Global Economic Commentary | June 29, 2026

Straitening Out

The ceasefire builds confidence in the outlook for global growth.

Discussing the Outlook

The Northern Trust Economics team reviews the key facts and risks in their global forecast.

In choppy waters, many novice ship passengers will experience sea sickness. The only sure remedy is to wait it out. Symptoms will pass, as will the rough waters.

While the Middle East is still far from calm, it does appear the worst of the volatility in the region is in the past. The U.S.-Iran ceasefire is in place, with negotiations underway for a more durable peace. Most importantly for the global outlook, ship traffic through the Strait of Hormuz is starting to increase.

If the Iran conflict has ended, then so has the greatest risk to the growth outlook. Effects will linger: waves of inflation are still causing some upheaval, and shortages of critical commodities could continue to manifest for months to come. Central banks are watching prices closely to chart an appropriate course for policy.

Following are our outlooks for the world’s major markets.

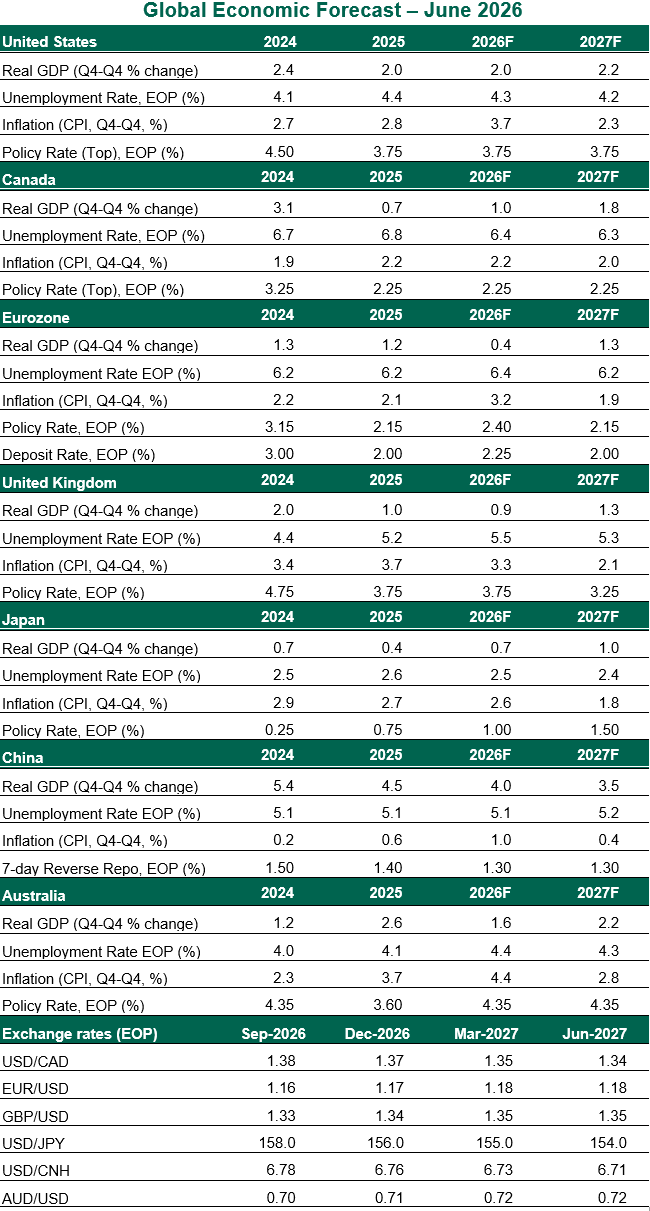

United States

- The U.S. labor market is coming back to life after a long dry spell. A gain of 172,000 new jobs in May, plus upward revisions to prior months, suggest the “no hire, no fire” dynamic is breaking toward renewed hiring. Inflation remains a challenge, with the headline consumer price index reaching 4.2% year-over-year in May; tamer core inflation (excluding food and energy) of 2.8% suggests the pass-through of energy costs has been limited. The Iran deal will support price stability, though a renewed tariff push will lead to a new round of uncertainty.

- Under the new leadership of Chair Kevin Warsh, the Federal Open Market Committee (FOMC) has squarely reaffirmed its commitment to price stability. New task forces will evaluate the central bank’s approaches to its communications, balance sheet, use of data, inflation frameworks, and views on productivity and jobs. Many aspects of the Fed may evolve, but the 2% inflation target will stand firm. In the June Summary of Economic Projections, nearly half of FOMC members expected a rate hike by end of year. We expect steady rates, with risk of a hike.

Canada

- Working through a technical recession, we have marked down our growth outlook for Canada. The decline of output in the first quarter was driven partly by one-off shifts in gold imports and government spending. Consumer spending and business investment showed modest gains, and they will support a return to growth. The Canadian economy saw an encouraging report of 88,000 job gains in its May Labor Force Survey, though this jump only serves to return employment to the level it had attained at the start of the year.

