Global Economic Commentary | May 27, 2026

Knocking At the Door

Stagflation remains at bay for now, but risks are building.

An unexpected rap on your front door is sometimes cause for anxiety. You are not sure who or what is out there, wanting to get in.

Markets are anxious about prospects for stagflation. For now, the global economy is keeping it at bay. But with energy flows under strain and inflation stirring again, this unwelcome guest may upset households around the world.

Most markets have been very resilient in the face of the war. But the longer disruptions persist in the Strait of Hormuz, the greater the risk that growth begins to soften just as price pressures pick up. Oil prices are not fully pricing a sustained disruption, but longer-term bond yields reflect growing pessimism about inflation. A renewed rise in energy prices and further elevation of borrowing costs could quickly tighten financial conditions.

Following are our outlooks for the world’s major markets.

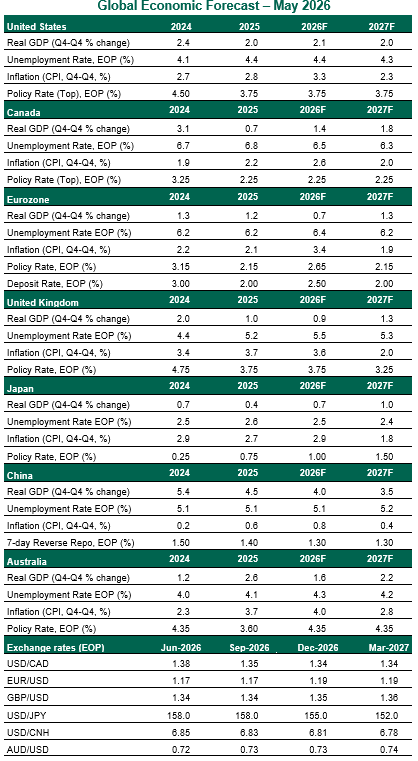

United States

- The United States has avoided major fallout from the Iran conflict. Incoming data continues to suggest economic resilience, with the labor market still a key support. But energy prices have moved higher with little near-term relief in sight. Headline inflation rose to 3.8% year over year in April, with core at 2.8%. Notably, price gains are reappearing in less typical categories such as apparel and technology, likely reflecting lagged tariff effects.

- The Federal Reserve held rates steady in late April, but a rare three-member dissent against easing language points to a more divided committee. With policy conviction shifting, we have removed our expectation of a rate cut later this year. Incoming Fed Chair Kevin Warsh will have to navigate a more fractured and assertive Fed.

Canada

- Canada's gross domestic product (GDP) is growing again, after contracting at the end of last year. Domestic demand has improved, but the data reflects the period before energy markets were disrupted. Domestic headwinds are building, with a softer labor market and slower population growth set to weigh on household spending in the near term. Fiscal policy should continue to provide a degree of support, helping to cushion the slowdown in growth.

- The upcoming United States-Mexico-Canada Agreement review on July 1 is a key inflection point. Our base case assumes free trade will prevail, but the risk that frictions persist or intensify remains material.

- Inflation dynamics present a mixed picture for policymakers. Headline measures rose 2.8% year over year in April, driven by higher energy prices and a favorable base effect from last year’s removal of the consumer carbon tax. However, underlying price pressures remain subdued. Core inflation was notably soft, reflecting slack in the labor market. This leaves the Bank of Canada in a patient position.

Eurozone

- Growth in the eurozone is losing traction, with forward-looking indicators pointing to a pronounced slowdown. A second consecutive decline in the Purchasing Managers’ Index (PMI) in May has raised the likelihood that activity will contract in the second quarter. While hard data has yet to reflect a meaningful spillover from the Middle East conflict, the deterioration in sentiment is broad-based and typically leads the cycle. Policy support will be limited: fiscal measures announced so far are modest compared to the 2021–2022 energy shock, constrained by tighter public finances. The net result is a weaker growth backdrop.

