Weekly Economic Commentary | January 30, 2026

Health Care Headaches

Neither relief nor reform are in sight for health costs.

By Ryan Boyle

Affordability and the cost of living have become frequent topics of conversation. Costs rose, but incomes did not immediately keep pace. The rate of inflation has moderated, but consumers remain sensitive to high prices, worried they are falling behind. Higher prices occur when demand exceeds supply, and level off when balance is restored. Many of the latest inflationary challenges are in sectors where equilibrium will be difficult to reach.

Healthcare is one of them. The sector is suffering from a chronic malady of rising costs. Demand for health treatments will never abate; illness, injury and aging are simply parts of the human experience. However, the capacity of the U.S. healthcare system is not keeping pace with the aging population and innovative treatments. Growing demand and limited supply lead to higher prices.

Of late, costs are on the rise as novel therapies come to market for more specific illnesses. Breakthroughs in gene therapy and cancer treatments are tremendous advancements, but their high development costs are spread across fewer patients. GLP-1 drugs offer promising outcomes for a growing array of symptoms, but insurers are hesitant to cover the high price of using them for non-critical applications.

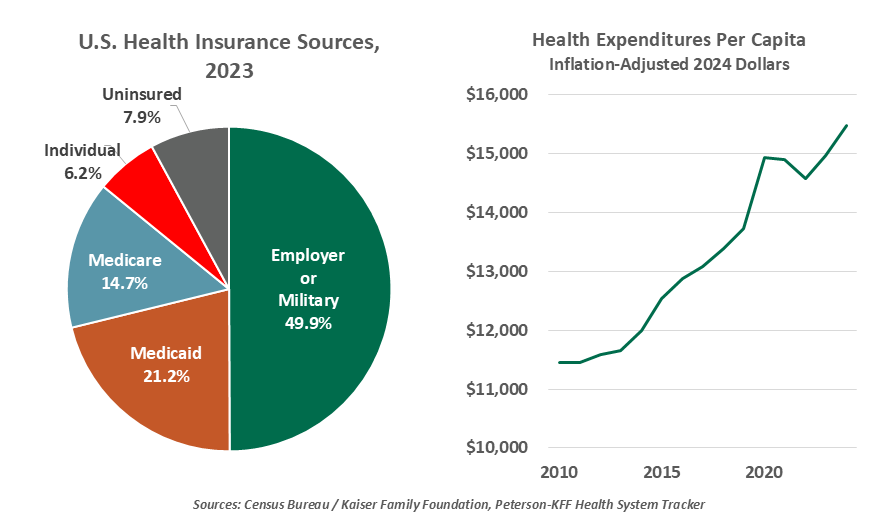

Most citizens rely on health insurance to access care. The majority of consumers receive insurance through their employers; those over 65 or of low income qualify for federal insurance programs. A subset of consumers purchase directly from insurers.

However it is acquired, health care and health insurance are getting more expensive. A survey of employers found the average cost of family coverage reached almost $27,000 per year in 2025; this figure represents a cumulative increase of 26% over the past five years. Fortunately, most workers are shielded from the full extent of this inflation, as employees pay an average of only 25% of premiums for health coverage.

The federal government is the largest individual payer in the health economy. It funds Medicare, Medicaid, and federal employee benefits, along with directly providing care to the military, veterans and prisoners. All federal expenditures are under new scrutiny. Last year’s “Big Beautiful” reconciliation bill set a path of cutting Medicaid funding (subsidies to states for healthcare for the poor) by $1 trillion in the decade ahead. This past week, health insurers were shocked by the announcement that Medicare reimbursement rates will be held flat in the year 2027. Retirees will not welcome the higher gap insurance premiums that are likely in store. As this major payer pulls back, private insurers will shoulder a greater share of providers’ expenses.

Many forces are pushing up healthcare costs.

