'%3e%3cpath%20d='M14.5584%2010.5857L23.6652%200H21.5072L13.5999%209.19156L7.2843%200H0L9.55034%2013.8992L0%2025H2.1582L10.5087%2015.2935L17.1783%2025H24.4626L14.5582%2010.5857H14.5588H14.5584ZM11.6025%2014.0215L10.6348%2012.6375L2.9357%201.62451H6.25036L12.4638%2010.5123L13.4315%2011.8963L21.5082%2023.4491H18.1935L11.6027%2014.0219V14.0213L11.6025%2014.0215Z'%20fill='%23808182'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_20_84'%3e%3crect%20width='24.4624'%20height='25'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

%20is%20a%20leading%20provider%20of%20wealth%20management,%20asset%20servicing,%20asset%20management%20and%20banking%20to%20corporations,%20institutions,%20affluent%20families%20and%20individuals.%20Founded%20in%20Chicago%20in%201889,%20Northern%20Trust%20has%20offices%20in%20the%20United%20States%20in%2019%20states%20and%20Washington,%20D.C.,%20and%2020%20international%20locations%20in%20Canada,%20Europe,%20the%20Middle%20East%20and%20the%20Asia-Pacific%20region.%20%3c/desc%3e%3cpath%20fill='%233d4042'%20d='M21,21H17V14.25C17,13.19%2015.81,12.31%2014.75,12.31C13.69,12.31%2013,13.19%2013,14.25V21H9V9H13V11C13.66,9.93%2015.36,9.24%2016.5,9.24C19,9.24%2021,11.28%2021,13.75V21M7,21H3V9H7V21M5,3A2,2%200%200,1%207,5A2,2%200%200,1%205,7A2,2%200%200,1%203,5A2,2%200%200,1%205,3Z'%3e%3c/path%3e%3c/svg%3e)

%20-%20https://sketch.com%20--%3e%3ctitle%3eEmail%3c/title%3e%3cdesc%3eShare%20article%20via%20email%3c/desc%3e%3cg%20id='Article'%20stroke='none'%20stroke-width='1'%20fill='none'%20fill-rule='evenodd'%3e%3cg%20id='article-desktop'%20transform='translate(-291.000000,%20-905.000000)'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cg%20id='Group-3'%20transform='translate(280.000000,%20700.000000)'%3e%3cpath%20d='M12.5859376,205%20L25.5,216.098563%20L38.4140625,205%20L12.5859376,205%20Z%20M11,206.352162%20L11,221.582916%20L19.5446429,213.697123%20L11,206.352162%20Z%20M40,206.352162%20L31.4553572,213.697123%20L40,221.582916%20L40,206.352162%20L40,206.352162%20Z%20M21.1197917,215.049268%20L12.5212054,223%20L38.4787946,223%20L29.8802084,215.049268%20L26.1688988,218.240388%20C25.7827601,218.567837%2025.21724,218.567837%2024.8311012,218.240388%20L21.1197917,215.049268%20L21.1197917,215.049268%20Z'%20id='Shape'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cpath%20d='M317.048444,961%20C318.677807,961.001791%20319.998224,962.333083%20320,963.975866%20L320,963.975866%20L320,972.789759%20C320,973.478748%20319.446027,974.037283%20318.762667,974.037283%20L318.762667,974.037283%20L313.420222,974.037283%20L313.420222,980.619276%20C313.466211,981.335082%20312.928257,981.953082%20312.218333,982%20L312.218333,982%20L298.781667,982%20C298.071743,981.953082%20297.533789,981.335082%20297.579778,980.619276%20L297.579778,980.619276%20L297.579778,974.037283%20L292.237333,974.037283%20C291.553973,974.037283%20291,973.478748%20291,972.789759%20L291,972.789759%20L291,963.975866%20C291.001776,962.333083%20292.322193,961.001791%20293.951556,961%20L293.951556,961%20Z%20M311.486889,970.525371%20L299.513111,970.525371%20L299.513111,980.050743%20L311.486889,980.050743%20L311.486889,970.525371%20Z%20M314.395276,962.742345%20C313.970645,962.65481%20313.549254,962.905694%20313.420222,963.322865%20C313.394809,963.404999%20313.380715,963.490265%20313.378333,963.576269%20C313.380722,963.661209%20313.394821,963.7454%20313.420222,963.826423%20C313.529012,964.18316%20313.855609,964.426832%20314.225778,964.427444%20C314.659193,964.427644%20315.022348,964.096906%20315.066078,963.66215%20C315.109809,963.227395%20314.819907,962.829881%20314.395276,962.742345%20Z%20M317.130097,962.784571%20C316.813535,962.651298%20316.448506,962.723595%20316.20547,962.967701%20C315.962434,963.211807%20315.889338,963.579564%20316.020315,963.899239%20C316.151293,964.218915%20316.460504,964.427444%20316.803556,964.427444%20L316.803556,964.427444%20C317.274992,964.425655%20317.651006,964.045094%20317.651006,963.576269%20C317.652304,963.230394%20317.44666,962.917844%20317.130097,962.784571%20Z%20M311.783656,955%20C312.500482,955.040538%20313.043667,955.574507%20312.997231,956.192982%20L312.997231,956.192982%20L312.997231,959%20L297.002769,959%20L297.002769,956.192982%20C296.956333,955.574507%20297.499518,955.040538%20298.216344,955%20L298.216344,955%20Z'%20id='icon-print'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

