Global Economic Outlook | December 12, 2025

Charting New Courses: Northern Trust's Economic Outlook for 2026

What paths will major markets find in 2026?

This year has witnessed some of the most significant policy shifts in recent memory. Economic, strategic and fiscal norms have all been challenged, creating a level of uncertainty that has been hard keep up with.

Fortunately, challenges to the foundations of global growth did not cause them to crack. Activity once again proved resilient, a quality which forecasters often underestimate. We expect the global expansion to continue at a modest pace in 2026.

This year, we collaborated with our partners in Northern Trust Asset Management to identify economic themes that underpin the annual Capital Market Assumptions. The following areas will have an important bearing on the outlook for next year, and beyond.

Rising Innovation, Declining Demographics

Technological progress continues to accelerate, with artificial intelligence (AI) at the heart of it. AI promises to deliver efficiency gains and unlock new growth opportunities. The United States is expected to remain the global leader in innovation, benefiting from its deep capital markets and fast adoption of advanced technologies. China is a contender for primacy, making AI models and chips a strategic priority.

Countries that are unable to keep pace will struggle to sustain long-term economic growth amid the aging of workforces. They will be challenged to attract capital and balance budgets.

AI introduces a range of issues, from infrastructure to job displacement to privacy and ethics. Expect this emerging technology to attract heightened social and regulatory attention, not all of it positive.

The Global Shift to Self-Reliance

Geopolitical tensions and pandemic-era supply chain vulnerabilities have accelerated a trend toward greater economic self-sufficiency. The United States is at the forefront of this pivot, deploying industrial policy and onshoring to reduce import dependence. While this shift promises resilience, it comes with higher costs and erodes the benefits of global integration.

Trade has become more tense, but decoupling is easier said than done. For trade-dependent economies, the shift threatens growth prospects as they face reduced market access and rising barriers, making adaptation both urgent and complex. The related paradigm change in global security could have important long-term consequences for some countries and regions.

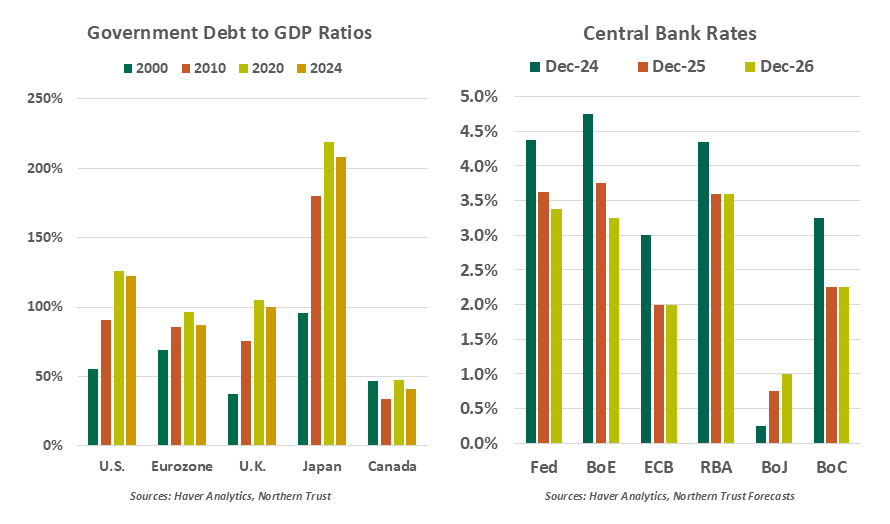

Debt and Deficits Loom Large

Fiscal discipline has been in short supply, but the need for it is rising. Massive debt burdens threaten higher interest rates, higher taxes and higher inflation in the years ahead. Across advanced economies, credible fiscal frameworks will be critical to maintaining market confidence as debt sustainability concerns increasingly shape policy choices.

The potential for fiscal stress is no longer limited to emerging markets. The United States, despite its stronger growth outlook, faces rising interest costs and political hurdles to deficit reduction. Europe and Japan are even more constrained. Investors have been reasonably patient with the global accumulation of debt, but a day of reckoning may be near at hand.

Following are our thoughts on how top markets will fare in 2026.