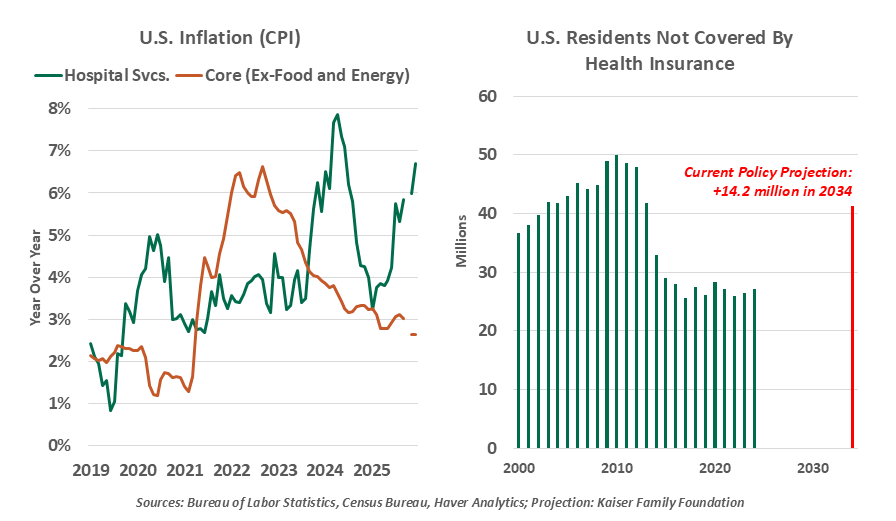

A third cohort in the health insurance spectrum is at particular risk. The Affordable Care Act (ACA) passed at great political cost in 2010, and remains controversial today. But it did succeed in expanding access to private insurance for those without employer plans. As more and more workers have transitioned from payroll jobs to “gig” employment, the ACA has attracted more registrants; enrollment grew to over 24 million people in 2025.

To keep costs affordable, 93% of those using the ACA receive tax credits for purchasing coverage. These preferences were eliminated in last summer’s reconciliation bill, and were at the heart of the 2025 government shutdown. The end of enhanced subsidies this year will lead ACA premiums to more than double for 22 million enrollees, putting the cost out of reach for many households. More healthy consumers may opt out of insurance, damaging the risk pooling that ACA supported. ACA enrollment has already fallen by 1.4 million members this year, and the Kaiser Family Foundation forecasts over 14 million more people will go uninsured in the decade ahead.

After long promising to improve on ACA, President Trump revealed the Great Healthcare Plan this month. The one-page document enumerates which reforms the president would want to see. The outline aims to lower drug costs by forbidding pharmaceutical companies from charging higher prices in the U.S. than they collect in other countries. It pushes for more prescription medicines to be sold over the counter. It proposes cash rebates directly to consumers to buy health plans, rather than subsidizing insurers as ACA does. The plan also calls for more plain-language price transparency from insurers, echoing reforms made in ACA. No mention is made of substantive reforms to insurance carriers or healthcare providers.

Other aspects of the current administration’s agenda have not helped reduce healthcare costs. Suppliers for low-margin generic drugs are concentrated overseas, and pharmaceuticals had to be excluded from many new tariffs. Additional tariffs loom from the section 232 pharma investigation. While tariffs can lead to more domestic production, the resulting drugs may be more expensive. And the labor force in healthcare facilities has a higher concentration of immigrants; tighter policy is raising the risks of capacity constraints and inflationary labor shortages.

Reform proposals meet skepticism from the public and elected leaders.

By results alone, the U.S. healthcare system is difficult to defend. Costs per person are higher than any other country. Health outcomes like life expectancy and infant and maternal mortality are worse than other developed nations. Patient satisfaction is low, while worker attrition is high. Ideas for reform are abundant. Inter-state insurance deregulation and a public insurance option fell out of ACA negotiations, but they could be resurrected. Inertia must be overcome: transitioning to a new system will be risky, and the outcome can’t be assured to be an improvement. No reform could ever make a health system entirely free or perfectly effective.

Doctors will attest to the need for preventive care. Small problems caught early can be treated easily, before they fester into larger maladies. The longer the U.S. puts off its healthcare problems, the worse the symptoms will be.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.