Tax News You Can Use | For Professional Advisors

Jane G. Ditelberg, Chief Tax Strategist

While taxes imposed by the federal government may get the most press, state and local governments impose their own taxes, some of which are quite hefty. Some states impose income taxes, but other state-level taxes include property taxes, sales taxes, estate or inheritance taxes and real estate transfer taxes. The types of taxes and the rates vary widely among the states, and taxpayers moving to a new jurisdiction should evaluate all applicable taxes in a comprehensive manner to determine how a move would impact their overall tax bill.

The cumulative impact of state and local taxes is felt more deeply since legislation in 2017 and 2025 capped the federal income tax deductions for state and local taxes (SALT). And as states look to address their own budgets, a number of states have enacted or at least proposed special “Billionaire’s Taxes” “Millionaire’s Taxes”[1] or “Mansion Taxes,”[2] essentially adding higher income tax brackets, wealth taxes, or higher real estate transfer taxes for high income or wealthy taxpayers on top of the usual rates. With some state and local tax jurisdictions imposing more significant burdens than ever, many taxpayers question whether it makes sense to relocate to reduce the taxes they are or will be subject to.

Whether or not your move is motivated by tax considerations, it is important to understand what the tax burden will be in the jurisdiction of your new home and how to establish residency there.

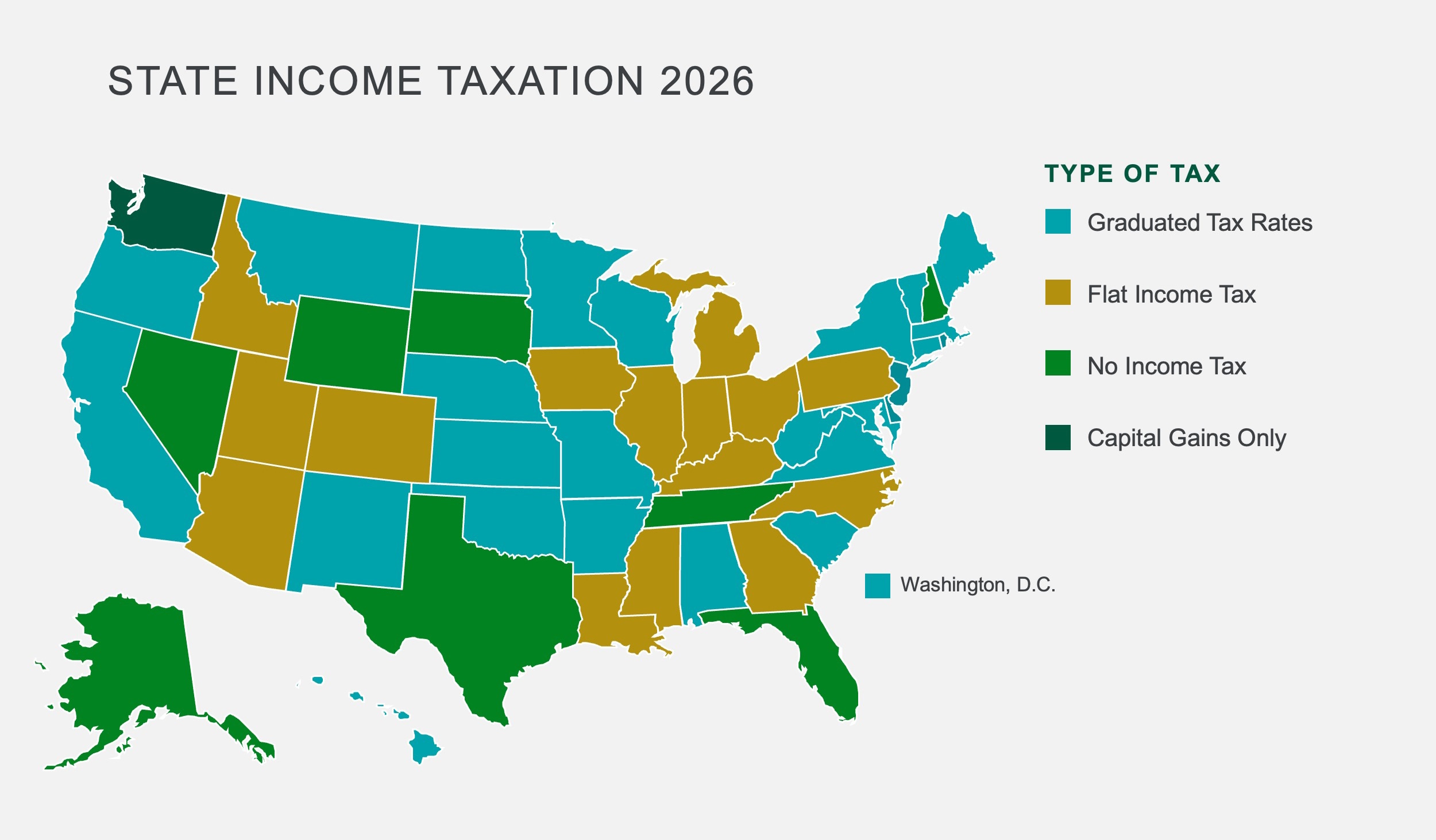

Income Taxes