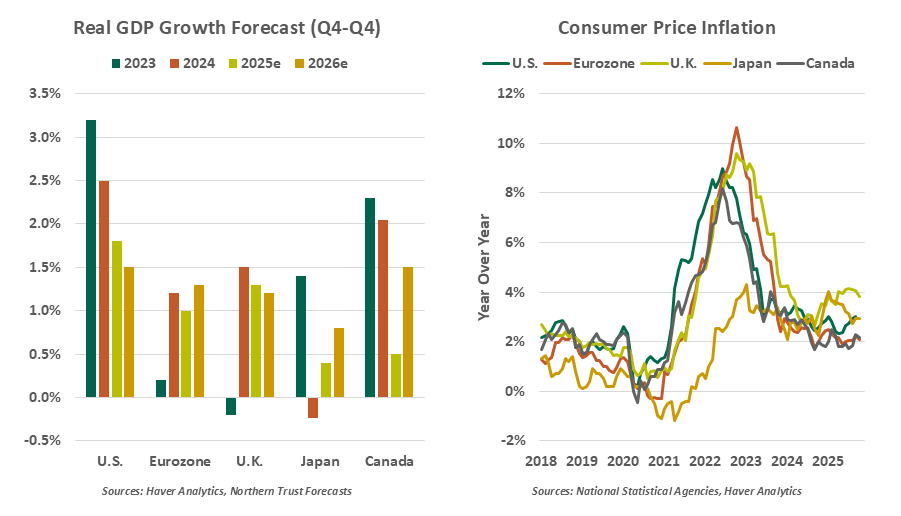

Consumption and AI will remain key drivers of U.S. growth.

United States

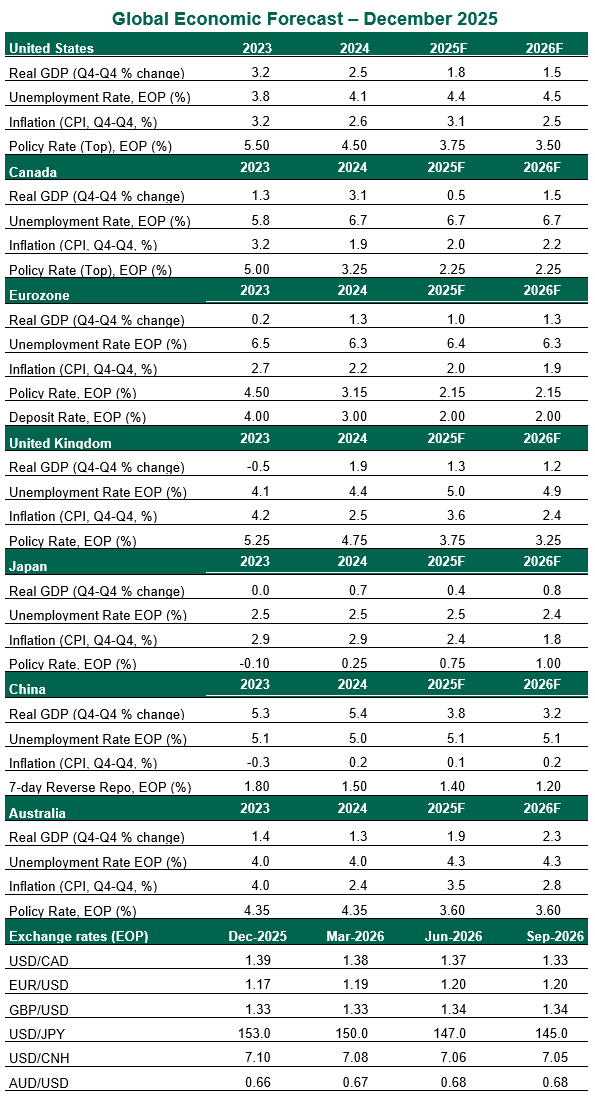

- Policy uncertainty has been a focal point in the U.S. over the past year, with effects felt worldwide. But entering the second year of the second Trump term, policy is reaching a steadier state. Tariff escalations appear to be behind us, with nations like Japan and Korea nearing agreements; a one-year détente with China was also an important signal. The “One Big Beautiful” reconciliation bill set a clear path for tax rates and investment incentives.

- However, the new steady state is still quite different from the long-running status quo. Imports are more expensive, immigrant labor has been dislocated, and popular fear of recession has not abated. Adapting to the new normal will take time, but we believe the post-pandemic expansion will continue. Consumption, buoyed largely by wealth effects, will continue to lead the way.