- Headline inflation rose to 3.0% year over year in April, and is likely to peak in the third quarter as energy effects pass through. Second-round effects remain contained, but the risk of broader pressures is rising. Against this backdrop, the European Central Bank held rates steady in April but shifted tone, with hikes now in view. We expect two 25 basis point increases over the summer, taking the deposit rate into mildly restrictive territory.

United Kingdom

- The U.K. economy started the year on firm footing, with GDP rising 0.6% in the first quarter, a step up from the modest 0.2% recorded at the end of last year. But forward-looking indicators are becoming less reassuring. The composite PMI fell sharply in May, pointing to a loss of momentum. The economy now appears at greater risk of stalling, particularly as political uncertainty intensifies. Longer-term bond yields have surged to multi-decade highs. A change at the top could bring a shift toward looser fiscal policy and higher borrowing, which the market will punish.

- The British labor market is also showing clearer signs of cooling. Unemployment edged higher in March to 5%, while vacancies declined. Wage pressures are easing, with private sector pay growth dropping to 3% year over year, a rate considered consistent with price stability. Inflation decelerated to a 3% annual rate in April, driven by downward pressure from regulated and indexed prices. While higher energy costs will push inflation higher in the coming months, we expect the Bank of England to keep Bank Rate at its current restrictive level over the forecast horizon.

Japan

- The Japanese economy extended the momentum built late in 2025, with real GDP rising a solid 0.5% in the first quarter of this year. Strong external demand from the ongoing AI-driven cycle should continue to support Japan’s export sector. However, domestic demand will be constrained. Higher energy costs and elevated uncertainty will weigh on consumption, with survey evidence already pointing to a pullback in discretionary spending by households. Fiscal policy is moving back into focus. Prime Minister Takaichi has announced a supplementary budget of around 0.5% of GDP to cushion the impact of rising commodity prices. A reduction in the proposed consumption tax on food is also under consideration. As inflation rises and fiscal worries grow, long-term yields may increase and the yen may fall, deepening the trade shock.

- Proposed policy measures should help contain inflation. But if instability in the Middle East persists, a sharper rise in utilities costs may call for another round of fiscal support later this year. The broader concern is the emerging mix of rising cost pressures and weakening real incomes, which increases the risk of a stagflationary drift. A cautious, measured approach will be the most effective course for the Bank of Japan.

China

- China’s strong start to the year is giving way to a more subdued growth profile. April data pointed to a broad-based loss of momentum, with retail sales and industrial production slowing and fixed asset investment contracting. Exports should continue to provide a key pillar of support, but the external backdrop is becoming less favorable as disruptions linked to the Middle East weigh on global trade, even as U.S.–China relations stabilize. At home, the property sector remains a persistent drag, with little evidence of a durable bottoming-out. The result is a familiar imbalance: an economy driven by external demand, while domestic activity struggles to gain traction.

- Price dynamics are also shifting. Higher energy and input costs are generating a modest reflationary impulse, evident in April’s firmer consumer and producer price readings. But this is not yet a sign of a healthier demand cycle. Sustained reflation would require a meaningful increase in domestic demand, which is not our base case. Calls for more forceful policy easing will grow as growth softens, but authorities are expected to remain focused on targeted measures aimed at stabilizing the economy rather than delivering a broad-based impetus.

Australia

- Australia’s economy is holding up, but the outlook is increasingly tied to the Iran conflict. Higher energy prices are expected to slow household consumption in the near term. As this drag fades, higher interest rates over the forecast horizon will continue to keep activity in interest rate‑sensitive areas such as consumption and housing in check. The federal budget has added another layer of uncertainty. The removal of tax breaks on existing homes and changes to capital gains tax have unsettled investors and are likely to cool housing activity in the months ahead.

- Resurgent inflation has forced the Reserve Bank of Australia (RBA) to lead

developed markets in rate hikes this year.

Forward indicators suggest firms are passing on higher prices swiftly, implying

further upside to inflation readings. But

recent loosening of labor market conditions will keep the RBA on a prolonged hold.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.