Eight states do not impose an individual income tax, one state taxes capital gain only, 14 states impose a flat tax, and the remainder have graduated income tax rates. The following map documents the current state income tax rates:

The following table lists the bottom and top income tax rates for 2026 for the 10 states with the highest state tax rates.

Note that the bracket thresholds matter. For a lower-income taxpayer, taxes may be higher in Minnesota, where the lowest bracket is 5%, than they would be in California, where the highest marginal rate is 14.4% but the lowest bracket is 1%.

Sales Tax

Sales taxes are imposed on the purchase of goods and sometimes services and may be imposed by the state or any local unit of government. There are five states that do not impose a state-wide sales tax, but, among these, Oregon, Alaska and Montana have localities that impose sales tax. New Hampshire and Delaware have no sales tax at all but impose excise taxes on certain types of purchases (New Hampshire) or a gross receipts tax (Delaware) that have a similar effect. The local (state or county) portion in some states is larger than the state rate, so it is important to consider the aggregate rate applicable. The following table shows the 10 states with the highest average combined state and local sales tax rates in 2026.

The gap between the state tax rate and the combined tax rate means there are areas in the state where the highest rates do not apply. Therefore, properly evaluating a move will require understanding the specific rates applicable in the local area you plan to live, as well as where you are likely to shop.

