Weekly Economic Commentary | January 9, 2026

The New South American Calculus

Maduro's removal will enable a new vision of natural resources and regional realignment.

By Vaibhav Tandon

Mao Zedong once warned that power grows out of the barrel of a gun. In recent decades, global institutions and markets that make kinetic interventions less common. But when those mechanisms fail, power will fill the void.

Venezuela offers a clear illustration of that dynamic. Markets and international sanctions punished the country, but did not bring down its regime. This led Washington to use force. While the political ramifications of President Nicolás Maduro’s arrest are still not clear, the economic consequences are taking shape.

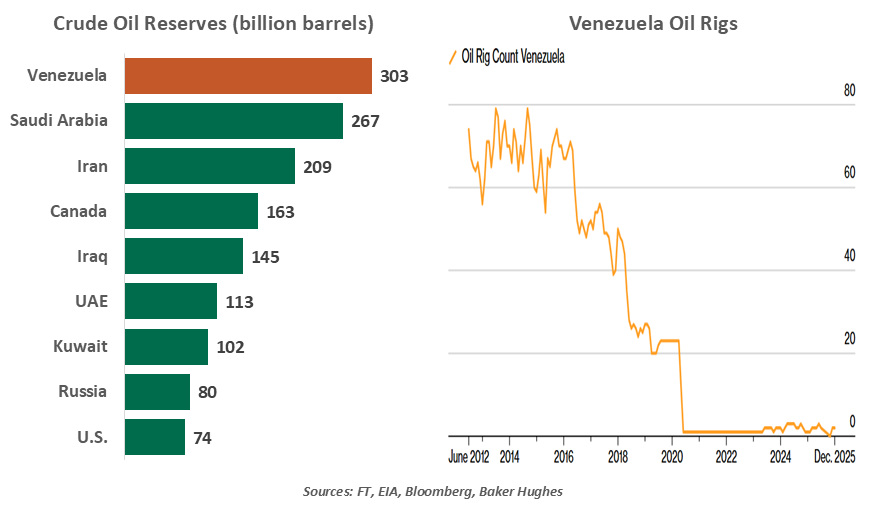

Venezuela sits atop the world’s largest proven crude reserves, totaling over 300 billion barrels or about 17% of the global total. Despite that heft, the country now produces less than 1 million barrels per day (mbpd) of oil, down from nearly 3.5 mbpd (8% of global supply) in the late 1990s.

Venezuela’s global economic footprint has shrunk in parallel. It now accounts for barely 0.1% of world gross domestic product (GDP), compared with roughly 1% in the 1970s. The country’s GDP in 2025 stood almost 70% below its 2013 peak.

Prolonged mismanagement, underinvestment, domestic policy volatility and foreign sanctions have hollowed out Venezuela’s oil sector. Now, Washington seeks to revive Venezuelan crude output by channeling billions of dollars into rehabilitating production. The U.S. is hoping to replicate the success of Panama, whose income per capita has more than tripled since America’s 1989 intervention.

On the surface, Venezuela’s reserves suggest tremendous potential. In practice, unlocking them will be slow and costly, and even potentially unviable. Venezuela’s state and infrastructure are much more degraded than those of Panama. Its crude is heavy and sour, requiring specialized infrastructure and large upfront investment. While U.S. refineries can import and process such grades, restoring the necessary wells and infrastructure could cost $10 billion a year over the next decade. That’s equivalent to more than a third of what the largest American oil firm has budgeted this year for global capital expenditures.

Rebuilding Venezuelan output will be a multi‑year, multi‑billion‑dollar exercise.

The timing is also unfavorable. Oil prices have been hovering near multi‑year lows, amid rising worldwide supply and softening demand from China. That backdrop, combined with Venezuela’s history of expropriating foreign assets, will be a significant hurdle for energy companies considering multi‑billion‑dollar investments in the country.