- The Canadian consumer price index gained 3.2% year-over-year in May, led by energy; core inflation remained composed at 1.6%. With core prices staying composed, the Bank of Canada held rates steady at its June meeting, a posture we expect to continue through 2027. A broadening of inflation could necessitate hikes, or a recession taking hold could bring about cuts; on balance, a prolonged hold is appropriate. The main policy event will be negotiations surrounding the U.S.-Mexico-Canada free trade agreement. A breakthrough before the July 1 deadline looks implausible. The default outcome of a shift to annual renewals will not be beneficial to cross-border investment.

Eurozone

- The eurozone economy remains stable but without a convincing recovery. Following a narrow first quarter gross domestic product (GDP) decline of -0.2%, dragged down by a contraction in volatile Irish GDP, recent activity indicators offer little hope for a rebound. Retail trade excluding fuel and autos was nearly flat in April. Business sentiment surveys have arrested their decline, but remain in contractionary territory. Industrial production has flattened, held down by a decline in German factory orders. Falling energy prices and a more stable trade environment should help bring about a return to growth in the second half of the year. The European Union‘s trade deal with the U.S. should promote more commerce, though a new U.S. investigation into German drug pricing shows that tensions can return.

- The European Central Bank (ECB) reacted decisively to inflationary risks, raising policy rates by a quarter-point at their June meeting. The decision was accompanied by guidance that the ECB would take a meeting-by-meeting approach. An important data point since then was the announcement of the U.S.-Iran ceasefire and accompanying decline in energy costs. With this key inflationary risk reduced, we no longer expect additional hikes. Stable prices and slow growth will clear the way for a rate easing next year.

United Kingdom

- Growth conditions in the U.K. remain weak, with monthly GDP falling by 0.1% in April; weakness in services offset gains seen in other categories. The full effect of higher energy prices may still be in the pipeline due to a looming hike in the energy price cap, hampering a recovery in consumption. Restrictive monetary and fiscal conditions will present further headwinds to a broad-based recovery. Inflation in May of 2.8% year-over-year was encouragingly below expectations, held down by a deceleration in food and core goods prices.

- The Bank of England Monetary Policy Committee (MPC) showed policy restraint at their June meeting, holding rates at 3.75%, with two dissents in favor of a rate hike. MPC members will take their time to gauge the durability of lower energy prices and the risk of second-order inflationary effects; we anticipate calmer inflation will prevent a decision to hike rates this year. Another leadership contest is unfolding, but we do not expect a new Prime Minister to propose any additional government spending, given limited fiscal space and recent market sensitivity. A clearer leadership path and cooler inflation have helped to bring the yield on 10-year U.K. gilts down by more than 40 basis points from their May 15 peak; easier financial conditions may be accretive to growth.

Japan

- The Japanese economy has not suffered the worst inflationary effects of the global shock. Headline inflation in May rose to 1.5% year-over-year, or 1.8% excluding fresh food and energy; a policy push to contain the effects of energy prices has helped to blunt the shock. However, higher costs will weigh on corporate investments. Occasional interventions have been needed to stabilize a falling yen, while the ten-year Japanese Government Bond (JGB) yield has climbed more than 50 basis points this year, reflecting greater concerns of fiscal sustainability.

- The Bank of Japan (BoJ) continued its tightening cycle with a 0.25% policy rate increase to 1.0% in June. This rate normalization long precedes the Middle East situation, but the global backdrop has added to the BoJ’s reasons to take action against rising inflation. The BoJ has also offered a plan to end quantitative easing, tapering its Japanese Government Bond (JGB) purchases in 2027. We anticipate two additional hikes at a gradual pace through 2027, which will help to arrest Japan’s weakening currency.d

China

- China has shielded itself well from the more severe risks stemming from the Middle East, holding the world’s largest strategic petroleum reserve and controlling its exports of fertilizers. Tighter supplies led to the producer price index of raw materials reaching a four-year high in April, offering a brief respite from deflation. A reduction in tensions in the Gulf leaves China with little sense of relief, given its long-running growth challenges. Weak demand and high inventories are weighing on industrial production and retail activity, while the property sector is moribund. High-tech exports remain a bright spot: AI-driven investment continues unabated, and Chinese electric vehicles are selling well in most markets outside the United States. Sustained growth will require a diversification beyond these narrow sectors.

- China’s continued strategy of growth through exports was a topic of discussion at the G7, and the meeting’s declaration included a call to diversify supply chains of critical minerals. The current cycles of U.S. tariffs, justified with investigations into forced labor and industrial overcapacity, could be used to renew a hard line on trade with China.

Australia

- Inflation remains a key concern for the Australian economy, with lingering effects of energy prices still poised to feed through. Business investment is showing narrow gains in data center and Olympics-related development, while domestic demand remains weak. Nominal household spending fell more than 1% from March to April, across goods and services alike. The unemployment rate moderated slightly to 4.4% in May.

- The Reserve Bank of Australia led developed markets with a return to rate hikes this year, but we expect the passage of Middle East tensions will allow rates to stabilize going forward. Lingering inflation risks will not leave room for rate cuts through next year, absent a material decline in employment or economic activity. Higher interest rates may contain inflation, but at the cost of more subdued consumption and investment.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.