Asia Pacific Economic Outlook | July 10, 2026

Simmering

The return of hostilities in the Middle East has tempered earlier optimism that the conflict was moving toward a lasting resolution. While the situation remains fluid and risks of renewed disruptions persist, Asia Pacific (APAC) economies have so far avoided the more severe consequences that many had feared.

Energy prices have edged higher following the recent flare-up in tension between Iran and the United States, but they remain below levels that would threaten APAC growth prospects. Shipping routes have been gradually normalizing, but the risk of another bout of disruption remains elevated. Any easing in supply chain pressures should help contain inflation and support business sentiment, but the renewed conflict underscores that some of the headwinds weighing on activity earlier in the year have not fully disappeared.

The near-term outlook has become less adverse than a couple of months ago, but geopolitical uncertainty and trade tensions continue to pose risks. As a result, growth is likely to remain constrained even as domestic conditions gradually stabilize.

Following are our views on how major APAC markets are poised to perform.

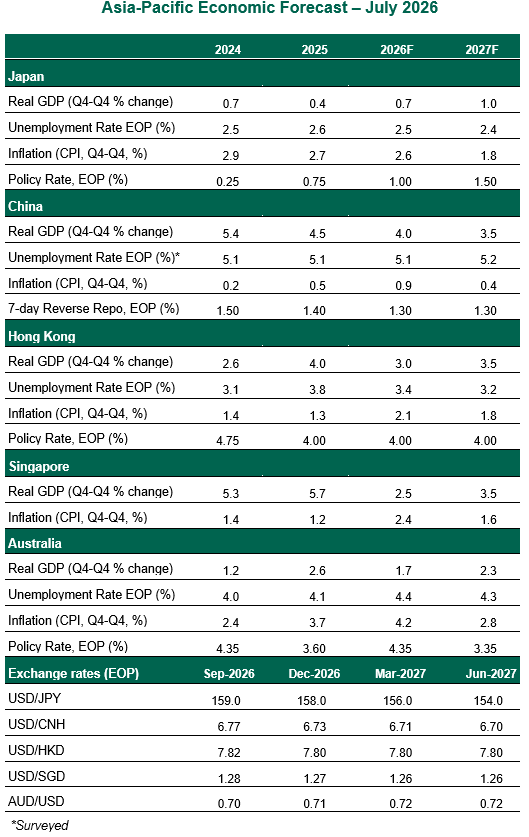

Japan

- Japan has been largely shielded from the worst of the recent global energy shock, helped by government measures that have softened the impact of higher fuel costs. Economic activity continues to tick along. Incoming data on industrial production, bank lending and consumer activity point to an economy that remains resilient despite rising cost pressures. Export performance has also held up well, supported by strong demand for AI-related products and technology inputs.

- Inflation remains contained by international standards, allowing the Bank of Japan (BoJ) to continue gradually normalizing policy. The BoJ raised its policy rate to 1%, the highest level in more than three decades, and outlined plans to end quantitative easing by tapering government bond purchases through 2027. But the move wasn’t enough to suspend the downward pressure on the yen amid widening interest rate differentials with the U.S. We expect further measured rate hikes as policymakers balance inflation control, currency stability and economic growth. Currency intervention remains a possibility if downward pressure on the yen persists.

China

- China’s economy has continued forward in spite of recent Middle East disruptions, supported by its large strategic petroleum reserves and control over key fertilizer exports. Higher commodity prices pushed producer price inflation to 4.1% year over year in June. However, the inflationary impulse has largely stopped at the factory gate: consumer price inflation decelerated to 1.0%, reflecting weak domestic demand, limited pricing power and margin pressures. Elevated inventories and a still-struggling property sector continue to weigh on activity. AI-related industries have become an important driver of exports, but this concentration is also attracting greater scrutiny beyond Washington. China will likely need stronger internal demand as its exports will face an increasingly difficult external backdrop.

- Policymakers appear committed to stabilizing growth and are continuing to rely on incremental measures. The People’s Bank of China introduced overnight reverse repo operations late last month, adding a new tool to manage short-term liquidity and borrowing costs while preserving the seven-day reverse repo as its primary policy rate. Rate cuts and liquidity support will help cushion the slowdown, but are unlikely to generate a sustained rebound in activity.

Singapore

- Singapore continues to grow like an emerging market, registering a strong 6% annual rate of expansion in the first quarter. Gains were broad-based across all sectors; the ongoing AI investment boom and firm capital spending should continue to underpin activity. Household consumption remains the main area of softness, with retail sales growth slowing to 3.0% year over year in May from 5.4% in the previous month. Singapore is not unique in being covered by the U.S. administration's Section 301 investigations, but its trade-dependent economy makes it especially exposed to a more protectionist trade regime.

- Inflation risks prompted the Monetary Authority of Singapore to tighten policy in April, but the central bank also signaled growing caution about downside risks to growth. Unless the energy shock intensifies, we do not expect further tightening in July. We think April's policy adjustment was a one-and-done move.

Hong Kong

- Hong Kong’s economy is on a firm footing, with first-quarter growth reaching 5.9% year over year. Trade activity remained a key source of strength, with exports and imports continuing to expand at a double-digit pace, despite heightened geopolitical uncertainty. Hong Kong has also been relatively insulated from recent Middle East-related disruptions given its limited dependence on Gulf energy imports and its services-oriented economic structure.

- U.S. monetary policy remains a key variable for Hong Kong, given the Hong Kong dollar’s peg to the U.S. dollar and the city's position as a regional financial center. Speculation in the U.S. has shifted to rate hikes amid elevated inflation, though we expect a prolonged period of unchanged rates from the Federal Reserve. Higher-for-longer U.S. interest rates would keep financial conditions relatively tight in Hong Kong, slowing the recovery in property markets and tempering capital market activity.

Australia

- Monetary tightening and the Middle East conflict have proven to be a drag on activity. Confidence indicators have weakened, household spending fell in April after a strong first quarter, and the housing market has cooled down. Although the unemployment rate dipped to 4.4% in May, labor market conditions remain consistent with a gradual softening.

- Headline inflation moderated two-tenths to 4.0% year over year in May, an improvement largely driven by lower energy costs as underlying price pressures remain sticky. Yet, the case for further policy tightening has diminished. At its latest meeting, the Reserve Bank of Australia noted that financial conditions are already somewhat restrictive and that economic activity is slowing across a range of sectors. Barring a renewed external shock, we do not expect additional rate hikes, as they would risk placing additional strain on activity.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.