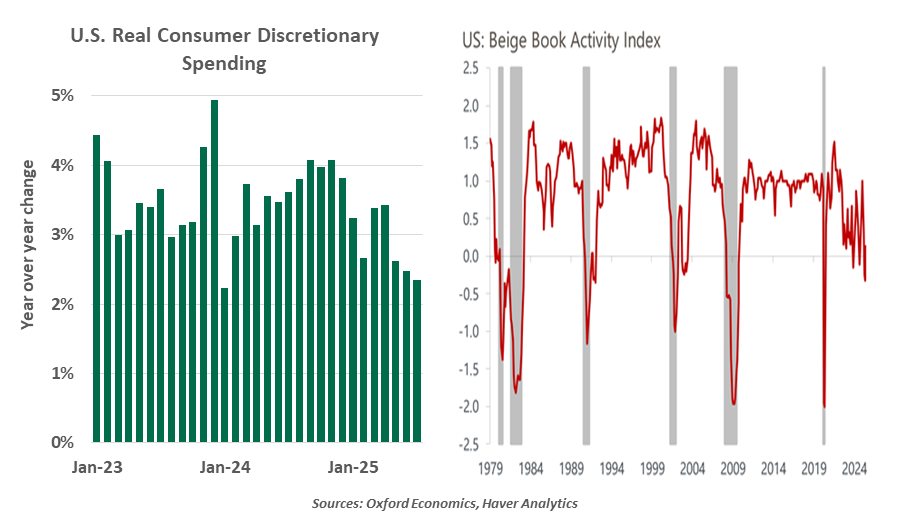

Real GDP growth bounced back in the second quarter, rising at a 3.0% annualized rate after contracting by 0.5% in the first three months of the year. But the core U.S. economy is shifting into the slow lane. Much of the second quarter growth was driven by a bounce back from first quarter trade distortions. With the temporary boost from front-loaded purchases fading, consumer spending is turning sluggish. Business investment is declining, reflecting a growing caution to commit to capital expenditures. Households are bifurcating, as those with the fewest resources fall behind. With tariffs adding to inflation and the labor market showing slack, real incomes may fall.

While no major recession indicators are flashing red, the economy is clearly transitioning to a slower-growth regime. The evolving growth picture strengthens the case for a more

accommodative and preemptive stance from the Federal Reserve.

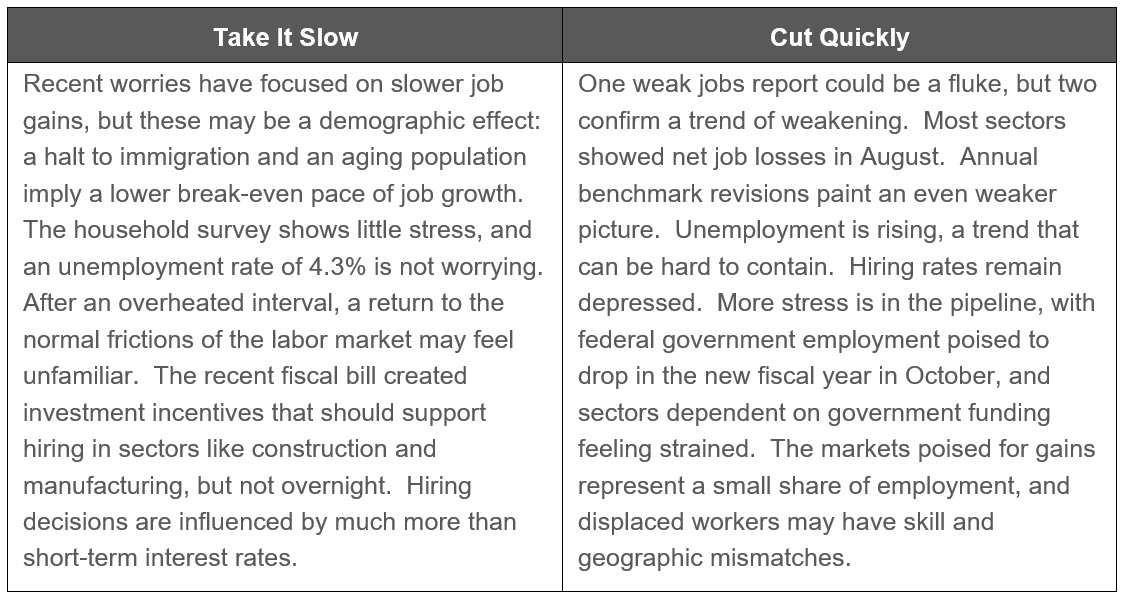

Employment

The labor market has cooled, not crashed.