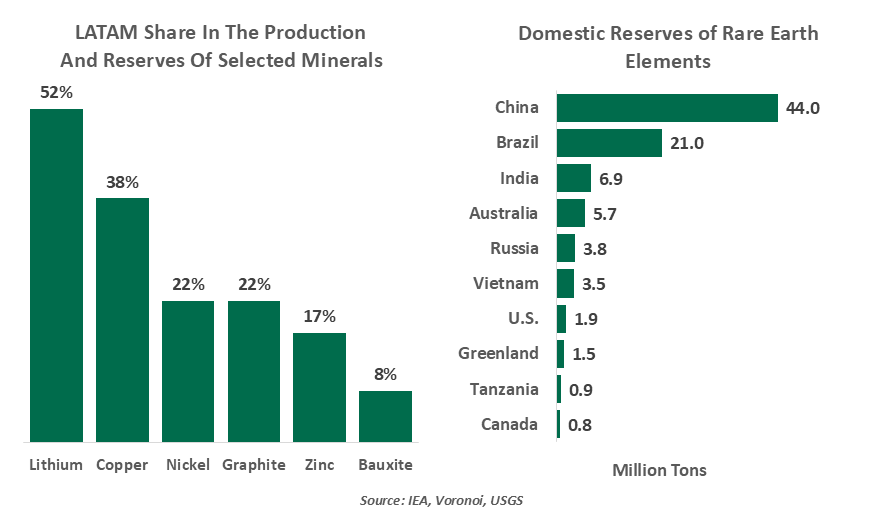

Washington’s renewed focus on Venezuela may not be solely about hydrocarbons. The 2025 U.S. National Security Strategy elevates the Western Hemisphere as a core priority, linking economic security to control over vital real assets. China’s threat of export controls on rare earths laid bare the United States’ dependence on Chinese supply. Recent U.S. willingness to extend economic and political support to Argentina suggests that mineral-rich Latin America (LATAM) is moving to the center of U.S. strategic planning.

LATAM already occupies an important position in global mineral markets. The region has a global share of 40% of both production and reserves of copper. It supplies more than a third of the world’s lithium, with Chile and Argentina the second‑ and fourth‑largest global producers. The continent also holds substantial potential in graphite, nickel, manganese, and rare earths. Venezuela is known to hold large deposits of gold, iron ore and bauxite. Brazil alone controls roughly 20% of global reserves across several of these commodities.

Last week’s intervention seeks to reaffirm U.S. influence in the region. China has steadily deepened its economic links with LATAM nations, eroding U.S. sway in a region long regarded as America’s strategic backyard. China-LATAM trade exceeded $500 billion in 2024. Chinese firms have become dominant investors in key sectors like energy, mining, and infrastructure, raising supply chain and geopolitical concerns.

Venezuela sits squarely in the middle of that contest. Since 2000, it has received over $100 billion in Chinese loan commitments, making it Beijing’s fourth‑largest bilateral borrower. Outstanding debt to China is now estimated at $10 billion. Prior to the December blockade, Venezuela exported the majority of its crude to China. Those supplies met only about 4% of China’s total import needs; for Beijing, the preservation of repayment flows may matter more than the barrels themselves.

LATAM could become a focal point in the U.S.-China contest for influence.

Within the region, reactions have been mixed. Argentina has already signaled support for U.S. actions, while Mexico and Brazil remain more cautious. Although the likelihood of direct U.S. intervention in other LATAM nations appears low, the show of muscle in Venezuela could lead Washington to press harder for trade-related concessions. In Mexico’s case, U.S. leverage in upcoming United States-Mexico-Canada Agreement negotiations may be used to push for stricter enforcement against Chinese trade and investment, raising the prospect of protracted talks or renewed tariff threats.

Mao may have been right: power can emerge from force. But it is difficult to generate economic growth at the end of a bayonet. Venezuela’s future, and that of the Western Hemisphere, will depend critically on re-establishing policies, markets and institutions that are durable. The hard work in Latin America is just beginning.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.