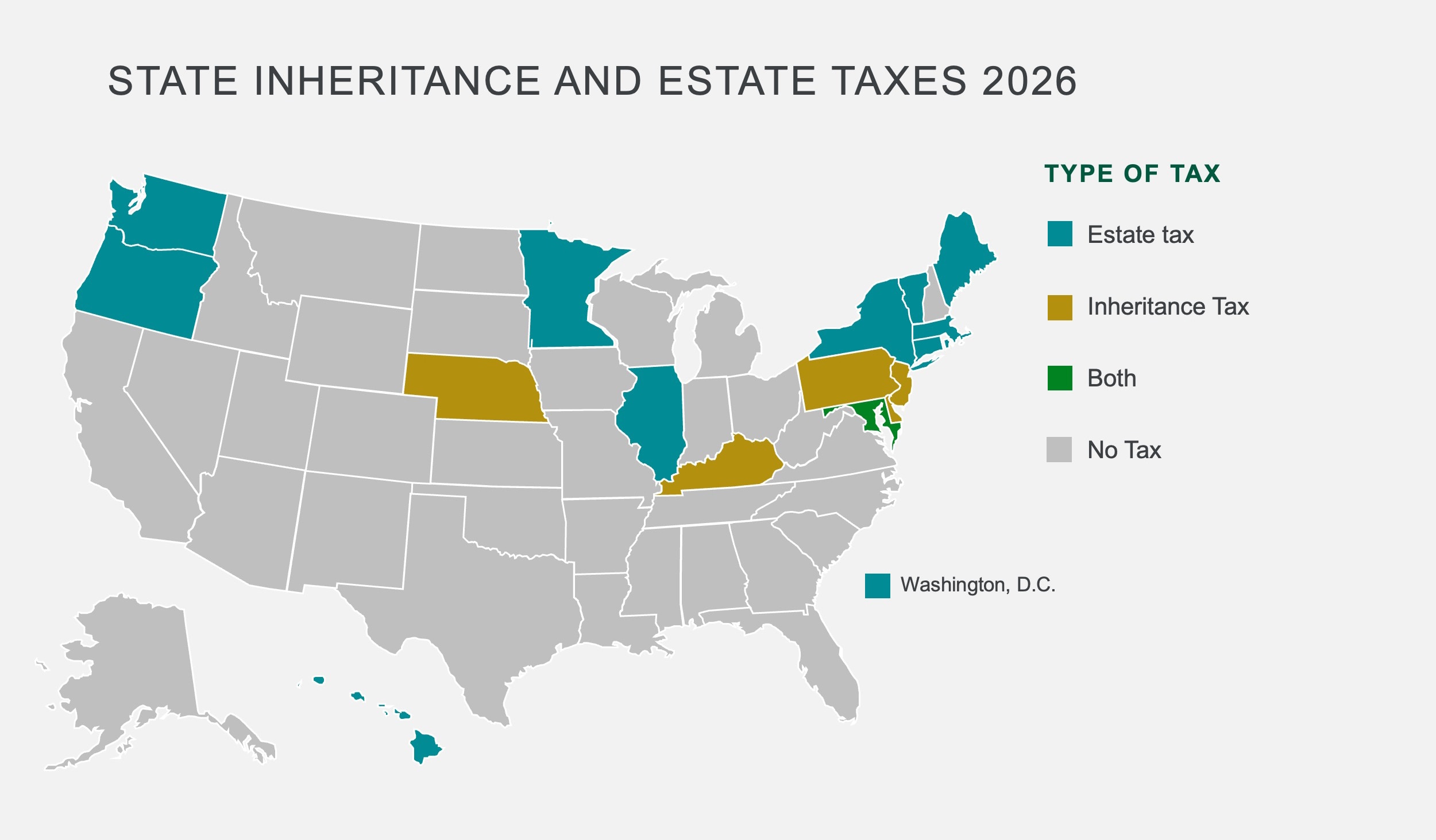

Estate and Inheritance Taxes

Estate and inheritance tax rates are harder to compare, in part because each state may tax different things, have different exemption amounts or different rates. Estate taxes are imposed on what the decedent owned at death, while inheritance taxes are imposed on the recipient and may have different rates depending upon the recipient’s relationship to the decedent. Maryland imposes both an estate tax and an inheritance tax, 12 states (including Washington D.C.) impose an estate tax only,[1] and four states impose an inheritance tax only.[2] Washington has the highest marginal rate of 35%. Oregon has the lowest exclusion, taxing assets over $1 million, and Connecticut has the highest, matching the federal exclusion, currently at $15 million. This leaves 33 states imposing no inheritance taxes or estate taxes at all. This can make a significant difference in terms of what will be available to your beneficiaries after your death. The following map shows the states that impose estate taxes and/or inheritance taxes.

