Neither Here Nor There

Uncertainty has not impaired overall economic performance.

Anthropologists use the term “liminal state” to describe an ambiguous period of transition. A person or group has left their old normal behind but has not reached their new steady state, like a child maturing to adulthood or a region enduring a natural disaster.

The U.S. economy has entered a liminal period. We are in the midst of trade and fiscal policy transitions; uncertainty is too prevalent to feel that we are in a new normal. So far, economic data is holding up well. Worst-case fears of policy-led inflation or job losses have not come to pass.

As highlighted in our midyear themes, we welcome the trend of resiliency over recession. As long as the worst uncertainty remains behind us, we believe the domestic economy will continue to grow. But liminal spaces can feel disorienting.

Following are our thoughts on the U.S. economy.

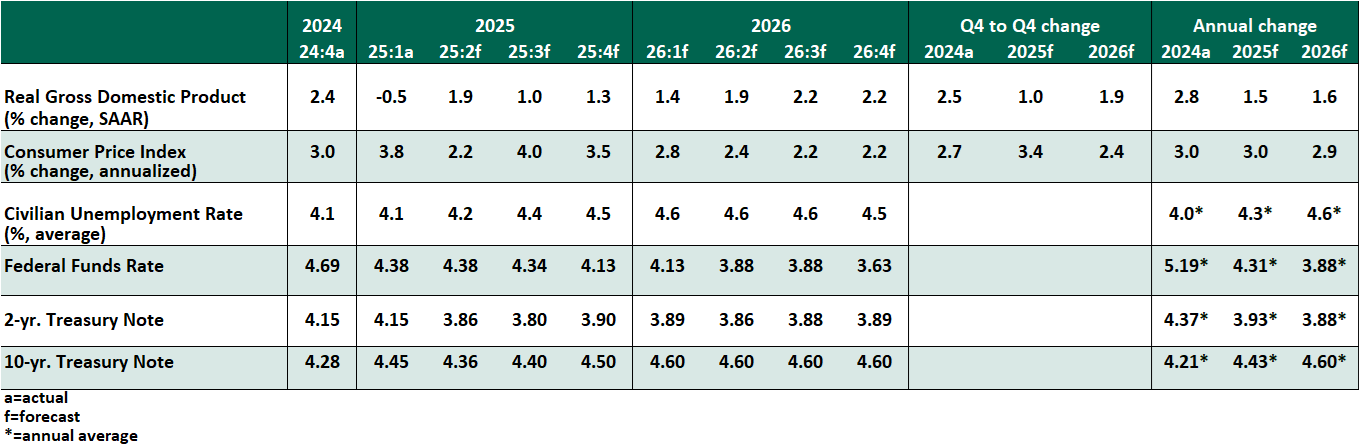

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The labor market remains steady. The June employment report exceeded tepid expectations with a gain of 147,000 jobs. The unemployment rate fell one tenth to 4.1%. The details of the report were less encouraging: hiring was concentrated in the government and healthcare sectors, and the unemployment rate was held down by a decline in the labor force. The ratio of vacancies to job seekers has held above 1:1 for the past year, a broad indicator of balance, though higher continuing unemployment claims suggests that those who lose their jobs are struggling to find work.

Our forecast assumes that some strains remain in store for the labor market. However, halted border flows and a push toward immigrant removals will limit growth of the labor force, which will hold down the unemployment rate.

- Consumer spending is showing some sluggishness, which was expected after households front-loaded major purchases in the early part of the year. Nominal retail sales fell -0.9% from April to May, led by slower vehicle sales.

The first quarter decline in gross domestic product (GDP) was an anomaly caused by higher imports. That flow stopped in April, and we expect a return to a slower but more normal composition of growth in the remainder of the year.

- Inflation also continues at a moderate pace. In May, the consumer price index grew 2.4% over the past year, or 2.8% on a core basis (excluding food and energy). The deflator on personal consumption expenditures was similarly stable but above-target at 2.3% and 2.7% core. Evidence of tariff-driven inflation in goods prices is scant.

- Healthy job gains and warm inflation justify the Federal Reserve keeping a patient posture. At its June meeting, the Federal Open Market Committee left rates unchanged, but offered a Summary of Economic Projections that reflected some differences of opinion around the table. The median Fed governor forecasts two rate cuts before the end of the year, but a growing contingent expects no changes until 2026. None forecasted a hike.

The next move will be a cut, with a question only as to timing. If the data remain consistent with current readings, we believe a move in September will be justified, with a cautious pace of easing to follow.

- The new fiscal bill was ratified, with few surprises or major alterations in its final negotiations.

The act included a $5 trillion increase to the statutory debt limit, ending fears of a technical default this year. The national debt will rise, but bond markets have continued to take this news in stride. Long-term interest rates have remained within a reasonable range.

Individual experiences of the bill will vary. Manufacturers and other capital-intensive businesses will gain from renewed deductibility of investments, but healthcare and renewable energy firms will lose important funding. Households will benefit from higher standard deductions, child tax credits and enhanced state/local tax deductibility, but reduced healthcare funding will be a burden for many. Beneficial components are front-loaded, and the near-term stimulus may help offset some of the costs of trade policy.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.