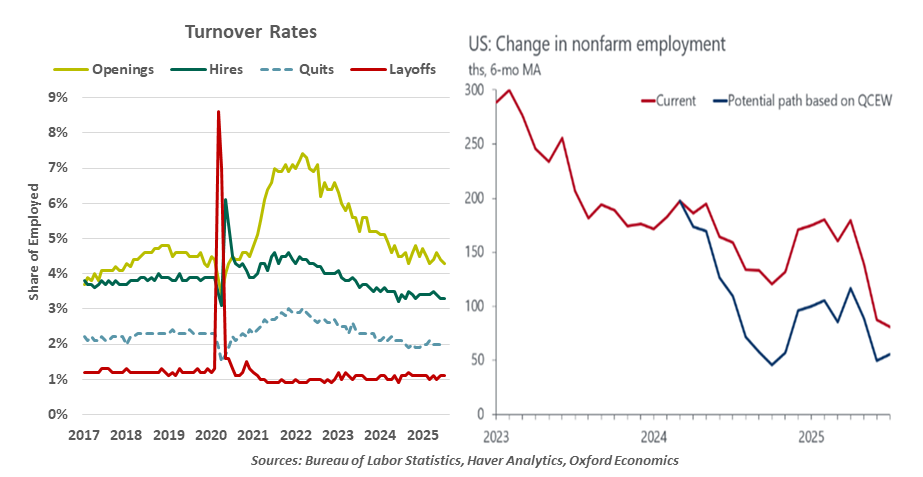

Through this cycle, the labor market showed great resilience, with job creation exceeding expectations almost every month since pandemic restrictions eased. This summer, it changed gears. Payroll gains have slowed, with many sectors falling into decline. Negative revisions to employment estimates have damaged both perceptions of the labor market and confidence in the methods of data collection.

Prevailing uncertainty has cooled hiring, though layoffs have been muted. Weekly initial unemployment claims have held low, but rising continued claims show that workers are having a harder time finding their next job after a termination. The “no hire, no fire” job market cannot carry on in perpetuity. Lower rates could help motivate some hiring plans at a crucial moment.

The labor market has not broken. The rapid jobs gains of recent years were made possible by a high flow of immigration, which has stopped. Panic about the labor market is not yet warranted, and labor market news should not dominate the Fed’s considerations.

Inflation

The Fed seems willing to put its inflation mandate on the backburner, for now.

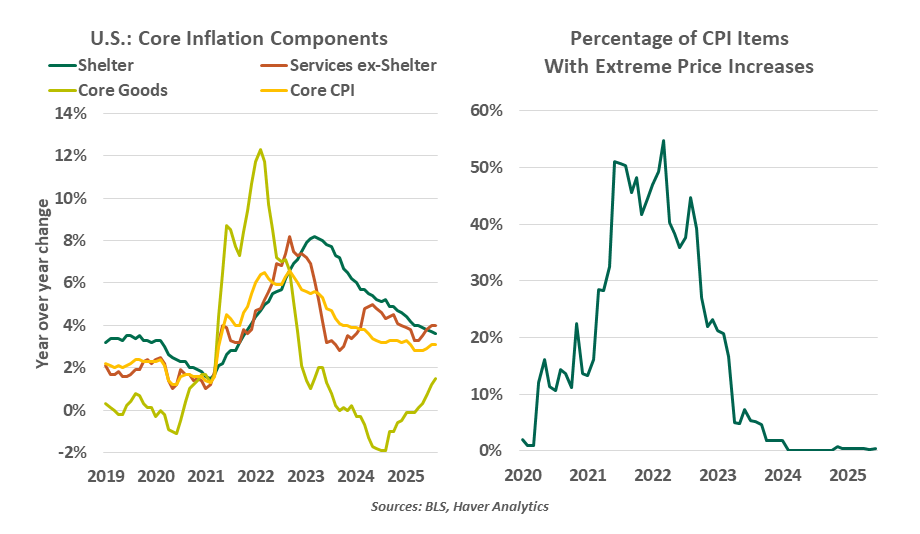

The central bank faces a tough balancing act between the threat of another bout of inflation and the rising risk of a hard landing due to deteriorating labor market conditions. The postulate that tariffs will have only temporary influences on inflation sounds dangerously similar to the “team transitory” contentions of 2021, which proved misguided.

