Weekly Economic Commentary | April 2, 2026

The War In Iran Will Stress National Budgets

The burden of war on public finances is growing.

Editor’s note: we’re publishing an abbreviated edition this week, in advance of the holiday weekend.

By Carl Tannenbaum

The war in Iran has been costly, in a number of ways. First and foremost, the humanitarian consequences have been substantial: the price paid by those in harm’s way is immeasurable.

For countries further from the fray, the financial toll of war takes several forms. Those involved in the fighting are spending substantial sums to prosecute their efforts. The war has cost the U.S. an estimated $20 billion so far; Congress has been asked to pass a $200 billion supplement to the defense budget to allow the U.S. arsenal to be replenished in the coming years.

Israel’s operations have cost that country an estimated $6 billion to $7 billion; this is a steep cost for an economy that is about 2% the size of the United States’. Gulf countries are using scores of expensive interceptors to counter missile strikes. When damage is done, aid packages to support repairs can be sizeable.

To date, direct military costs for noncombatants have been limited. But the United States has been pressuring European allies to commit materiel to help reopen the Strait of Hormuz. NATO members have hesitated to answer these calls, partly out of frustration at the apparent absence of consultation prior to the war. But they may eventually find it in their economic best interest to assist in re-establishing shipments from the Middle East.

Other costs to public coffers are becoming more significant. As we discussed last week, governments are offering some support to households to offset higher energy prices. But the burden of sustaining these programs may limit their lifespans.

The impacts on government spending could get considerably larger if the war takes a turn for the worse. In that case, recession becomes a very real possibility; governments may take steps to put a floor under the economic damage. Efforts to address the emergencies of 2009 and 2020 proved successful, but added substantially to national indebtedness.

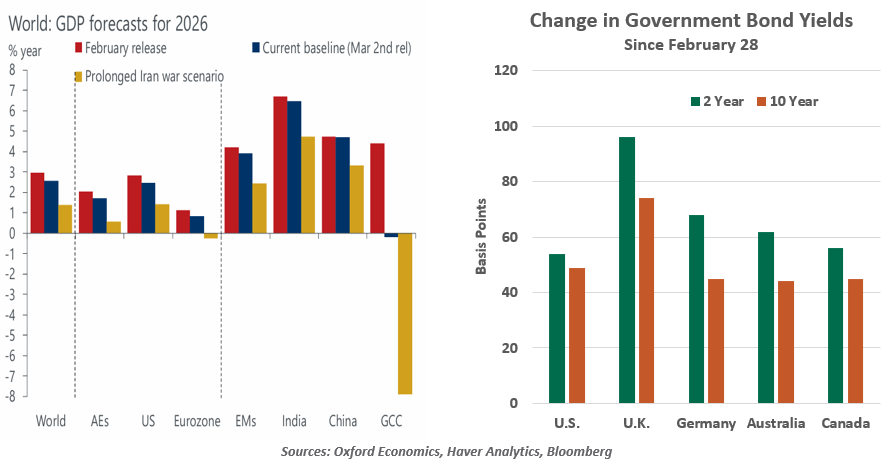

Countries are also facing the prospect of much higher borrowing costs to support that debt: inflation concerns have led to a selloff in government bond markets around the world. Sovereign yields have jumped, in some cases substantially.

Government income is also being impaired by the war. With production curtailed, Gulf countries are losing an estimated $1 billion per day in energy revenue. Destinations in the Middle East are going to experience sharp declines in tourism, which generates significant amounts of economic activity. Overall, Oxford Economics estimates that growth in global gross domestic product (GDP) will be 0.2% lower than previously estimated, shaving more than $2 trillion from global output and hindering worldwide tax receipts.

The war will deepen deficits, and add to interest costs.

Through all of these avenues, the war will deepen budget deficits around the world. This will create particular discomfort for countries in Europe. The euro area reestablished fiscal limitations in 2024, after suspending them during the pandemic. Rules could be relaxed again, but this might challenge investor patience. Last year’s budget stress in France suggests a need for more discipline, not less.

In the United Kingdom, the Treasury was projecting some headroom under its budget targets, which it hoped to use to make strategic investments in its economy. That fiscal space is now gone, and with it, prospects of improving the country’s competitiveness.

A series of countries have also been forced to intervene in foreign exchange markets. India is foremost among nations who have taken steps to arrest the declines of their currencies, selling U.S. dollar-based reserves to do so. These reserves will eventually need to be replenished, as they serve as an insurance policy against further declines and against efforts by speculators to profit from short positions.

The battle in Iran arrived at a time when national budgets were already stretched. In the wake of the war, the calculus of fiscal policy has become much more complicated.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.