- Our forecast is for inflation to remain moderately elevated through the first half of 2026. Tariff costs are working their way to final prices gradually, but they will be a one-time shock. Firm wage growth will keep inflation above target thereafter. The employment outlook will vary by sector, with favorable conditions for the construction and manufacturing sectors offset by challenges in healthcare, higher education and federal government. After intervening in the latter months of this year to support a softening labor market, the Federal Reserve will prioritize its inflation mandate and reduce rates only once more in 2026.

Eurozone

- The eurozone economy managed modest growth this year despite persistent headwinds, but performance has been uneven across major regional markets. The Spanish economy gained, but momentum faded in Italy and stalled in Germany after a robust start to the year. The recent strength in French gross domestic product (GDP) growth is unlikely to sustain, given fiscal challenges and political uncertainty. With inflation and growth steady, the European Central Bank policy remains “in a good place,” implying that current interest rates are appropriate.

- The euro area is expected to gain momentum from improving consumption backed by tight labor markets and supportive monetary conditions. But growth will fall short of potential, constrained by U.S. tariff impacts, weak external demand and uneven fiscal capacity across member states. While Germany’s fiscal expansion will provide some support, French and Italian governments remain restrained by weak public finances. Persistent manufacturing weakness will prevent core economies from firing on all cylinders..

- Unlike the U.S., the eurozone’s fragmented innovation ecosystem and slower technology adoption will limit its ability to offset its demographic drag with productivity. Geopolitical shifts have reinforced Europe’s push for strategic autonomy, but execution will be fraught with challenges. The U.S. is pushing for its European allies to curb their reliance on China, even as China slows and intensifies competition with Europe in sectors like autos. This dual pressure leaves Europe squeezed between its largest security partner and a major trade counterpart, forcing choices that risk undermining growth and competitiveness.

U.K. faces another year of sluggish expansion.

United Kingdom

- After a robust first half, growth in Britain shifted to a lower gear. Consumers pulled back, and businesses have been hesitant to invest. The growing use of AI has provided some support to capital spending through a surge in data center construction, but the broader investment outlook remains downbeat.

- A soft economy will push inflation closer to the Bank of England’s 2% target. The labor market is cooling, with unemployment rising to its highest level since early 2021 and pay growth decelerating. This weakening backdrop, combined with fiscal tightening, has strengthened the case for a gradual easing cycle starting in December and continuing through mid-2026.

- Though near-term turmoil was avoided as the government restored fiscal headroom in its latest budget, Britain’s political situation and public finances remain fragile. In our view, the back-loaded nature of recent budget measures has not fully restored credibility in the fiscal framework, leaving the feedback loop between higher yields and worsening fiscal forecasts intact. While Britain’s demographic profile is somewhat more favorable than that of many European peers, an aging population and generous retirement systems will add pressure to public finances. The risk of a leadership challenge within the ruling Labor Party next year could inject further fiscal uncertainty.

Canada

- Geopolitical tensions and U.S. industrial policy have reshaped North American trade dynamics. U.S. tariffs have inflicted noticeable pain on Canada’s economy. The nation barely avoided a recession at midyear. Tariff exclusions for U.S.-Mexico-Canada Agreement (USMCA)-compliant products and easing monetary and fiscal conditions have helped stave off a broader downturn. The Canadian labor market appears to have bottomed out, with few signs of a spillover to the broader economy.

- The Canadian economy may struggle to sustain momentum amid threats of further trade disruptions. The uncertainty will continue to drag on industrial production, exports and business investments. We see auto tariffs as a key source of downside risk to the Canadian economy; the longer they remain in place, the greater the risk of carmakers relocating production.

- Unlike many peers, Canada’s relatively strong fiscal position provides room to sustain a positive fiscal impulse in the year ahead, as reflected in the 2025 budget. This will help cushion near-term weakness, even as potential output is limited by slowing labor force growth and productivity constraints. Weaker growth and subdued inflation will allow the Bank of Canada to hold rates steady at the slightly stimulative level of 2.25% through 2026

Japan’s hard-won exit from deflation is set to hold for another year.

