- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | February 27, 2026

Tariffs: A Lost Year

A long-form review of what tariffs have accomplished and what may be in store.

By Carl Tannenbaum, Ryan Boyle and Vaibhav Tandon

My father used to tell me that if I found myself in a hole, I should stop digging. I might offer the same advice to those setting trade policy in Washington.

Last week’s Supreme Court ruling has prompted a re-set of U.S. tariff policy. As an updated strategy is being formulated, it is worth assessing whether the effort is worth sustaining. A high level review suggests that American trade policy over the last year has detracted from economic performance, and should be re-thought.

It’s been a little over a year since the second Trump administration imposed its first volley of new tariffs. The world had been put on notice that this weapon would be brandished, and had been preparing for its application. But few foresaw the blizzard of tariff advances and retreats which have made the last twelve months so challenging for a wide range of stakeholders.

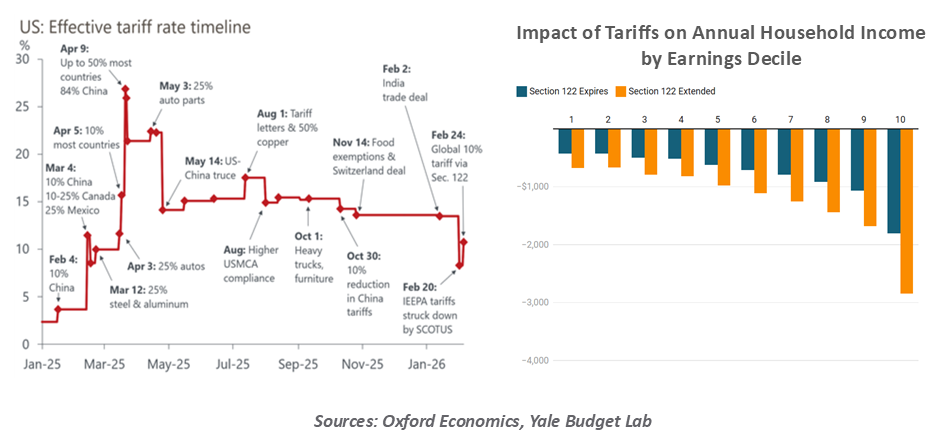

Pronouncements have come with frequency. Some have been long on generalities and short on details; others have been modified or scuttled before they became effective. At times, the effort has stressed raising revenue; at others, reshoring. Measures of trade policy uncertainty are seven times higher than they were at the start of 2024.

U.S. importers and their foreign counterparts have had their heads on collective swivels, trying to orient themselves in the best possible way. Complying with the orders has not been easy; forms and procedures have been created on the fly, complicating collections. Coping with them has diverted attention and resources from more productive applications.

The U.S. trade deficit is deeper than ever, and there is scant evidence of production shifts back towards the United States. A recent study from the Federal Reserve found that trade protection had not resulted in increased capacity utilization at American factories. While some companies have announced plans to build new facilities in the U.S., their openings are far into the future. Employment in the U.S. manufacturing sector remains stagnant.

Tariff threats have had a very limited impact on trade with China, the country that owns the largest trade surplus with the U.S. The subject of trade friction in the first Trump administration, China has been preparing for a new round of trade restrictions for a number of years. They have effectively subverted tariffs by using transshipment points, and they accumulated leverage in negotiations through control of commodities essential to technology.

Several counterparts agreed to trade “deals” in 2025, which took the form of broad outlines. Details on many of these arrangements remain incomplete, and some are now in suspense because of the weekend action to implement an across the board tariff. Other leading exporters have provided support to their regional industries to preserve their global market share.

The uncertainty created by tariffs has diminished economic activity.

Any benefit to U.S. producers has been modest at best, and the reliability of the United States as a trade negotiator has come under question. This will certainly complicate negotiations to renew the U.S.-Mexico-Canada Agreement this spring.

And then there is the impact on consumers. The Yale Budget Lab estimates that tariffs cost the average household more than $800 last year. Tariffs are taxes, and they hit lower income households proportionately harder. While economic growth was good last year, forecasters suggest that it could have been higher by at least half of a percent in the absence of tariffs.

