Oil Prices on the Way Down

Low oil prices are welcome news to most households, but not producers.

By Ryan Boyle

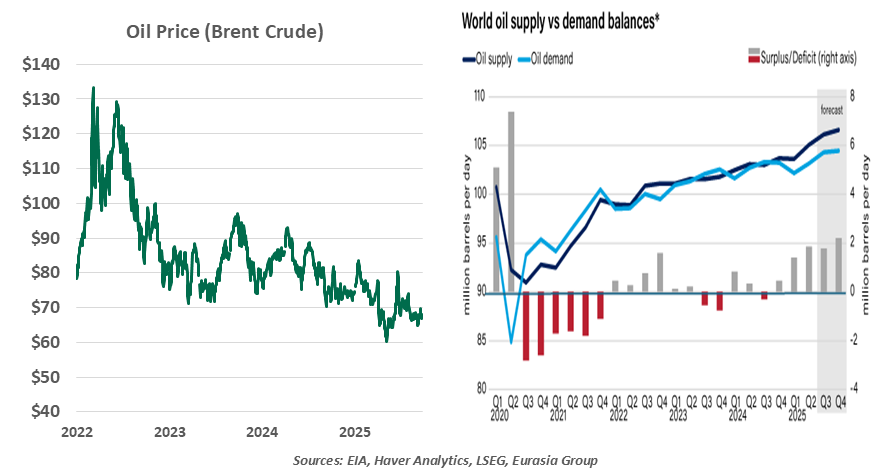

Oil prices are notoriously difficult to forecast. Production can be volatile, and the global oil supply chain is complex. Unexpected price swings can cause pain to businesses and households; pledges from elected leaders to bring down prices often prove to be out of reach. But for the year ahead, a simple combination of falling demand and rising supply are poised to keep oil prices in check.

Everywhere we look, the supply of oil is on the rise. U.S. production rose gradually for years and is still holding near all-time highs. Shale producers have become more efficient, extracting as much crude as possible from existing wells. The nation has become nearly self-sufficient in its energy needs; from a trivial export volume ten years ago, the nation now exports about four million barrels per day (bpd).

Most members of the Organization of Petroleum Exporting Countries (OPEC) are also expanding their production. In recent years, OPEC nations had voluntarily reduced their output by 2.2 million bpd, hoping to preserve a more profitable price point. Those reductions are now being unwound, despite low prices; OPEC nations are seeking to recapture their market share. And conflict in the Middle East did not disrupt supply.

Oil from Russia has become a point of contention; many of the world’s major buyers did not follow western sanctions. The U.S. raised tariff rates on India to discourage its purchases of Russian oil and has threatened the same for other nations. Though its export markets are under pressure, Russia is unlikely to halt, as crude oil represents over 20% of the country’s exports.

Meanwhile, the global economy has stepped down. China is reckoning with overproduction in its manufacturing sector and sharply cooler demand from its largest trading partner, which slows their oil consumption. China has continued to purchase oil despite the slowdown, potentially restocking their reserves. No other nation stands ready to fill the gap created by China’s lower demand.

Industry bodies are watching these shifting dynamics. The US Energy Information Administration (EIA) sees 2.3 million bpd in new global supply outpacing 900,000 bpd in demand growth for the remainder of the year. The International Energy Agency (IEA) forecasts an even larger increase of 2.7 million bpd in new supply, met with even less demand than the EIA predicts.

Low oil prices help households but discourage exploration.

Low oil prices are welcome news to most households. Motor fuel represents over 2% of the household personal consumption expenditures basket, and gasoline prices directly inform consumers’ experience of inflation. The 4.8 million homes that rely on heating oil will also benefit from lower crude prices. Falling energy costs will help to keep inflation expectations anchored, and may free some budgetary space for other spending. Businesses similarly welcome lower transportation costs, at a time that goods prices remain subject to other inflationary pressures.

However, low oil prices weaken the prospect for greater domestic oil production. Most North American reserves are in shale fields which are more costly to explore and mine. An oil price under $60 leaves no retained earnings to expand production; as pandemic-era bankruptcies are a recent memory, shareholder returns are a priority for producers.

Adoption of alternative sources is less compelling when conventional energy is cheap; the U.S. risks falling behind China in green energy sectors. The IEA is even reevaluating their long-term assumptions to reflect the persistence of the oil market. Whereas its prior forecasts had expected the peak in oil demand growth to be reached in 2030, it is now contemplating a scenario of growth through 2050. Ample supply and stable prices will slow the transition away from petroleum.

Experience has taught us the difficulty of forecasting an oil price; we’re lucky to even get the direction of price changes right. But an outlook for stable prices is certainly supportive for growth. The oil market offers a welcome reprieve from the many sources of uncertainty this year.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.