Japan

- Despite headwinds from U.S. tariffs, the Japanese economy has managed to stay afloat, supported by resilient domestic demand. A virtuous cycle of inflation and wage gains appears to have taken hold but not spiraled. Private consumption and capital expenditure have grown for six consecutive quarters, and we expect these forces to remain the primary drivers expansion in the coming year. The new prime minister’s steer toward fiscal stimulus, coupled with a growth strategy centered on strategic investments in areas such as AI, will offer additional support.

- Japan’s external sector could struggle due to higher trade barriers in the United States and rising friction with its second-largest trading partner, China. Reduced Chinese demand for Japanese goods will weigh on exports, while a decline in Chinese tourism will limit inbound travel receipts.

- The Bank of Japan’s (BoJ) cautious pivot toward monetary normalization is set to continue. With wage hike demands likely matching or exceeding last year’s pace, the BoJ appears poised to raise its policy rate in December. While this meeting is unlikely to provide clarity on the future path of hikes, another round of robust pay gains from next year’s Shunto negotiations will pave the way for one more rate increase in 2026.

China

- Much like other parts of the world, the Chinese economy proved more resilient than expected this year. Robust performance in the first half was supported by front-loading of U.S. imports and continued trade diversification away from America. However, a notable slowdown is forthcoming.

- Domestic challenges remain significant. The ongoing property sector downturn, sluggish industrial activity and persistent deflationary pressures will continue to weigh on growth. Consumption will lose momentum as the impact of the recent goods trade-in program fades. Structural issues, including an aging population and rising debt burdens, will limit the scope for large-scale demand stimulus. Though China is competing directly with the United States in the AI space, it will not be a panacea for its productivity challenges. A relatively high share of Chinese output is physically intensive and less exposed to automation.

- On the external front, U.S.-China trade tensions remain a key risk. Presidents Trump and Xi agreed to a oneyear tariff truce in October, but a comprehensive deal will be elusive: thorny issues such as technology restrictions, intellectual property and security concerns will be difficult to resolve. For 2026, our base case assumes continued uncertainty, limiting China’s ability to rely on external demand as a growth engine.

Australia

- A gradual recovery, underpinned by improving household spending, is underway in Australia. Less restrictive monetary policy and ongoing fiscal measures have made conditions more conducive to growth. Buyers are returning to the property market, pushing prices higher as interest rates ease. Yet the path ahead remains finely balanced. Consumers could tighten their belts again as inflationary pressures re-emerge, job growth slows and wage gains moderate.

- Cost pressures and tariff-related uncertainty are forcing Australian firms to pause or scale back expansion plans. While Australia is less exposed than others to American tariffs, it remains vulnerable to China’s economic slowdown and the knock-on effect of weaker demand on commodity prices.

- Australia’s economic challenge lies in its constrained supply side and weak productivity growth, which have lowered the economy’s potential growth rate and stalled disinflation. Population growth will remain a headwind for labor supply, and AI is unlikely to compensate completely. Against this backdrop, we foresee the Reserve Bank of Australia maintaining an extended pause through 2026 as the most likely outcome.

The move from free trade to self-reliance will put pressure on EMs’ growth model.

Emerging Markets

- Emerging markets (EMs) have relied on exports and integration into global supply chains for growth. This strategy is now on a collision course with the U.S. shift toward self-reliance. As Washington prioritizes domestic manufacturing, technology security and energy independence, EMs may face weaker demand for their goods. Tariffs have settled far above pre-trade war levels, which will impair exports. With other nations lacking the scale to fully compensate for lost U.S. demand, export-led EMs are set to face a tougher growth environment.

- For EMs, AI presents both an opportunity and a threat. On one hand, it can boost productivity. On the other, automation could lead to widespread job displacement, leaving millions unemployed or underemployed. Countries investing in digital infrastructure and skills development will be better positioned to harness AI’s upside, though scaling efforts may face financing constraints and weak transmission networks. EMs have quietly strengthened their debt profiles in recent years, a reversal of the traditional risk narrative. This improvement, driven by stronger policy frameworks and macro fundamentals, suggests lower fiscal risks heading into 2026.

- India remains a clear standout among emerging economies, underpinned by strong demographics, a focus on closing infrastructure gaps and a thriving tech ecosystem. Unlike many peers, India’s growth story is anchored in resilient domestic demand and less on international trade. These structural tailwinds position India as a relative outperformer in 2026, even as global trade patterns shift and advanced economies pivot inward.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.