A central reason for these disappointments is that the tariff program did little to address the real root causes of America’s trade imbalance. Policies like tariffs can have an influence on where production takes place, but the U.S. trade deficit is primarily the result of two fundamental forces

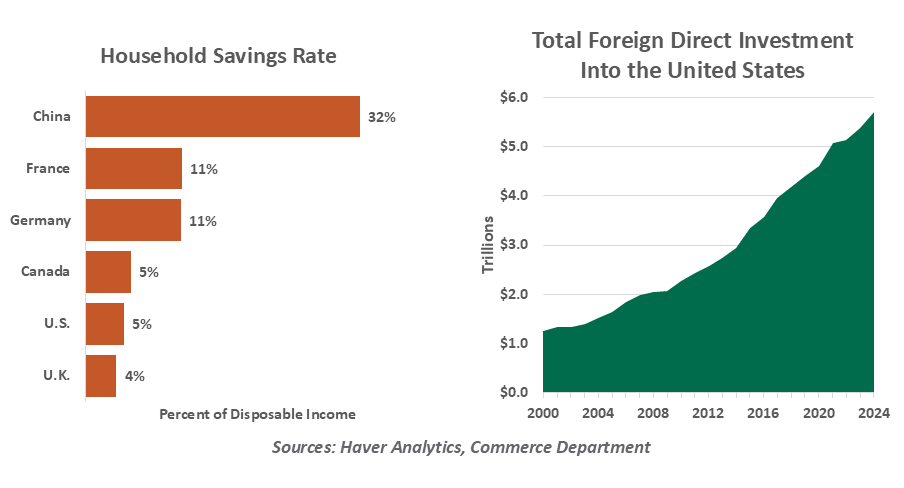

a) Americans spend a much higher fraction of their incomes than consumers in other developed countries. Saving rates in the U.S. are half of what they are in Europe and one-fifth of what they are in China.

Higher levels of demand inevitably pull in a lot of goods that are produced overseas. To sustain their spending, U.S. households have access to the most expansive system of consumer credit in the world.

Recent fiscal policy has added to America’s consumption imbalance. The One Big Beautiful Bill Act that passed last summer is expected to produce substantial tax refunds this spring; a good portion of the proceeds will be spent on imported goods.

There are measures which could be taken to favor saving over spending, such as tax advantaged investment opportunities or a value added tax (VAT) that adds to the costs of consumption. Many other countries have a VAT, which may explain why their saving rates are higher. For a variety of reasons, though, the United States has been reluctant to pursue policies that would curb consumerism.

b) The United States is a favored destination for financial capital. The level of foreign direct investment in the U.S. is six times higher than it was at the turn of the century. Strong asset returns, liquid markets, and a well-developed legal and regulatory regime all contribute to these inflows.

Money brought to America’s shores by investors is spent on imported products. (Technically speaking, the capital account and the current account are mirror images of one another.) Curbing imports will require reducing capital inflows, an outcome which could reduce U.S. asset prices and/or raise interest rates.

The developments of the past year have given global investors pause about their level of investment in the United States. But while they are hedging their exposure to dollar assets, there is little evidence that they are reallocating their portfolios to other markets.

Tariffs don’t address the real root causes of the U.S. trade deficit.

In sum, the two biggest root causes of the U.S. trade deficit have gone unaddressed. From this perspective, it is not surprising that the imbalance hasn’t improved.

My father and I used to play a lot of gin rummy, at which I lost often. After a defeat, I would insist on a rematch, as if the outcome had been a fluke. Sometimes, he would tell me, it’s better to cut your losses and quit when you are behind.

Down But Not Out

The second Trump administration has been characterized by fervent activity. The president has erred on the side of acting first and leaving questions for later. Last week, some of the legal questions raised by tariffs were answered, but new actions and new questions lie ahead.

Emergency powers were not the sole justification for trade actions in the past year. Section 232 national security protections were invoked for metals, the auto sector and select semiconductors. Section 301 reprisals for other nations’ unfair trade practices were enacted in the first Trump term against China, and remained in force through the Biden administration; Trump then escalated them last year.

We can expect to hear many more invocations of these sections of trade law. Last year’s section 232 investigations are nearing completion, while Section 301 country reviews are now being launched. These processes require research and comment periods, but any tariffs that stem from them will usually prove durable. Importers and nations affected by these tariffs lack recourse. No legal precedent is set to challenge tariffs enacted under these sections; even if litigation is filed, appeals will be slow and deliberate.

The ruling will only bring about a change in trade war tactics.

This still leaves the majority of recent trade actions in an unsteady state. Shortly after the Court ruled, the White House invoked Section 122 to enact a temporary 10% tariff on all imports. This action is legally limited to only 150 days, but it buys time to complete other investigations for tariffs. Despite ratification in 1974, Section 122 has never been used to place tariffs. The law was meant to remedy temporary balance-of-trade deficits, and today’s application may also be improper. But we do not expect a legal challenge to overturn it on this short timeframe.