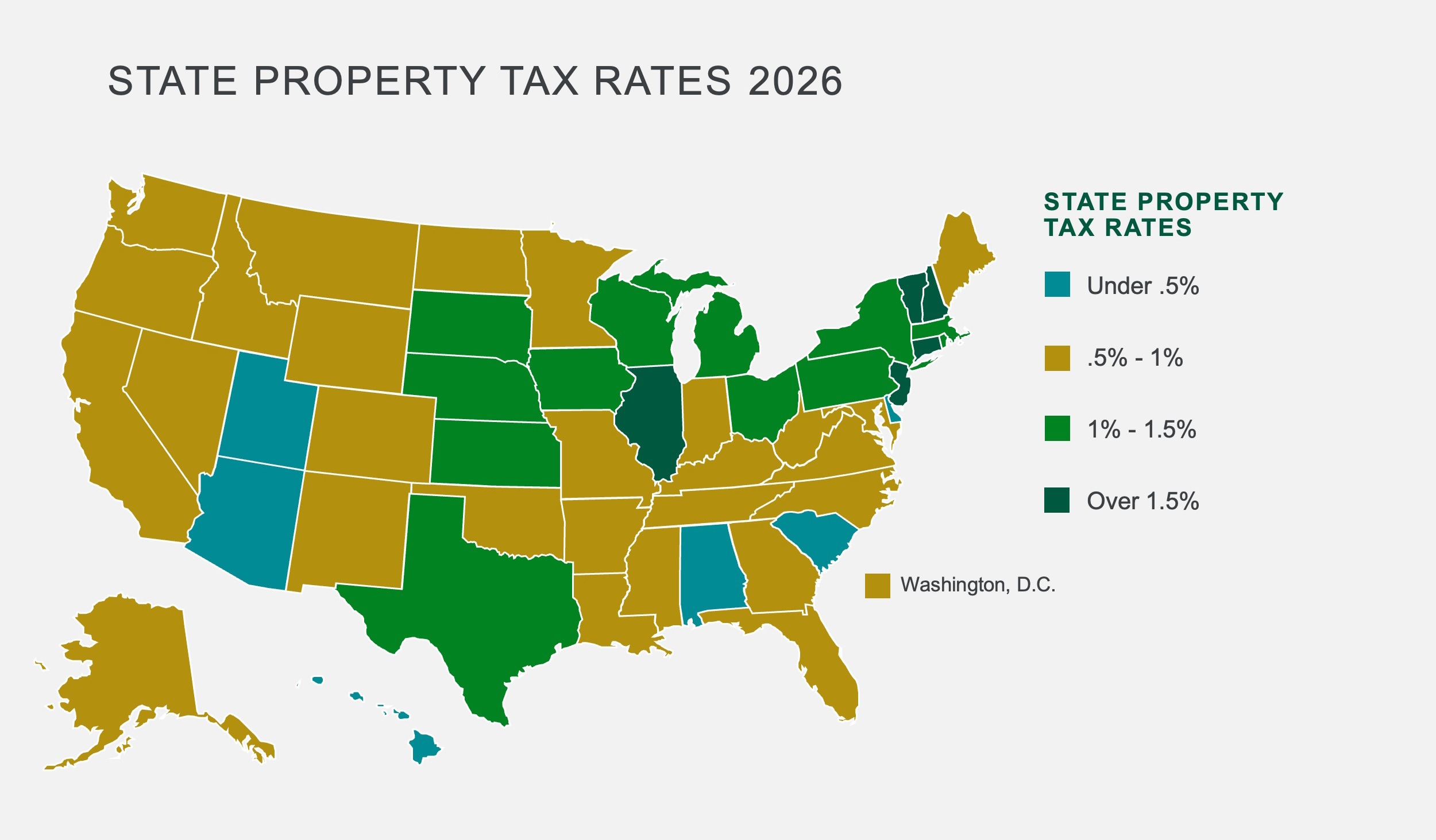

Property Taxes

Every state imposes real property taxes. The rates vary widely, but it is also important to keep in mind that home values also vary widely from place to place. It is possible that your property tax bill in Hawaii, the state with the lowest tax rate, will be higher than your property tax bill in New Jersey, the state with the highest rate. It is also important to determine whether you qualify for any exemptions, such as homestead property or senior citizen status. State property tax rates are shown on the map below. Be aware that there can be additional property taxes imposed at the local level in some areas, which are not included in the illustration.