But the focus has rightly shifted toward the employment mandate as signs of economic softening become more apparent. Inflation has been well-behaved across most segments. Price pressures in labor-intensive categories like accommodations and recreation have steadily moderated, in line with wages. Domestically-generated inflation is set to ease further, led by improved demand-supply dynamics in housing and emerging slack in the labor market.

The longer-run drivers of underlying inflation, like wages and inflation expectations, have been relatively benign. However, inflation has not returned to the 2% target on a sustained basis. The key difference now is that economic activity has stepped down and the labor market is no longer tight, conditions that support further moderation in price increases.

Financial Conditions

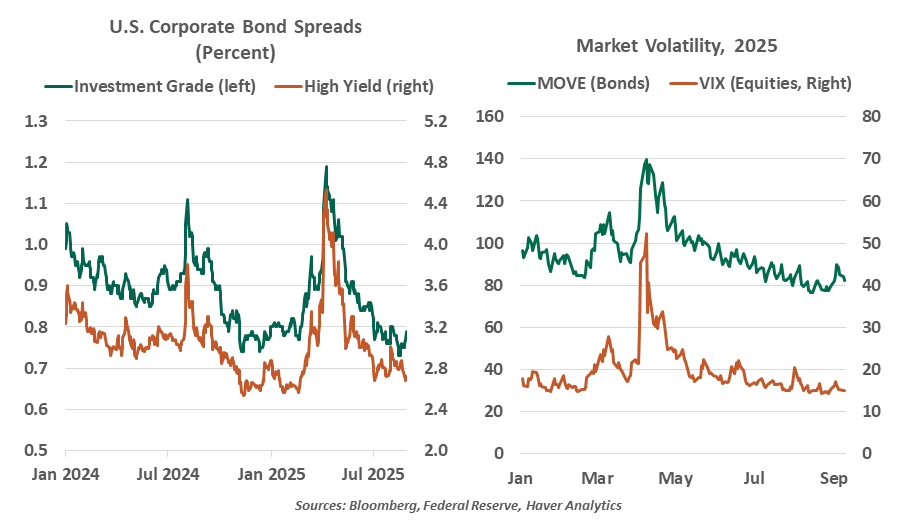

Credit conditions carry an echo of the low-turnover labor market. Outstanding loans are performing sufficiently, but new debt issuance is sluggish. Real estate markets are working through strains. Among commercial properties, office demand has passed through the bottom of its cycle, with demand and valuations gradually recovering. The housing market is stalling: housing starts have not kept pace with demand, and price appreciation is slowing.

In the past year, the Federal Reserve has almost ended its program of quantitative tightening, with only marginal reductions of its U.S. Treasury and mortgage-backed securities portfolio. Liquidity in this market will be imperative as debt issuance rises rapidly following the July debt ceiling increase.

The banking system has offered little reason for alarm, a welcome reprieve after some moments of stress in the wake of rising yields. While the opacity of private equity and private credit vehicles is concerning, high investor interest has left these funds well-capitalized.

Financial markets are showing little strain.

Our View

Fed governors have been consistent in signaling the next move is a cut, with a question only as to timing. Approaching the September meeting, a feared inflation spike did not materialize, and the labor market is weakening. Conditions are in place for a 25 basis point cut at the next meeting.

Arguments could be advanced for jump-starting the cycle with a cut of a larger increment, as was done last September. We believe the circumstances do not yet warrant a large move.

We expect high uncertainty and sluggish hiring will prevail in the remainder of the year. If these circumstances pave the way for a cut in September, they will likely mean cuts in the meetings ahead, for a total of 75 basis points of cuts this year. From there, one additional cut will bring the Fed to the vicinity of neutral early next year, and a pause will be appropriate.

The September meeting will include a Summary of Economic Projections (SEP), including the “dot plot” of rate expectations. Recent iterations of the dot plot showed the governors pricing a higher-for-longer posture, but that was before the labor market stepped down. Estimates of the long-run neutral rate fell into a wide range of 2.6 to 3.9%; arguments can be made for any policy path.

The data will remain the focus of policymakers, and cuts can be justified on data alone. Political pressure will cast a shadow on any upcoming decision by the FOMC. We believe a decision to ease will be consistent with the Fed’s mandate, regardless of who is sitting at the table.

Most limbo players will inevitably tumble, but they hope for a gentle landing. We do, too. The prevailing narrative until recently was a soft landing: falling inflation facilitating rate cuts, without the economy suffering broader harm. Weaker jobs data have raised the specter of recession. Policymakers are now motivated to intervene to support the economy, rather than letting inflation set the pace. The bar is lowering, and the party may pick up.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.