The Supreme Court did not opine on refunding of tariffs already paid. If the tariff was illegal, then payments should be refunded, but that decision will require separate legal action on an uncertain timeline. We have been braced for a brief inflationary shock as final prices adjust to offset tariffs, but it never gathered momentum. Now, most tariff rates are taking a step down, which should rule out a price surge. Importers’ margins will be bolstered by the temporarily lower customs duty.

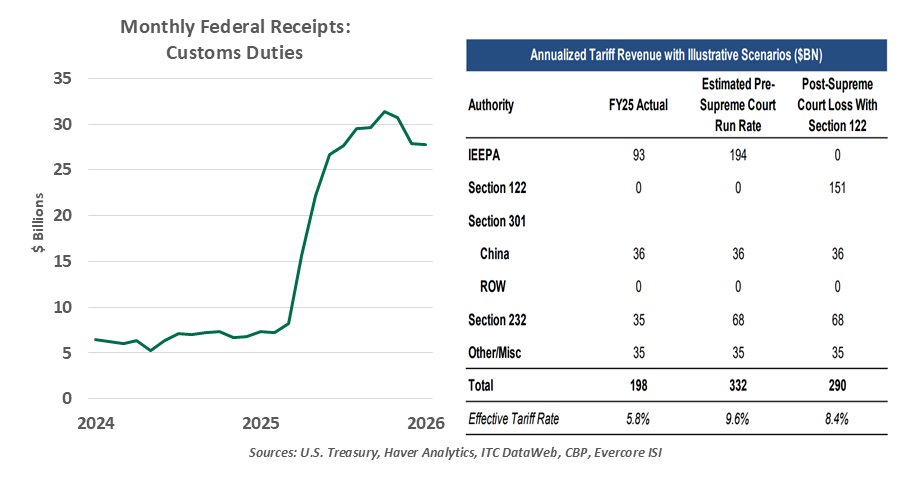

Tariffs have unambiguously added to U.S. federal revenue. The pace of tariff collection is now set to slow, but not fall to old norms. The weighted average tariff rate is lower today but still at a historically high level; the tariff rate is poised to rise as investigations are completed. Last year’s reconciliation package locked in a trajectory of higher deficits, which will only be compounded by this loss of government revenue. The Yale Budget Lab forecasts that tariff revenue in the decade ahead has fallen by half with the revocation of International Emergency Economic Powers Act (IEEPA).

The U.S. has also used tariffs as a negotiating tool, such as discouraging purchases of oil from Russia. Those secondary tariffs have now been rendered moot. Trans-shipment, or routing goods through favored nations to reduce tariffs, will no longer face a special penalty. The soft power of tariff threats has clearly diminished.

Tariffs can be an effective remedy against specific unfair terms of trade, like state subsidies. Deploying them as a broad-side weapon in the trade war was beyond their capability. New tariffs will be better defended and more deliberately targeted. The emergency may be over, but the trade war will drag on.

International Implications

The Supreme Court’s ruling strikes at the heart of the U.S. administration’s trade strategy, constraining its ability to wield tariffs as an all-purpose policy threat. By limiting the use of emergency powers to impose sweeping tariffs, the Court has reshuffled the balance of winners and losers, at least in the near term.

The biggest beneficiaries are nations that had borne the brunt of the emergency levies. China, India and Brazil emerge as clear winners, as the flat Section 122 surcharge replaces high country‑specific rates that were implemented under IEEPA. China still faces the highest relative tariffs, but the differential has narrowed, which may reduce transshipment incentives.

The tariff pivot has created some winners and losers overseas.

North American trading partners face relatively low effective tariff rates, but the impact of the Supreme Court ruling is likely to be limited given the already high level of United States‑Mexico‑Canada Agreement (USMCA) compliance. Section 122 carries forward almost the same set of carve‑outs that existed under the emergency tariff regime, so the universe of goods shielded from the new levy is largely unchanged.

By contrast, some countries that had negotiated preferential treatment under the old framework now look relatively worse off, as new levies stack on top of existing Most Favored Nation rates. The European Union (EU) and the U.K., in particular, find themselves disadvantaged by a higher baseline that erodes the value of earlier concessions, while Japan’s prior advantage has also been marginally stripped away.

More importantly, the ruling has cast a shadow over existing trade deals. While U.S. officials insist that previously agreed arrangements remain intact, trading partners are less convinced. The European Parliament has delayed ratification of its deal, Britain has hinted at retaliation, and India has postponed trade talks. The decision also weakens America’s ability to threaten sweeping, unilateral tariffs against Canada and Mexico as leverage to extract further concessions in the upcoming USMCA review.

So while the Court ruling may favor some and hinder others, all of America’s trade partners are facing a new round of uncertainty. No one will be terribly happy about that.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.