Taxes are one factor to consider when making decisions

Do People Relocate for Tax Purposes?

There is not a straightforward way to identify the motivation of taxpayers who move without asking them directly. For most people, their motivations are likely mixed. But for some, taxes play a key role in that decision, particularly for individuals who already spend time in two or more states and can plan where to spend the majority of their time to establish tax domicile. According to data collected by the IRS, billions of dollars of income have shifted from high-tax states to states with lower taxes. The growing number of states proposing wealth taxes or higher income tax rates for millionaires or billionaires is likely to strengthen this trend. Kiplinger reported on a study showing that about 70% of the $4 billion in adjusted gross income that migrated out of state came from households earning over $200,000.

Whether taxes motivate a move or not, it is important to evaluate the taxes that will apply in a new location when considering a move. A comparison of applicable taxes between your current state and a new state may impact the timing of certain transactions. Depending on the numbers, receiving deferred compensation or incurring tax on a Roth IRA conversion when residing in a low-tax state may increase the benefit. Similarly, buying a more expensive home may be more attractive in a state with lower property taxes.

Things To Consider In Relocating.

Taxes are one factor to consider in deciding when making decisions about relocation, but there are many other factors to consider. Remember that a move will impact quality of life in many different areas — big and small. Each family needs to balance these factors when determining whether and where to move. Here are some ideas to consider:

Lifestyle Considerations

- What are the options for public and private schools?

- What is the proximity to major airports?

- Where is the nearest major hospital or specialized doctor?

- What is the proximity to your family and friends?

- Is there public transportation nearby?

- What is the crime level?

- What civic and cultural events are there?

- What outdoor and/or recreational activities are there, and is the weather favorable for participating in your favorite pastimes?

- What are the options for assisted living or elder care?

- Can you age in place, or will another relocation be needed?

Spending Considerations

- Is the sales tax higher or lower than your current location?

- Will a change in the cost of living impact your spending?

Tax Considerations

- What will your property tax burden be, and what exemptions might be applied?

- What sources of income are subject to state income?

- What are the local gasoline taxes, and taxes on other products or services you use regularly?

- Are there state-level estate or inheritance tax considerations?

Other Considerations

- Is there veterinary care nearby for any pets?

- Are there weather or climate considerations that will impact your insurance bill (flood, wind, or hurricane damage) or other decisions?

- How often will family and friends be able to visit you, and are there accommodations nearby for them if they will not be staying with you?

Steps for Establishing a New Tax Domicile

Once you have made the decision to change your domicile, there are steps to take to successfully establish tax residency in your new state. This following list is representative but not exhaustive. Also remember that where your immediate family members are living, working, or going to school will also be relevant. Seek legal and tax counsel familiar with the laws in both the old and new jurisdictions.

- Obtain a driver’s license in the new state (and do not renew the one from your old state)

- Register your vehicle in the new state

- Register to vote in your new location

- If applicable in the new state (e.g., Florida), file a Declaration of Domicile or similar document with the local court

- Review and update your estate plan

- Review and update property and casualty insurance policies

- File federal tax returns using your new address

- File tax returns in the new state as a resident, and file as a non-resident in the old state if you have income there

- Reference your new domicile in any legal documents

- Update your mailing address for credit cards, account statements and other recurring mail

- Relocate heirlooms and collectibles to your residence in the new domicile

- Evaluate moving memberships, such as club memberships, library cards, houses of worship, and other affiliations, and reflecting non-resident status on ones in your former state of residence.

If you have questions about state taxes or other issues related to relocating, please contact your Northern Trust Advisor.

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)